Archive for 2023

Who’s Got Swag?

January 10, 2023 There’s a rush of excitement at Broker Fair and deBanked Connect. Behind the scenes there is also a fun creative process that sponsors get to prepare for right before every event. SWAG! It can be challenging to think of anything other than pens and Post-its to jazz up one’s table with memorable tchotchkes so here is some unforgettable swag from over the years:

There’s a rush of excitement at Broker Fair and deBanked Connect. Behind the scenes there is also a fun creative process that sponsors get to prepare for right before every event. SWAG! It can be challenging to think of anything other than pens and Post-its to jazz up one’s table with memorable tchotchkes so here is some unforgettable swag from over the years:

Broker Fair 2019 in the Roosevelt Hotel, as some might recall, had a live basketball hoop by Rapid Finance. LoanMe brought out squeezable stress relievers and what better way to relieve it than squeezing a money wad. Silver sponsor Cooper Asset had special bags that came in handy when collecting all that swag.

At deBanked Connect San Diego 2019, PIRS Capital gave out mouse pads, great for guests to use at work with a constant reminder of where they got it from. Bitty Advance had reusable water containers, smart to stay hydrated while bouncing from sessions to the sponsor showcase room. BFS Capital had a bowl of candy on their table and who doesn’t love a sweet treat after endless meet and greets.

At deBanked Connect Miami 2019, SOS Capital was looking out for everyone by having a bowl of mints out for grab. And if one can’t calculate large numbers without a calculator handy, RTR Recovery had guests covered with that.

After having a virtual Broker Fair in 2020, Lendini stepped it up a notch with a hand-rolled cigar station at the pre-show party in 2021. If one didn’t have a pen and notepad to take down information, Velocity Capital Group made sure to have plenty available. Velocity also had a mini massage station to loosen everyone up after a tense year in quarantine.

Although Covid took some time away from events, the deBanked Connect Miami 2022 sponsors were more ready than ever to show off their swag. FundFi played it safe with hand sanitizers and the LCF Group knew everyone would need a ChapStick throughout the event after talking all day. FinTap got creative with their very own Staples easy-button that said ‘funded.’ Legend Funding had mini piggy banks, ROC Funding Group had cigar cutters, and Lendini had flasks and raffled off a Gucci duffle bag.

Broker Fair 2022 swag was a blend of the practical with the innovative. THOR Capital had shot glasses and if one needed a coaster for that Lifetime Funding had your back. Now that everyone has moved on to wireless headphones, Dedicated Financial GBC brought back wired headphones, which are perfect for flying. Beyonce said it best, “I got hot sauce in my bag swag,” and everyone could too because IOU Financial had mini hot sauce bottles. Following the tradition of raffling their most-wanted Gucci duffle, Lendini also had mini tool kits and Magic 8 Balls that fortuned all good news surrounding the event.

At deBanked events, sponsors always come through with original swag ideas. With Miami 2023 right around the corner, we are excited to see what will be there this year.

Amazon’s Business Loan Trajectory

January 10, 2023 According to documents purportedly obtained by Business Insider, Amazon plans to increase its business loan operations in 2023, estimating that loan receivables will eventually exceed $2B. Insider also says that its expected loss rate is 1.34%.

According to documents purportedly obtained by Business Insider, Amazon plans to increase its business loan operations in 2023, estimating that loan receivables will eventually exceed $2B. Insider also says that its expected loss rate is 1.34%.

The receivable figure would not be all that surprising as Amazon as been on a steady trajectory upwards over the last decade with the exception of 2020 when covid struck. Its receivables reached $1.4B in Q3 2022. The year-end figure has not yet been released. $2B+ for 2023 would be in line with the historical trend.

2016: $661M

2017: $692M

2018: $710M

2019: $863M

2020: $381M (covid)

2021: $1B

2022 (Q3): $1.4B

Not counted in these figures is financing to Amazon sellers conducted through a third party. Amazon recently teamed up with Parafin on merchant cash advances, Lendistry for Business Loans, and Marcus for lines of credit, for example. Data on funding from these parties is a little more difficult to come by.

Backd Enters the Fifth Year of Funding Dreams

January 9, 2023 AUSTIN, TX – (Jan. 2023) – Backd, a commercial alternative business lender, has kicked off its fifth year in business, with a continued commitment to helping business owners fund and develop their dreams through easy-to-access alternative financing.

AUSTIN, TX – (Jan. 2023) – Backd, a commercial alternative business lender, has kicked off its fifth year in business, with a continued commitment to helping business owners fund and develop their dreams through easy-to-access alternative financing.

Last year the company grew exponentially while being named a 2022 Top Workplace by The Austin American Statesman. This is in addition to adding a business line of credit funding option to complement the already popular working capital. With a focus on a quick and convenient turnaround time to help companies that struggle to obtain conventional financing, Backd is looking to grow its financial products that offer flexible financing this year to support small businesses and allow them to truly thrive in 2023.

As part of this commitment, in the closing months of 2022, Backd CEO Xan Myburgh joined the Forbes Finance Council, a collective invitation-only community created in partnership with Forbes and the expert community builders who founded the Young Entrepreneur Council (YEC).

“It’s truly an honor to join this esteemed community,” Xan said. “As entrepreneurs, we are driven to improve upon the status quo, and I intend to provide my own expertise in entrepreneurial financial knowledge while simultaneously learning from the best business leaders the world has to offer.”

About Backd

Backd is a FinTech company headquartered in Austin that provides alternative financing solutions like working capital and line of credit for growing businesses across the nation.

For more information, visit backd.com, email kieran@backd.com or call Kieran at (512) 621-5169.

deBanked CONNECT MIAMI Has SOLD OUT

January 9, 2023The industry’s largest annual event in South Florida has once again sold out! If you have questions about your existing tickets or sponsorship to deBanked CONNECT MIAMI, please contact events@debanked.com.

This event is being held at the Miami Beach Convention Center on January 19th. It will be deBanked’s 5th event in Miami since 2018. It’s the ultimate networking experience for brokers, lenders, funders, fintech, collectors, lead generators, investors, software companies, law firms, and more. Thank you to Bitty Advance for being this year’s title sponsor.

Financing Fertility

January 6, 2023 Ever heard of financing in vitro fertilization? LendingPoint offers financing opportunities for IVF to help women trying to get pregnant. On average IVF can cost anywhere from $15,000 to $30,000. That’s not cheap. LendingPoint is widely known in the consumer lending space but the range of why borrowers are looking for financing is wide.

Ever heard of financing in vitro fertilization? LendingPoint offers financing opportunities for IVF to help women trying to get pregnant. On average IVF can cost anywhere from $15,000 to $30,000. That’s not cheap. LendingPoint is widely known in the consumer lending space but the range of why borrowers are looking for financing is wide.

“We have some really impactful financing opportunities where we’re financing IVF programs for women to get pregnant, which is probably some of the most lovely stories that we get to hear and an impact that we get to do on someone’s life,” said Amanda Flashner, Chief Experience Officer at LendingPoint.

Different treatments have different price points and different needs. LendingPoint partners with many merchants so that they can offer their own customers what they need at the point of sale. Other types include medical, dental, and home improvement businesses, for example.

Flashner was recently appointed Chief Experience Officer (CXO) which is a new executive position for the company altogether. Advocating on behalf of their customers, she is responsible for their beginning-to-end experience, making sure it’s personalized to the customer centricity that they’re building.

“It’s a really exciting time. I like to say our customers have always been the heart of our company and they are, and our CEO (Tom Burnside) has been an incredible advocate for the customer experience practice that I helped build here from the ground up at LendingPoint, but now our customers really have a seat at that table, helping make big decisions on their behalf, so that’s really exciting.”

CXO is not commonly heard of like CFO or COO but Flashner said she does see this role becoming more important in an executive committee of other companies.

Get Ahead in 2023 with These Best Accounting Practices for MCA Companies

January 6, 2023

As we draw the curtain on 2022 with the festive holiday season and prepare to kick off 2023 with a bang- with ambitious goals and the highly anticipated industry meetup at deBanked Connect in Miami on January 19-, your company accountant is gearing up for a busy quarter. Depending on the level of financial organization in your MCA business, filing your annual taxes can be a breeze or a nightmare.

Better Accounting Solutions has been the premier accounting partner in the MCA space for over a decade, and we’ve compiled some of the best accounting practices you can implement now to make your taxes easier next year:

1. Determine your income recognition method and be consistent with it:

This is important for three reasons:

a) Accurate financial reporting: Consistently applying a single income recognition method ensures that the financial statements accurately reflect the income earned by the business. This is important for internal decision-making and stakeholders such as investors and creditors who rely on these statements to assess the business’s financial health.

b) Tax compliance: Proper income recognition is important for tax compliance purposes. The method used to recognize income can affect the amount of tax that a business owes. By consistently applying a single method, the business can ensure that its tax returns are accurate and avoid potential issues with the tax authorities.

c) Simplicity: Consistently applying a single income recognition method can also make it easier for the business to prepare and file its tax returns, as well as to manage its overall financial record keeping. This can save time and reduce the risk of errors or discrepancies.

2. Understand Writeoffs:

As a business owner, it is important to understand how to maximize write-offs in order to reduce your company’s tax liability, and one way to do this is by taking advantage of deductions and credits that are available to the company. For example, businesses can write off typical expenses such as employee salaries, office rent, and supplies. On top of that, you may be able to write off meals, trips, and events if they are being done for the business, so consult your accountant to see what counts.

It is also important to ensure that these expenses are properly documented in the company’s financial records, and that they are being paid for using company cards accounts rather than personal accounts for business expenses. This is because personal expenses are not tax deductible, whereas (many) business expenses generally are. By using clearly delineated company accounts, businesses can ensure that they are able to properly document and claim these expenses as deductions on their tax returns.

3. Documentation, Documentation, Documentation!

Businesses and governments are run on the back of paperwork, and ensuring you are on top of your documentation and records is the best way to ensure smooth operations and compliance. This includes making sure:

All your business licenses and registrations are in order.

Your W-2’s are filed by the end of January.

Determine who you need to get W-4’s and W-9’s from:

It’s important to know how to categorize your partners to establish clean and complete records. Filing inconsistent records, internally or compared to their paperwork, can cause issues and complications down the road when you file your taxes.

For example, an ISO is typically classified as an independent contractor rather than an employee. As such, an ISO would typically need to fill out a W-9 when working for you, rather than a Form W-4.

Form 1099 is a tax document used to report various types of income other than wages, salaries, and tips that are reported on a Form W-2. Form 1099s are typically issued by businesses or other organizations to contractors or other independent workers for services rendered or income received.

Independent contractors, including ISOs, are responsible for paying their own taxes and are not entitled to the same employment benefits as employees, so you’d need to get a W-9 form from them and then give them a 1099 based on the information they gave you.

Better Accounting Solutions recommends not giving syndicators 1099s from you because we’ve found that many syndicators have different methods of reporting their recognized income to the IRS, and we do not want to report differing numbers to the IRS, which can lead to obvious complications.

It is important for businesses to correctly classify workers as either employees or independent contractors to ensure that the proper tax forms are used and that the correct amount of taxes are withheld or paid.

Speak to an experienced financial expert to determine how to classify your partners, vendors and employees.

Get a W-9 from all of your partners (ISO’s, etc.) before you pay them, otherwise, you’ll have to chase them for paperwork when they’ll have no incentive to get it to you in a timely manner.

4. Ensure You Are Getting The Best Financial and Accounting Advice:

If there is a major theme in this piece, it is the importance of having access to expert financial and accounting advice and guidance, particularly in an industry as complicated as merchant cash advance.

Whether you work with an in-house CPA or work with a large accounting firm, do consistent check-ins and self-audits to make sure your business is getting the premier service it deserves, which will certainly save you a significant amount of stress, time and money.

Last Chance to Comment on SBA’s Proposal to Lift SBLC Moratorium

January 4, 2023 In November, the Small Business Administration formally proposed a rule to lift the moratorium on licenses for Small Business Lending Companies (SBLCs). The moratorium wasn’t some pause borne out of the covid era. It’s been in place since 1982, creating a market of just 14 licensed SBLCs over the span of 40 years. Originally this moratorium had only gone into place because the SBA “did not have adequate resources to effectively service and supervise additional SBLCs” but now in modern times the SBA has determined there’s a problem, “that certain markets where there are capital market gaps continue to struggle to obtain financing on non-predatory terms.” Their solution? Lift the moratorium.

In November, the Small Business Administration formally proposed a rule to lift the moratorium on licenses for Small Business Lending Companies (SBLCs). The moratorium wasn’t some pause borne out of the covid era. It’s been in place since 1982, creating a market of just 14 licensed SBLCs over the span of 40 years. Originally this moratorium had only gone into place because the SBA “did not have adequate resources to effectively service and supervise additional SBLCs” but now in modern times the SBA has determined there’s a problem, “that certain markets where there are capital market gaps continue to struggle to obtain financing on non-predatory terms.” Their solution? Lift the moratorium.

The proposal was published on November 7th and the public’s ability to comment ends on January 6th. One potential outcome of lifting the moratorium is that fintechs could potentially become licensed SBLCs. That appears to be a desired outcome for Funding Circle who shared their comment on social media on Wednesday.

“We need the SBA to lift the SBLC moratorium in order for us to apply to originate 7(a) loans nationally,” Funding Circle wrote. “This would allow us to leverage our platform technology and more than a decade of lending experience to expand access to 7(a) loans for underserved communities and to do so quicker, at a lower cost and with a superior customer experience.”

With more than 60 comments garnered on the proposal so far, Funding Circle is virtually the only fintech to have weighed in at all. A number of comments from the traditional finance realm were highly critical of the idea of allowing fintechs to become SBLCs, citing their supposed inexperience and perceived failures to responsibly dole out PPP funds. Others expressed a belief that the SBA still did not have the resources necessary to supervise additional SBLCs even after 4 decades and that the agency is already stretched too thin as it is.

“SBA should not expand 7(a) Program until it requests, and receives from Congress, an appropriation to fund the additional SBA staff necessary to supervise additional 7(a) lenders,” the American Bankers Association wrote.

There are complexities and nuances to the pros and cons of the arguments, but the opportunity to comment at all is running out. The deadline is Friday January 6th.

Anyone can submit their own comment here.

Update: Upstart, another fintech, had their comment processed by the SBA after this story was posted. The company also supports lifting the moratorium.

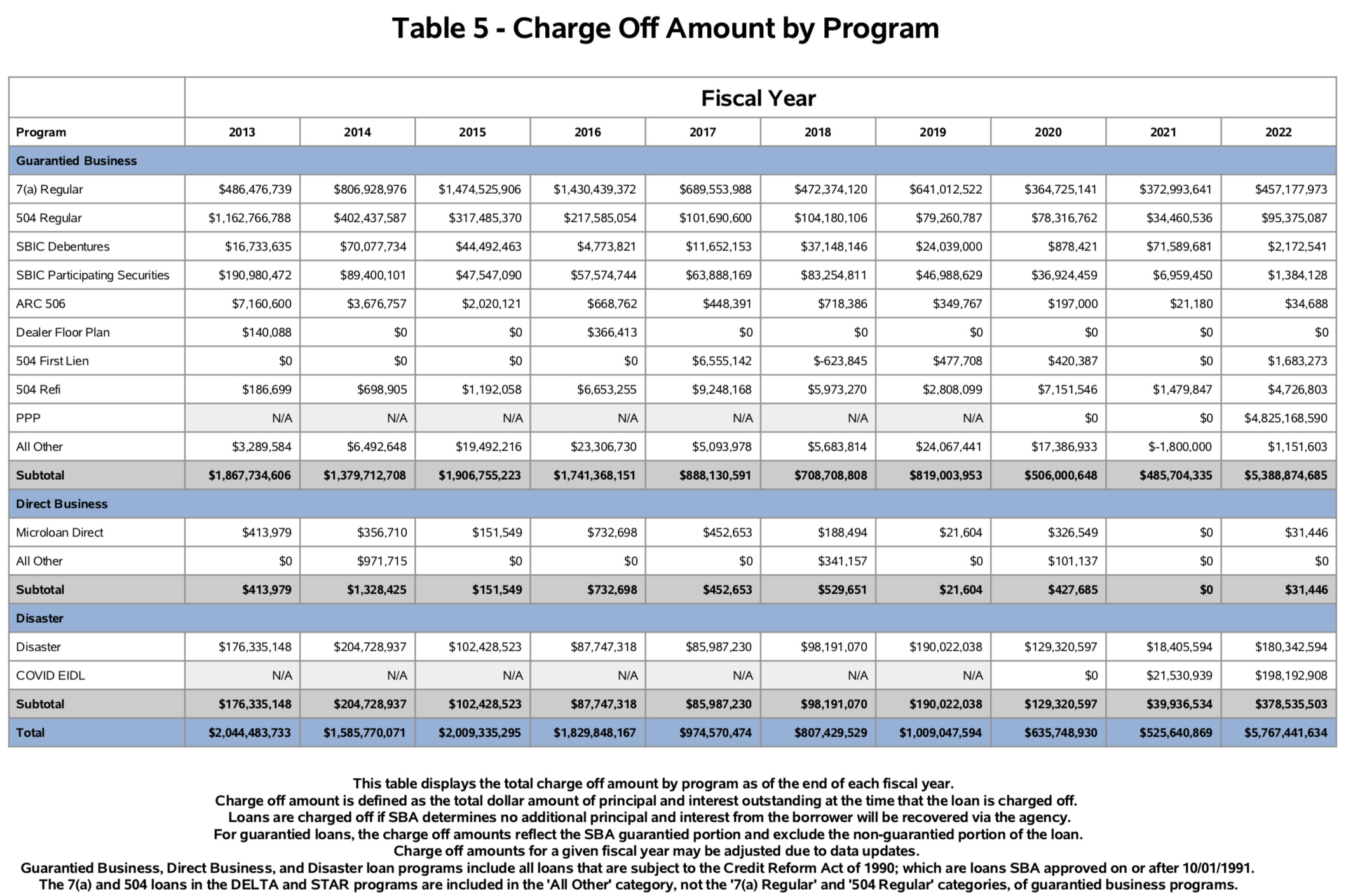

$220M Worth of EIDL Funds Already Charged Off

January 2, 2023 It’s a small sum compared to the total outstanding principal balance, but $220M worth of covid-related EIDL funds had already been charged off as of SBA fiscal year-end 2022. That year-end of September 30th is before almost any borrower was required to make even one payment on the 30-year loan. The total outstanding principal balance net of charge-offs was $358B at the time.

It’s a small sum compared to the total outstanding principal balance, but $220M worth of covid-related EIDL funds had already been charged off as of SBA fiscal year-end 2022. That year-end of September 30th is before almost any borrower was required to make even one payment on the 30-year loan. The total outstanding principal balance net of charge-offs was $358B at the time.

The SBA originally allowed a 30-month deferment on EIDL payments and just recently began offering an additional six-month deferment to eligible borrowers if they need it. Making payments at all can be a little bit complex in that of itself, however.

It remains to be seen how covid-era EIDL borrowers will perform. The SBA charged off $457M in just 7(a) loans in 2022 alone, for example, so the figures on the EIDL are not that material yet. In the years before covid, the SBA was regularly charging off between $800M-$2B/year in loans total. However, it is unlikely that a significant number of them defaulted before the first payment was even due.