Archive for 2020

Kabbage Launches Checking Accounts for SMBs

July 22, 2020 Today Kabbage announced the launch of its latest service, business checking accounts. Targeting small-sized businesses and offering no monthly fees, 1.10% APY, and a Kabbage debit card; Kabbage Checking is available now and is part of an effort by Kabbage to transition from being a pure SMB-funding company into a cash-flow management company.

Today Kabbage announced the launch of its latest service, business checking accounts. Targeting small-sized businesses and offering no monthly fees, 1.10% APY, and a Kabbage debit card; Kabbage Checking is available now and is part of an effort by Kabbage to transition from being a pure SMB-funding company into a cash-flow management company.

“Kabbage is a full financial services platform that’s focused on solving on cash-flow management for small businesses.” President Kathryn Petralia explained in an email. “A business checking account is a core function of how they manage their money, and we saw an opportunity to build them a solution specifically designed for them – while simultaneously reducing their costs and increasing their yield.”

Launched in the wake of a study which reports that over 40% of small businesses are looking to change their bank following struggles with their Paycheck Protection Program applications, Kabbage is optimistic that fintechs an online lenders will benefit from a wave of interest following the failures of financial institutions in the face of the coronavirus.

“Amidst one of the largest financial crises in history, we helped over 225,000 small businesses access services many of their long-time bank partners would only provide to their largest customers,” the President said in a statement. “We believe in the businesses too often left out, overlooked, and underestimated. Kabbage Checking is a new banking service built to give those small businesses an upper hand to earn more, save more, and grow their business faster without sacrificing anything they expect from a bank.”

WATCH: NY State Senate Banking Committee Debates The Commercial Finance Disclosure Bill

July 22, 2020The New York State Commercial Finance Disclosure Bill passed through the senate banking committee yesterday, but not until some debate over the merits of it took place. You can watch the full discussion by the Senate Banking Committee below:

The Aftermath: What Industry Experts Had to Say About The Future Alignment of People and Data

July 20, 2020

Like never before, the ways in which people and data are employed are overlapping more in a post-covid economy. Nearly three months of slow-down and, in some cases, complete economic shutdown have forced brokers and funders alike to view businesses differently than before. New documents, metrics, and terms are being incorporated into underwriting with the belief that it will provide a much more comprehensive picture of each business applying for funding.

Broker Fair Virtual took the chance to explore these new perspectives in The Aftermath, a panel featuring Moshe Kazimirsky, VP of Strategic Partnerships and Business Development at Become; Heather Francis, CEO of Elevate Funding; and David Snitkof, Head of Analytics at Ocrolus. Here, the industry experts discussed what the future of data and people may look like, what the new things that funders are looking out for are, and how the coronavirus has changed consumer and merchant behavior.

First up was Heather Francis, who gave a run down of how Elevate has adapted to the constantly shifting environment created by covid-19. “There were slim pickings on what we could fund,” Francis noted of the early lockdown period. Explaining that many businesses didn’t fit their criteria in the early days of lockdown, Elevate began the process of including new metrics and lenses through which to ascertain if businesses were financially viable.

National, state, and local restrictions became a daily check-in, rather than monthly; with one person being assigned to cover changes in local and even county regulations. As well as this, Francis explained that the company shifted its focus from underwriting the business owner’s activity to underwriting the consumers’ activity. This meant that foot traffic was constantly reviewed via FourSquare, trends that showed which industries were seeing upticks and downturns were monitored, and what customers in varying geographies were comfortable with was gauged.

“There are some areas in our country that were not heavily impacted,” Francis explained, commenting on the discrepancies between locations, particularly for bars and restaurants. “I know some of us have our optics on what’s going on in our daily lives, and a lot of people in our space are located in New York or California, and these were the very heavily regulated areas where everything was shut down and there was not much to do. Here in Florida, it was easier, with open-seating dining.”

“There are some areas in our country that were not heavily impacted,” Francis explained, commenting on the discrepancies between locations, particularly for bars and restaurants. “I know some of us have our optics on what’s going on in our daily lives, and a lot of people in our space are located in New York or California, and these were the very heavily regulated areas where everything was shut down and there was not much to do. Here in Florida, it was easier, with open-seating dining.”

David Snitkof echoed Francis’s points, saying that “the old way of businesses underwriting credit is no longer sufficient … If you were to only look at people’s repayment histories, their credit profiles, and things like that, you wouldn’t get all the data you need to make the right decision. Generally there’s this idea that the past is prologue and the greatest predictor of future results is past behavior, and this type of pandemic makes that no longer the case … we need to think beyond the traditional data sets that people have used to underwrite credit.”

According to Snitkof, the old models for underwriting and funding have been overturned, with funders adhering to three principals going forward as they chart new methods: more data, more time, more detail. This means incorporating more data and analytics than before, pushing for more data-driven strategies; requesting information and data from merchants that cover longer periods of time, with the hope of gaining further insight into the pattern of the business; and upping the thoroughness with which each merchant is scrutinized, recording more information that is unique to their industry, location, and business management.

“Lenders will realize that in order to make a credit decision, we need to have access to very deep, detailed, and wide time-framed data of our customers; and we need to be able to process it in an automated and efficient way,” Snitkof asserted.

Still, while it looks like data is due to play a larger role in the future, Heather Francis took care to mention that important data is currently missing from their metrics. Credit and delinquency reporting are on hold, just as rent is paused for many tenants; meaning that in two or three months, many funders could be in for a surprise when they realize their merchant is having trouble.

Speaking on the Paycheck Protection Program as well as the Economic Injury Disaster Loan, both Snitkof and Francis expressed that while it is good to see deposits for the government programs, questions must be asked regarding them. They can’t be viewed as revenue, since they do not reflect a business’s ability to generate revenue, said Snitkof, but rather they offer a chance to view how a company manages its cash-flow, with how they spread out PPP and EIDL funds being a key insight.

Speaking on the Paycheck Protection Program as well as the Economic Injury Disaster Loan, both Snitkof and Francis expressed that while it is good to see deposits for the government programs, questions must be asked regarding them. They can’t be viewed as revenue, since they do not reflect a business’s ability to generate revenue, said Snitkof, but rather they offer a chance to view how a company manages its cash-flow, with how they spread out PPP and EIDL funds being a key insight.

Looking forward, the panelists noted that the experiences of economic shutdown; PPP; EIDL; and how many business owners’ banks supported, or did not support, them could lead to a shift in how non-banks are viewed.

“It’s definitely a time and place for us to really highlight how our industry is placed to assist small businesses,” Francis stated. “We should really take this opportunity to expand on what we can do and how we can help. I think it’s our moment to shine because a lot of banks have pulled back on what they’re able to do in this time.”

This pulling back by banks became clear during the peak of the PPP application period, when many business owners complained of a lack of or poor communication between themselves and the bank they applied to. Highlighting the importance of the customer experience, Snitkof pointed out that this aspect of alternative finance may only become more important as time goes on.

“We have this golden age of customer service. Customers are going to demand good funding, on the right terms, with full transparency, with good speed of decisioning, with a good relationship, and if they can get that from someone who is not a bank, but is an alternative finance provider, then that’s a great funding scenario for them.”

More generally though, the panel ended on a note of ambiguity over the future, with the speakers agreeing that what comes next will be uncertain and challenging, as Francis reminded the audience of what 2020 has in store: a presidential election and a possible second wave of the novel coronavirus.

But there may also be opportunity for those who are there to take it, according to Snitkof, who finished off by saying that “the silver lining of what we’ve just been through as a country, as a world, as an industry, is that all those things that were good enough, they were on pause. So it’s given people the time and space to reimagine what they could do and actually look at the capabilities that we’ve available to us and say ‘maybe we can provide a great personalized customer experience to every small business and customer out there. Maybe we can be more automated and data-driven in our decisions. Maybe we can actually extend better terms on financing to people because we’re able to determine risk better, and optimize our market spend and cost of capital better.’ One of the good things about a disruption is it takes away a lot of the stuff that was good enough; a lot of those sacred cows are now ready to be disrupted and maybe in a few years we’ll see rapid innovation along those lines.”

New York State Legislators Resume Push of Commercial Finance Disclosure Bill

July 17, 2020 A bill (A10118A / S5470B) intended to create uniform disclosures for comparison purposes while also placing control of the commercial finance industry under the purview of the superintendent of the New York Department of Financial Services, is moving forward.

A bill (A10118A / S5470B) intended to create uniform disclosures for comparison purposes while also placing control of the commercial finance industry under the purview of the superintendent of the New York Department of Financial Services, is moving forward.

The March 2020 initiative was picked back up this week by members of the Assembly where it passed the banking committee and codes committee on a unanimous and bipartisan basis.

“When enacted, this bill will become the strongest commercial lending disclosure law in the country that covers all commercial financing products,” wrote Ryan Metcalf, Head of US Regulatory Affairs and Social Impact at Funding Circle, on LinkedIn. “It includes strong provisions that ensures enforcement and eliminates loopholes that will prevent gaming & abuse, & requires APR to be disclosed for all products.”

Metcalf further wrote that they and the Responsible Business Lending Coalition (RBLC) have been working diligently with NY state legislators for the last year or so to craft this bill. Among RBLC’s membership is Fundera, Nav, Lendistry, LendingClub and about 4 dozen other companies.

7/17 Update: OnDeck Still Negotiating Workouts With Creditors

July 17, 2020This morning, OnDeck disclosed that it was still actively engaged in securing workout arrangements with its creditors.

For its corporate debt facility, OnDeck’s lenders consented to an additional two week extension on the increased monthly principal repayments that OnDeck is required to pay as a result of the company’s covid-impacted portfolio triggering a rapid payout event. The circumstances mean that OnDeck has to make millions of dollars in loan payments but temporary workouts like these are enabling the company to slow them down.

OnDeck’s asset-backed revolving debt facility, meanwhile, has been spared the consequences of a borrowing base deficiency under a renewed agreement to suspend any designation of such to at least through August 18th.

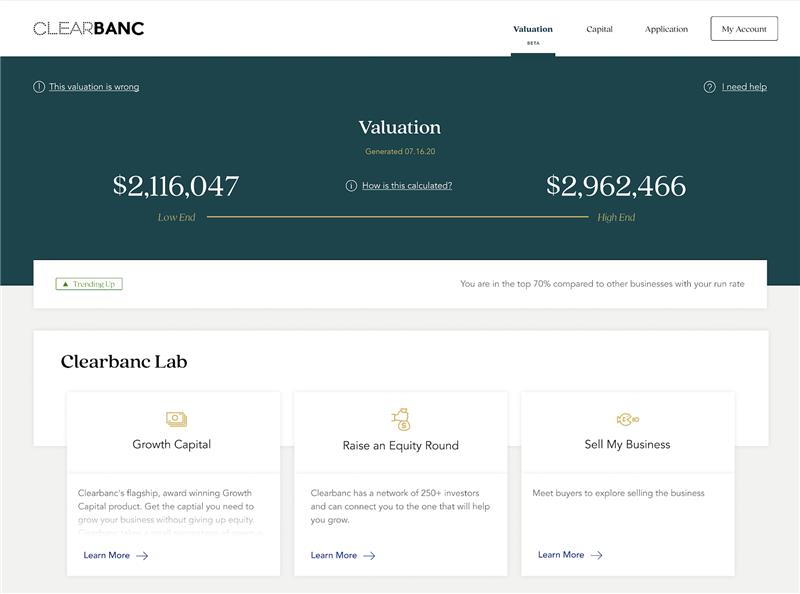

Clearbanc Launches Valuation Service for Founders

July 16, 2020

Today Clearbanc, the Toronto-based alternative finance company, has launched its latest service, Valuation, allowing founders to gauge their company’s value. Being an extension to Clearbanc’s platform, the service will be free to everyone and promises an estimation within 24 hours that can be checked weekly.

Valuation also offers three options to founders upon receiving their company’s value: the chance to access capital via Clearbanc’s funding channels, connect with investors in order to raise an equity round, and investigate possible acquisition opportunities. For the last two of these options, Clearbanc makes introductions to a selection of venture capital investors that have connected with the program.

As per the requirements, founders will have to connect a selection of private data points. Their business accounts, payment processor, accounting platform, and their admin account will all be required. As well as this, public data is also used to arrive at a valuation, basing the estimations on information specific to the company as well as the industry it is in.

“We think this could be as revolutionary as what Credit Karma did when they launched free credit scores for everyone and gave consumers access to their own information,” explained Clearbanc CEO Michele Romanow. “We’re really excited about this as it represents our first non-capital launch, and we think that it’s part of a much bigger vision of how we help founders win in this environment.”

Maxim Commercial Capital Funds Deals in 30 States During 2Q 2020

July 16, 2020Maxim Commercial Capital is pleased to report it funded hard asset-secured financings for small and mid-sized businesses (SMBs) in 30 states across the United States during the second quarter of 2020. After pivoting quickly in March to safer-at-home working conditions for its 30+ team members, Maxim experienced a steady increase in applications from equipment brokers and vendors for their borrowers with challenged credit. Maxim lends $10,000 to $3,000,000 to SMBs nationwide secured by heavy equipment and real estate to facilitate asset purchases, working capital and to refinance expensive short term debt.

“Maxim was founded during the Great Recession of 2008,” noted Behzad Kianmahd, Chairman and CEO. “We are applying our experiences gained during that time to overcome today’s extraordinary economic challenges and long term uncertainty caused by the COVID-19 pandemic. We have reaffirmed our commitment to finance SMBs, which are the backbone of our economy, refreshed our underwriting standards, and are continually improving our infrastructure by investing in technology and communication tools for the benefit of our customers, vendors, brokers and team members.”

During the second quarter, Maxim received numerous applications from business owners with strong credit but negative cash flow due to the economic downturn. Funded transactions for such borrowers included $95,000 secured by a 2019 Mack GR64F Tri-Axle Dump Truck for a growing landscaping company in New Jersey; $42,500 for a seasoned contractor’s purchase of a 2014 Caterpillar 312E Hydraulic Excavator; and, $29,000 to enable a business started up by seasoned contractors to purchase a 2020 Reinert ZR Concrete Pump.

Buyers of used class 8 trucks faced numerous challenges during the second quarter, ranging from lenders shutting down without warning to closed DMVs. Maxim successfully funded deals across the country, including $26,500 for a California-based long-haul truck owner-operator to purchase a 2017 Volvo 780; $20,800 for an Ohio-based transportation company to purchase a 2017 Freightliner Cascadia; and, $23,000 for a Texas-based owner-operator to purchase a 2016 Freightliner Cascadia to replace a truck with mechanical issues.

“We are humbled and encouraged by our team’s commitment to positively impact our customers’ future success, and by our customers’ continuous effort to make tough but rational decisions to stay in business during these difficult times,” commented Michael Kianmahd, Executive Vice President. “Based on our experience over the past few months, we are confident that SMBs across the nation will contribute substantially to the nation’s recovery from the biggest economic shock since The Great Depression.”

About Maxim Commercial Capital

Maxim Commercial Capital helps small and mid-sized business owners seize opportunity by providing financing in amounts up to $3,000,000 secured by heavy equipment and real estate. Maxim facilitates equipment purchases, provides working capital and refinances debt for companies across all industries located nationwide. Through Maxim’s tailored financing programs, businesses unlock capital tied up in underleveraged assets, often replacing expensive short-term debt and daily repayment working capital loans with longer term capital. As a leading provider of transportation equipment finance, Maxim funds up to 75% of the acquisition cost of class 8 and class 6 trucks, trailers and reefers for owner-operators and small businesses. Learn more at www.maximcc.com or by calling 877.776.2946.

The Shakeup’s Impact on Stock Prices

July 15, 2020