Archive for 2018

deBanked Connect – Miami (Recap)

January 30, 2018Thank you to everyone who attended our cocktail networking event in South Beach last week. It was a great opportunity for funders, lenders, brokers and others in the industry to connect with each other (many for the first time ever). Thank you again to Everest Business Funding, National Funding, Knight Capital Funding, NISO, Grand Capital Funding, and Venture Credit Solutions for sponsoring.

Below is a sample of our photos from the evening. If you attach any of your own on social media, please use #debankedconnect so that we can find them.

READY FOR AN EVEN BIGGER & MORE COMPREHENSIVE DEBANKED INDUSTRY EVENT?

BROKER FAIR IS COMING MAY 14, 2018

TO BROOKLYN, NY

JOIN FUNDERS, LENDERS AND BROKERS FOR THE INAUGURAL CONFERENCE

LEARN MORE HERE

CHECK OUT THE BIG NAMES SPONSORING BROKER FAIR 2018

Attorney Suing Dozens of MCA Companies Disqualified as Counsel

January 29, 2018 Rayminh Ngo, an attorney with Higbee & Associates that has appeared in no less than 80 lawsuits against merchant cash advance companies in New York State, hit a fatal roadblock in one case, court records reveal. That’s because Ngo and Higbee aren’t qualified to practice law in the State of New York. This disturbing matter was brought to light and evaluated by the Honorable Jerome C Murphy, a judge in Nassau County, late last month.

Rayminh Ngo, an attorney with Higbee & Associates that has appeared in no less than 80 lawsuits against merchant cash advance companies in New York State, hit a fatal roadblock in one case, court records reveal. That’s because Ngo and Higbee aren’t qualified to practice law in the State of New York. This disturbing matter was brought to light and evaluated by the Honorable Jerome C Murphy, a judge in Nassau County, late last month.

Platinum Rapid Funding Group, the plaintiff against a party that Ngo was representing, argued that the defendant’s attorney was in violation of Judiciary law §470, specifically that Ngo and the law firm did not have an office in New York State and consequently could not represent a client in New York.

Ngo denied the assertion and argued that he did in fact have offices there. But the evidence was not on his side. The two addresses he provided turned up empty, according to process servers who visited both locations. And the lease agreements submitted as exhibits were not valid for the time period in question.

“In the end, this Court finds that there is no evidence on this record that Ngo and Higbee had physical addresses in New York,” the order on the matter read. Ngo and Higbee were therefore disqualified as counsel of record. They have filed a notice of appeal in response.

That he has appeared in dozens of other lawsuits in the State was not addressed in the order, but it may be worth noting to his opponents both past and present that pursuant to this Court, they cannot practice in New York.

You can view the decision here.

The decision arose in Platinum Rapid Funding Group, Ltd. v. H D W of Raleigh, Inc. d/b/a Pure Med Spa, a/k/a Pure Cosmetic and Surgical Center and Holly Donielle Wybel a/k/a Holly D. Wybel, Index # 605890/2017 in New York Supreme Court.

BFS Capital’s Marrache on Canadian Small Business Landscape

January 28, 2018

It’s been about five months since Michael Marrache took the reins as CEO of BFS Capital. He spoke with us then about the company’s algorithmic solutions, ISO relationships and product pipeline. He recently took some time to talk with deBanked about the key themes in the Canadian market in 2018 – from minimum wage, to the impact of US tax reform on the Canadian economy, to ISO opportunities — and BFS Capital’s role there.

deBanked: When did BFS Capital begin operating in Canada?

Marrache: BFS Capital funded its first loan in Canada in 2012. Traditionally, we have approached Canada’s market via our partner channel, both US and Canada based. We plan on increasing that effort in 2018.

deBanked: Is Canada a market that BFS Capital recognizes as growing?

Marrache: Canada is a growing market for BFS Capital, though our non-US markets, including Canada and the UK, currently represent less than 20% of our global $300 million in financings. We see significant upside in both Canada and the UK in the next 12 months.

deBanked: What are the themes as you see them for Canadian small businesses and BFS Capital in 2018?

Marrache: There might be more insecurity among Canadian small businesses this year. The 2018 minimum wage increase to $14 an hour in Ontario, expected to rise again in 2019, for example, might cause some small businesses to have to cut hours or reduce staff to make up for the expense. They may have to raise their prices, which could impact demand.

Additionally, recent policy and legislative changes in the US could also impact Canada. For example, tax reform in the US, specifically a reduction in the US corporate rate, will put the US on par with Canada in terms of tax rates and similar burdens. At the same time, US regulations are being reduced while Canada’s appear to be increasing. All of this is part of the current US government’s initiative to drive domestic business growth and we are not sure how it will affect Canada’s economy, business confidence and consumer spending.

The Canadian dollar is also forecast to remain weak and might continue to fall for a while longer. With US tax reform potentially boosting the economy here, the US Fed is likely to raise interest rates, which might reduce demand for the Canadian dollar. The CAN$ could further slide if Bank of Canada cuts rates again. [Scotiabank]

At the core, however, Canada has 1.1 million small businesses. Not a small number. There were more than 350,000 small businesses created in Canada in 2016 and 42% of job creation in the country in the past decade stemmed from firms with fewer than 100 employees (CIBC Capital Markets). These businesses need working capital for a variety of needs related to their everyday business and, importantly for where we fit in, it has traditionally been difficult for small businesses to obtain financing from banks.

BFS Capital financing has come into the mainstream because it’s more accessible than a bank loan, less expensive than equity, and less risky than bootstrapping. Our financing solutions also require less commitment than taking on a partner or getting venture capital. Moreover, the few big banks in the market have tended to shy away from small businesses, so we have seen an opportunity with our ISO partner-base and directly, for our lending solutions.

Today small businesses in Canada can get the money in their account in just a day or two and there are a variety of products with different rates and payment options. As the market in Canada gets more competitive the rates will continue to go down.

deBanked: The last time I spoke with you, you talked about automated solutions, transparency tied to ISOs and company culture. Are these at the forefront of the Canadian business as well? Explain.

Marrache: Yes. These initiatives are embedded in the company strategy at the top. We believe speed is required but not sufficient; the company must lead with a culture of service and transparency. We are also investing in data science to improve risk profiling and process efficiencies for every partnership and every financing, including in Canada. These initiatives have been instrumental to our strengthened partnerships in the US and we expect these to benefit our Canadian partners as well.

deBanked: Can you provide any illustration of the number of Canadian merchants on the BFS Capital platform or the amount in loans or MCAs you’ve deployed in the country?

Marrache: Although at a more modest volume than our business in the US, since entering the Canadian market in 2012, BFS Capital has achieved originations growth of approximately 100 percent on a compounded annual growth basis.

Liberty Lending Partners With MetaBank

January 28, 2018

Online lender, Liberty Lending has partnered with MetaBank, a wholly-owned subsidiary of Meta Financial Group, Inc., the latter announced on Thursday.

During the three-year agreement, the federally chartered MetaBank will provide personal loans to Liberty Lending customers. Both entities will market the initiative.

According to the release, Meta expects to originate between $500 million and $1 billion in personal loans.

Eligible loans will be closed-end installment products ranging from $3,500 to $45,000 with durations lasting between 13 and 60 months.

“We are excited to partner with a respected and growing brand in online lending, and look forward to working together to deliver best in class loan products to consumers,” said Brent Turner, EVP and head of consumer lending at Meta, via release. “Furthermore, leveraging the underwriting expertise and consumer credit experience of the SCS team provides us with great resources to accomplish our objectives in consumer credit.”

“Liberty Lending’s mission is to provide innovative borrowing solutions to deserving customers. The partnership will enable Liberty Lending to further deliver on its mission to customers by leveraging Meta’s wealth of resources and expertise,” said Bill Yialamas, CFO of Liberty Lending.

Meta Financial Group is based in Sioux Falls, South Dakota while Liberty Lending is headquartered in New York, New York.

StrategyCorps: The ‘Amazon Prime Effect’ Could Significantly Alter Personal Banking

January 26, 2018 FinTech and mobile content has done more than provide exposure to alternative lenders and financing avenues.

FinTech and mobile content has done more than provide exposure to alternative lenders and financing avenues.

“It’s rewiring the way that we think,” Dave DeFazio, a partner at StrategyCorps told deBanked while discussing mobile devices. StrategyCorps helps financial institutions enhance their checking account offerings.

“We’re addicted to our phones. We’re using them more than ever. The winners in whatever category of business will be the ones that connect better with their customer’s mobile lifestyles and behaviors.”

DeFazio believes that even the flagship personal banking product, the checking account, could be facing a significant makeover in the not-so-distant future.

“There are companies that are kind of nibbling away at the strangle hold on the definition of the traditional account,” said DeFazio. He added that while the public tends to define their banking relationships now by which bank holds their personal checking account, things could be different “down the road.”

Citing a white paper that StrategyCorps commissioned, DeFazio also pointed to deposit displacement as a potential cause of alarm for traditional free checking.

Easy mobile access to P2P platforms such as Venmo, make it more convenient for traditional banking users to opt to store their funds elsewhere.

Another company “nibbling away” at funds that would otherwise be deposited in a traditional checking account is Amazon.

According to Reuters, the e-commerce giant leant more than $1 billion to over 20,000 small businesses operating via Amazon Marketplace between June of 2016 and 2017.

The loans range from $1,000 to $750,000.

The results from this venture could prompt Amazon to purchase a small or mid-sized bank of its very own in the next 12 months.

“This may either be a tactical move or a broad strategic jump into banking, as Amazon seeks more stickiness with consumers and small businesses in consumer lending such as auto loans, credit cards and home mortgages,” CFRA bank analyst, Ken Leon, told Bloomberg in December.

DeFazio says that as consumers grow accustomed to whatever unique perks and advantages that Amazon and other platforms bring to the table for products such as a personal checking account, it could force traditional institutions to work much harder to stay attractive.

deBanked Afterparty in Miami (Please read if you are planning on attending our event tonight)

January 25, 2018 Thank you so much to everyone who is attending our event tonight!

Thank you so much to everyone who is attending our event tonight!

The interest has exceeded all of our expectations… and the hotel’s.

That’s why we’re planning on heading across the street after 8:30PM (when our event ends) to the Delano at 1685 Collins Avenue for continued networking!

Funders, ISOs, if you were not registered through EventBrite tonight or if you’re registered and want to continue connecting with the industry, we’ll be happy to see you after 8:30!

Thanks again for all the continued interest. We have been receiving all your calls, emails and texts about trying to squeeze in to the Gale rooftop tonight. Unfortunately, there are capacity issues that prevent us from making last minute exceptions.

See you at The Gale 5:30 – 8:30. Open bar. Must be RSVP’d.

See you at the Delano across the street after 8:30 (On the main floor and out back on the deck)

Sorodo’s Co-Founder: Alternative Financing Options ‘Unknown’ Amongst the U.K.’s Small Business Community

January 25, 2018Are small businesses across the pond aware of their alternative financing options? Manchester’s Sorodo Limited, a merchant cash advance company, feels that the word has far from spread.

“We still have some way to go, as the product is still fairly unknown to the wider business community,” co-founder Rich Wilcock said via release earlier this month while discussing merchant cash advance alongside other non-traditional avenues. “We spoke to a lot of business owners in 2012 and 2013, and they were understandably frustrated by their situation. Many who were declined for traditional forms of finance by their banks didn’t look any further, which is why it’s so important we get the message out about alternative funding options, such as peer-to-peer lending, cash advances, crowdfunding, unsecured borrowing and so on.”

Wilcock labeled awareness of the merchant cash advance option and other alternatives at the dawn of 2018 as “disappointingly low.”

Typical Sorodo Limited customers include owners of hotels, restaurants, cafes, pubs, clubs, bars, independent shops (including e-commerce stores), convenience stores, beauty salons and garages.

“In 2014, the average independent retailer was struggling to stay open, let alone turn a profit,” said Wilcock. “Many shops, hotels, restaurants and leisure outlets closed down, but we knew this product had the ability to not only keep businesses trading but also to help them grow.”

After promoting the lending alternative and seeing growth in Sorodo’s business, Wilcock believes that there is still significant amount of campaigning left to do. Thus, Sorodo Limited is expanding it’s offerings with a new platform called Capalona.

The newcomer is designed to help U.K. business owners find alternative solutions besides merchant cash advance that may serve their individual needs better.

“The term ‘alternative business finance’ covers a variety of new funding models that allow businesses to access funds that are not readily offered by traditional lenders,” said Wilcock. “These include products such as asset-based lending, invoice finance, venture capital, pension-led funding and many more.”

Capalona, which is currently up and running, is also based in Manchester.

MCA Helpline, A Debt Settlement Company, is Sued For Tortious Interference

January 25, 2018

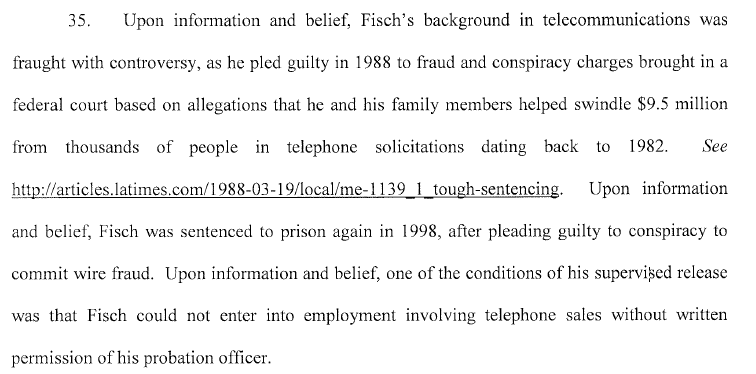

Debt settlement is under fire again. This time it’s a trio of defendants, namely MCA Helpline, LLC, Decision One Debt Relief, LLC and Todd Fisch individually, according to a complaint filed by plaintiff Everest Business Funding on Wednesday in Broward County, Florida.

Everest is seeking damages for Defendants’ tortious interference with at least a dozen of its merchant contracts.

“Defendants have engaged and continue to engage in the business practice of making misleading representations to Everest’s customers; namely, promising to save the merchants money on their existing contracts with Everest when they have no intention or ability to uphold such a promise,” the complaint states. “In so doing, Defendants tortiously interfere with Everest’s merchant agreements by inducing the merchants to breach their contractual obligations to Everest in favor of entering a new payment relationship with the debt relief company.”

Fisch is alleged to be the mastermind behind both MCA Helpline and Decision One Debt Relief.

Complicit ISOs were also put on notice. “To the extent any specific ISOs or their affiliates who have ISO Agreements with Everest have leaked information about Everest’s merchants to Defendants, or to any other third party, such conduct constitutes both a breach of the ISO Agreement and tortious interference with Everest’s merchant contracts,” it reads. “Through the course of discovery in this lawsuit, Everest plans to add as additional Defendants, as yet unidentified ISOs, which have been working with Defendants to target Everest’s merchant accounts in violation of their contractual agreements.”

Everest has been vigorously pursuing debt settlement companies. In September, they, along with Yellowstone Capital, filed a lawsuit against eight defendants (later amended to include 1 more) in New York.

Another lawsuit examining similar issues was also filed last year in New York. In Pearl Gamma Funding and Pearl Beta Funding v Creditors Relief, Pearl tacked on a defamation claim in addition to tortious interference. That case is still pending.

{kind=link}

.JPG){kind=link}