A Glimpse into Square Capital’s Marketing

As a merchant, Square has marketed their Square Capital program to me before. But this is the first time I’ve received direct mail marketing from them. Here’s a snapshot of what that looks like:

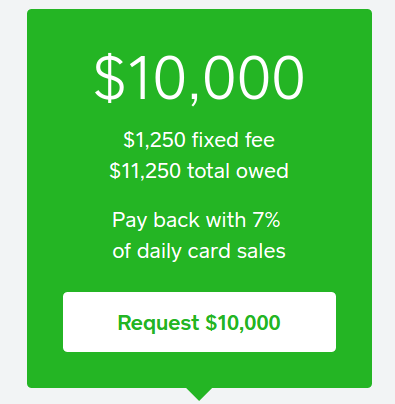

To view the potential offers, merchants are directed to log in to their Square accounts where they will see multiple terms. Even though their particular product is a loan made possible through Celtic Bank, all of the proposed loan offers are presented using the Total Cost of Capital method. That means cost is disclosed as a precise dollar amount so that potential borrowers will know exactly how much they will have to pay. Several studies have indicated that this is the easiest to understand, though it has been subject to some debate.

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

“There are no ongoing interest charges for your loan, only the one-time upfront fee that is listed as a dollar amount,” the Square Capital FAQ page states. “The total cost of the loan is a fixed fee and the total amount owed never changes.”

One of the defining features that makes Square Capital’s loan product different from a merchant cash advance or a purchase of future sales, is that Square enforces a fixed 18 month term. “If the loan hasn’t been repaid in full at the end of 18 months, the remaining loan balance will be due in full,” they state. That is completely unlike a purchase transaction in which there is no deadline or term. Even MCA purchase transactions that stipulate fixed daily payments do not actually have fixed terms. That’s usually because if a merchant’s sales activity rises or falls, they have the contractual right to request an adjustment to those payments to effectuate the basis of the agreement, that future sales be delivered in accordance with the unpredictable ebb and flow of business. That makes the date in which delivery will be satisfied in full unknowable. It’s that unknowable that can cause MCA transactions to be more expensive than their loan counterparts, though that is absolutely not always the case.

For Square, unknowable contract satisfaction dates likely made it difficult to bundle these deals up to sell off to institutional investors. Square Capital head Jackie Reses articulated this challenge during her appearance on an April 2016 LendIt stage. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date,” she said.

Even institutional investors recognize and understand that MCA purchase agreements do not have fixed terms.

Last modified: October 20, 2016Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.