Is NAMAA Reborn? Meet the Small Business Finance Association

Almost seven years ago exactly, the North American Merchant Advance Association announced their presence. As of today, they are now officially the Small Business Finance Association (SBFA). Back then, a release dated April 15, 2008 stated:

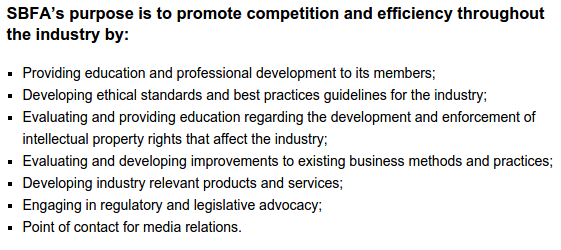

The North American Merchant Advance Association, Inc. (NAMAA) has recently been created to represent merchant cash advance providers and to promote competition and efficiency throughout the merchant advance industry. NAMAA’s members will have the opportunity to share industry education and professional development, ethical standards and best practices guidelines, the development of industry relevant products and services, and the engagement in regulatory and legislative advocacy.

Of the ten original members, a handful are no longer operating. NAMAA’s membership in 2008 arguably encompassed the entirety of the merchant cash advance industry sans AdvanceMe (now named CAN Capital). Today, the SBFA website currently lists seventeen members. The organization has clearly grown but it pales in comparison to the size of the industry in 2015.

Internal data indicates that there are well over one hundred direct providers of merchant cash advance. Several hundred more are ISOs/brokers that co-invest in merchant cash advance transactions (Strategic Funding Source has had more than 200). And there are more than one thousand ISO/brokers that resell the product nationwide.

On this basis alone, less than two percent of industry providers and resellers are members of the trade organization. Granted, the seventeen member companies likely make up at least 15% of the industry’s funding volume. Member company Merchant Cash and Capital for example, announced just last month that they had funded $1 billion since inception.

Some have viewed the organization’s membership as overly exclusive and resistant to change. A seasoned veteran of an ISO that wished to remain anonymous said prior to the organization’s announced changes that, “NAMAA served a purpose for a long time but as the industry has changed, they have not.”

Ironically, Goldin’s statement in today’s release couldn’t be any more well timed. “With the alternative financing industry growing exponentially into a multi-billion dollar industry, we felt it was time for the trade association to evolve with it and open itself up to all types of small business alternative financing providers hence the name change to Small Business Finance Association,” he said.

The shift clearly acknowledges the true dynamic of the industry’s growth, that it’s not all merchant cash advance anymore.

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

SBFA Vice President Jeremy Brown is quoted in the release as saying, “NAMAA started primarily as an association of merchant cash advance providers and has evolved into an association for all types of small business alternative financing – particularly those providers of business loans.”

But with lenders added to the mix of potential constitutents, is the SBFA a little light? The SBFA will now represent less than 1% of the companies selling or reselling merchant cash advances and business loans. In growing membership however, patience may perhaps be a virtue.

Jared Weitz, CEO of United Capital Source, said, “NAMAA is a beneficial association in the industry and should be choosy with who they let in.” As a broker, his company has historically not been eligible for membership.

Similarly, Chad Otar, Managing Partner of Excel Capital Management, whose company has also not been historically eligible for membership, said, “The aim of NAMAA is to help out our audience to understand and remember the information we stand for as funders and ISOs.”

Otar’s point belies a troubling trend, that many players in this industry disagree about what it is they stand for.

In a deBanked Magazine article, titled, Stacking: Is it Tortious Interference?, Robert Cook, Cathy Brennan, and Kate Fisher of Hudson Cook, LLP delved into the industry’s most polarizing debate, the practice of entering into a cash advance transaction or loan knowing that the merchant has one or more open cash advances or loans with a competitor. They wrote:

On one side are companies that only originate first-position deals. These companies generally include a clause in their contracts prohibiting the merchant from obtaining another merchant cash advance or loan until the company receives all of the future receivables it has purchased or is fully repaid. First-position companies view stacking as a threat to recovery of money advanced or loaned to merchants. On the other side are companies that routinely offer second or third-position deals. These companies argue that merchants with adequate cash flow to support additional advances should be free to obtain them.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Though I did not ask the SBFA directly if the practice of stacking is an immediate disqualifier for membership, the organization has long been known to advocate against it. In Year of the Broker, Goldin commented that stacking litigation is underway.

Lawyers at Hudson Cook, LLP echoed the same. “In the last several months, at least two first position companies have sued their stacking competitors, claiming that stacking constitutes tortious interference with contractual relations,” they wrote.

The lawsuits come on the heels of the International Factoring Association (IFA) ban on merchant cash advance companies, citing tortious interference as the main driver.

After meeting with board members from both associations, the decision was made to deny membership to merchant cash advance businesses. This decision was based on numerous complaints and increased scrutiny that could negatively impact the factoring industry. By distancing ourselves from the merchant cash advance industry, we hope to diminish the chance of potential legislation.

-Commercial Factor July/August 2014

With several merchant cash advance companies left high and dry by the IFA, a potential leadership void has been created.

“As every industry evolves and shapes itself, some sort of governance and guidance is always needed,” said Otar. “This guidance is something that NAMAA holds itself responsible for,” he argued.

“The question is, can they reestablish themselves as a powerful voice that demands respect?” asked an industry veteran on the condition of anonymity.

Goldin assured me that the updated version of the organization’s best practices guide will be a public document.

Industry brokers like Otar are eager to comply with an established code of conduct and play any role they can in its creation. “Most of the business driven industry-wide is brought in through various ISO channels, which are the ones responsible in presenting the product offered by the funders to the end client,” he said.

That enthusiasm may be resonating with the SBFA. Goldin communicated that they are working towards different types of memberships, hinting at the possibility that brokers might one day be extended an invitation to join.

“We are exploring different levels of membership / pricing,” Goldin wrote in an email.

For the right price, they will likely find a lot of eager applicants.

Last modified: May 5, 2015Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.