Announcements

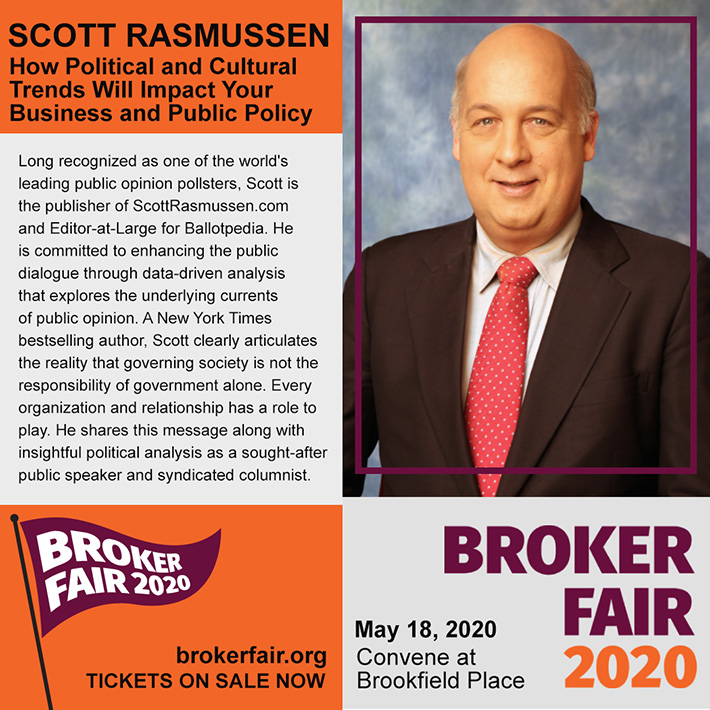

Broker Fair 2020 Announces Two Special Keynote Speakers

January 17, 2020Two special guests will speak at Broker Fair 2020 on May 18th in New York City. Scott Rasmussen and John Henry will complement a roster of leading professionals from the commercial finance industry. Broker Fair 2020 will be deBanked’s largest ever event.

TICKETS ARE ON SALE NOW AND EARLY BIRD PRICING IS STILL AVAILABLE!

TBF Financial buys $100 million of charged-off loans, leases and merchant cash advances from fintechs, banks, lessors

January 14, 2020DEERFIELD, IL, Jan. 14, 2020 – Commercial debt sales by fintech lenders, equipment leasing companies and banks are on the rise, with major companies striking deals to sell non-performing loans, leases and merchant cash advances after charge-off, reports Brett Boehm, CEO of TBF Financial.

TBF closed transactions in December totaling $100 million. The three largest deals were with a leading e-commerce company that acquired and liquidated a merchant cash advance business; a captive leasing company that provides financing for transportation equipment and other assets; and one of the 20 largest banks in the nation.

“One reason for the rise in commercial debt selling is the tremendous growth of online alternative lenders,” he explains. “As their business originations have increased, so have the number of accounts that eventually default. By selling commercial debt at charge-off instead of spending years trying to collect it, they can put that money back into making loans and merchant cash advances where they generate a much better return.”

“Other lenders and lessors also recognize that it is more productive to concentrate on their core business rather than chase collections past charge-off,” he adds. “Selling commercial debt provides immediate cash and allows collections personnel to focus on accounts that are more likely to be recovered, earlier in the past-due cycle.”

While the December deals may additionally reflect the eagerness of companies to bring in cash before year’s end, Boehm says prospective deals in the pipeline remain high in January, and he anticipates a busy first quarter 2020.

About TBF Financial

TBF Financial is the leading purchaser of non-performing equipment leases, commercial bank loans, online small business loans and merchant cash advances in the U.S. Founded in 1998, the company buys commercial accounts up to four years old from the date of last payment. This includes equipment leases, loans and lines of credit that have personal guarantees, no personal guarantees, are secured, unsecured, pre-agency, post-agency, pre-litigation, and reduced to judgment. For more information, visit tbfgroup.com or contact Brett Boehm, CEO at bboehm@tbfgroup.com, 847-267-0660 or via LinkedIn.

Media Contact:

Carla Young Harrington

Susan Carol Creative for TBF Financial

540.479.7835

CAN Capital Announces New CCO

October 15, 2019We are proud to announce that we have hired David Lafferty as CAN Capital’s new Chief Credit Officer (CCO.) Lafferty brings his expertise in commercial lending, business development, operational planning and profit & loss management to the CAN Capital team.

Lafferty has over twenty years of proven experience providing financial services to small businesses. He is the former Vice President of Capital Markets and Credit and Risk Management at Marlin Business Bank. In that role, he has assisted small businesses in obtaining the capital they need to operate and grow, with a special focus on helping businesses finance the lease or purchase of equipment. Lafferty is a graduate of Pennsylvania State University, and a member of the Equipment Leasing and Financing Association (ELFA) Small Ticket Advisory Council.

“I have focused my entire career on serving the small business owner as they are the backbone of the United States economy. Being given the opportunity to join this team in a time when the company is experiencing rapid growth and gaining significant market share is extremely exciting. I am really looking forward to joining an already very talented workforce as we take CAN Capital to the next level,” said Lafferty.

Ed Siciliano, CAN’s CEO, had this to say about the new hire: “I’m very excited to welcome Dave to CAN Capital. He will be joining a strong group of talented people focused on Risk and Credit Underwriting and applying his deep experience in small business lending to calibrate CAN’s 20-year proven credit models. We all welcome Dave and feel fortunate to have him join.”

A Philadelphia native who now resides in New Jersey, Lafferty is the proud father of twin sons. When he isn’t helping small businesses succeed, you’ll find Lafferty golfing or riding motorcycles, or on the water boating and fishing in Punta Gorda Isles, Florida.

Please join us in welcoming new CCO David Lafferty, who, along with our dedicated group of CAN Capital team members, is ready to support our mission of helping every small business succeed.

About CAN Capital

CAN Capital, Inc., established in 1998, is the pioneer in alternative small business finance, having provided access to over $7 billion in capital for over 81,000 small businesses in a wide range of locations and different business types. As a technology powered financial services provider, CAN Capital uses innovative and proprietary risk models combined with daily performance data to evaluate business performance and facilitate access to capital for entrepreneurs in a fast and efficient way.

CAN Capital, Inc. makes capital available to businesses through business loans made by WebBank, member FDIC, and through Merchant Cash Advances made by CAN Capital’s subsidiary CAN Capital Merchant Services, Inc. ©2019 CAN Capital. All rights reserved

Media Contact: Carey Kirk, 678-858-6911, ckirk@cancapital.com

BFS Capital Eliminates Upfront Fees to Simplify Financing for Small Business Owners

October 1, 2019 CORAL SPRINGS, FLA. (Oct. 1, 2019)—BFS Capital, a leader in small business financing, today announced it has eliminated all upfront fees on its financing solutions, including loans and business advances, as it simplifies pricing for small business owners.

CORAL SPRINGS, FLA. (Oct. 1, 2019)—BFS Capital, a leader in small business financing, today announced it has eliminated all upfront fees on its financing solutions, including loans and business advances, as it simplifies pricing for small business owners.

With pricing that is transparent, flexible and easy to understand, BFS Capital is leading the evolution of small business financing. BFS Capital customers can now apply for and receive up to $500,000 in financing with no origination fees, no processing fees and no upfront costs. Customers are able to pay back a loan with a fixed daily or weekly payment, or as a flexible payment calculated as a percentage of credit card sales.

“There will be no hidden costs or unexpected surprises. What customers borrow is what gets funded into their accounts,” said BFS Capital CEO Mark Ruddock. “We are committed to empowering small businesses by meeting their needs with straightforward, cost-effective and timely online financing, whether it be to smooth cash flow, invest in adding staff, purchase equipment or upgrade a space.”

BFS Capital is also preparing to roll out a new, state-of-the-art digital lending platform. Over the next few weeks, the BFSCapital.com website will showcase a refreshed brand and exciting advances in automation across the entire loan application and approval process.

BFS Capital is also preparing to roll out a new, state-of-the-art digital lending platform. Over the next few weeks, the BFSCapital.com website will showcase a refreshed brand and exciting advances in automation across the entire loan application and approval process.

Partners, including Independent Sales Organizations (ISOs) that match small businesses to BFS Capital’s financing solutions, will also benefit from the company’s new no fee product proposition, evolving digital capabilities and dedication to transparency. ISOs and partners will soon have real-time visibility into the status of their leads across the entire customer relationship lifecycle, from the initial application through the life of the loan and beyond.

“As we embark on our mission of reimagining small business financial services, we are reinforcing support for our partners with API integration and faster, fully underwritten personalized offers, all complemented by market-leading pricing and commissions,” Ruddock added.

BFS Capital has over a decade long history of helping small business owners thrive and has provided more than $2 billion in financing. To qualify, businesses must be in operations for at least two years and generate at least $12,000 in monthly revenue. More than 23,000 businesses have been funded by BFS Capital across 400 industries.

To learn more, please visit BFSCapital.com.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS Capital’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund businesses in the United States, Canada, and through its United Kingdom subsidiary, Boost Capital. Since 2002, BFS Capital has provided over $2 billion in total financing to over 23,000 small businesses across more than 400 industries. Headquartered in South Florida with offices in New York, California and the United Kingdom, BFS Capital is an accredited BBB company with an A+ rating.

Media Contact

Archie Group for BFS Capital

Gregory Papajohn

gregory@archiegroup.com

917.287.3626

Nationwide Management Services Adds New Features To Its Virtual Site Inspections

September 20, 2019 MARICOPA, Arizona, September 20, 2019— Nationwide Management Services Inc. (NMSI) announced two new features have been added to its Virtual Site Inspection Software that will change the merchant cash advance and small business lending industries. NMSI’s new features are Pinch to Zoom/Remote Synchronized Zoom and Text Extract using OCR (Optical Character Recognition).

MARICOPA, Arizona, September 20, 2019— Nationwide Management Services Inc. (NMSI) announced two new features have been added to its Virtual Site Inspection Software that will change the merchant cash advance and small business lending industries. NMSI’s new features are Pinch to Zoom/Remote Synchronized Zoom and Text Extract using OCR (Optical Character Recognition).

With Pinch to Zoom you can touch the screen with two fingers and expand/collapse the distance between your fingers and the image zooms in and out. Also, you can move the image right, left, up, or down to focus exactly where you want to focus. Remote Synchronized Zoom allows participants to be simultaneously zoomed based on the mobile device, the user can choose zoom 2x or 3x.

Text Extract using OCR allows the use of optical character recognition to capture alphanumeric sequences to help eliminate typos. For example, a user can capture the MAC address or serial number of a device by copying it to their device/systems clipboard and then paste it wherever needed.

Millions of dollars are lost every year due to merchant fraud. NMSI is at the forefront of this technology and provide its clients with Virtual Site Inspection services that are easy, fast, and secure. In fact, this service can save time and allow Merchant Cash Advance Providers and their underwriters to fund deals quickly.

Important features that set the virtual site inspections apart from other competing services are online chat, SMS messaging, sharing of images, videos and documents, the ability to add single and group participants, screen share to multiple devices, private notes, capture still frame, collaborate markup of images, high-resolution photos, GPS tag location every 10 seconds, recording of the video session, and OCR to capture Serial numbers, Model numbers, and VIN numbers.

“Our proactive approach exemplifies our commitment in providing the small business lending industry the best in class virtual software in the marketplace,” said John Marsh, Chief Executive Officer for NMSI. “Our Virtual Site Inspections provide our clients with the risk management they desire. NMSI continues to lead the way in providing outstanding services to our clients.”

For more information about our Free Virtual Site Inspections, you may visit: https://debanked.com/nationwidemsi/

About Nationwide Management Services Inc.

Nationwide Management Services Inc. is a Veteran owned business established in 2005. NMSI is based in Arizona and specializes in Virtual Site Inspection and Face to Face contact (Door knocks).

SOURCE Nationwide Management Services Inc.

Media Contact:

John Marsh

President

Nationwide Management Services, Inc.

520.840.4583

info@nationwidemsi.com

www.nationwidemsi.com

TBF Financial Buys $60 Million in Commercial Debt from Major Online Lender

September 10, 2019 DEERFIELD, IL, Sept. 10, 2019 ─ TBF Financial purchased nearly $60 million in non-performing loans from a major online small business lender in recent transactions, CEO Brett Boehm announced today.

DEERFIELD, IL, Sept. 10, 2019 ─ TBF Financial purchased nearly $60 million in non-performing loans from a major online small business lender in recent transactions, CEO Brett Boehm announced today.

TBF bought the pools of post-charge-off loans as the highest bidder in transactions arranged through multiple brokers. In most cases, the company purchases directly from alternative lenders, equipment leasing companies and banks.

“We are seeing growing interest from online lenders who want to sell off commercial debt this year. It’s a smart strategy in any economic cycle because it provides lenders and lessors with immediate cash and a way to accelerate recoveries while protecting their customer relationships. Concerns about an economic slowdown are another reason for growing interest in commercial debt sales, as companies prepare to handle a rise in delinquencies and defaults,” Boehm said.

In the most recent deal, the $60 million in transactions included non-performing loans that had not previously been handled by collection agencies as well as post-agency accounts.

TBF Financial is the leading purchaser of non-performing equipment leases, commercial bank loans and online small business loans in the U.S. The company buys commercial accounts up to 4 years old from the date of last payment. This includes equipment leases, loans and lines of credit that have personal guarantees, no personal guarantees, are secured, unsecured, pre-agency, post-agency, pre-litigation and reduced to judgment.

Just as fintechs launched a new industry, TBF created its own industry. When the company started in 1998, there were no businesses buying lease charge-offs on a consistent basis. The principals of TBF believed that they could buy charged-off equipment leases at an attractive price that would also provide TBF with a margin of profit. The equipment finance industry embraced the new services. Since then, TBF has broadened the commercial paper it buys to include commercial bank loans and lines of credit.

The company remains at the forefront of commercial debt buying for the finance industry. For more information, visit tbfgroup.com or contact Boehm at bboehm@tbfgroup.com, 847-267-0660 or via LinkedIn.

Media Contact:

Carla Young Harrington

Susan Carol Creative for TBF Financial

540.479.7835

carla@scapr.com

Lending Valley Originates Over 100 Micro Deals in Debut

September 6, 2019 Brooklyn, NY – Lending Valley has originated 100 fundings to small businesses since the company’s debut in early June. The company was founded by small business finance veteran Chad Otar, the former CEO and co-founder of Excel Capital Management. Lending Valley focuses on micro funding deals of $1,500 to $10,000 with a variety of available payment structures. Otar is a Forbes Finance Council Member.

Brooklyn, NY – Lending Valley has originated 100 fundings to small businesses since the company’s debut in early June. The company was founded by small business finance veteran Chad Otar, the former CEO and co-founder of Excel Capital Management. Lending Valley focuses on micro funding deals of $1,500 to $10,000 with a variety of available payment structures. Otar is a Forbes Finance Council Member.

“We saw that the micro advances market needed another player and our goal is to help merchants’ businesses, not hurt them, and make it as easy as possible for them to obtain the capital and to be able to get them to the next step in their business venture,” Otar said. “Lending Valley is backed by years of industry knowledge and a diverse team that can provide the best support possible.”

About Lending Valley

Lending Valley was founded in New York City by Chad Otar. Otar is a member of the Forbes Finance Council. To learn more about Lending Valley, visit https://www.lendingvalley.com or call 866-888-3051.

Clearbanc Raises $300M in a Series B

July 31, 2019

Toronto-based Clearbanc, a company founded on the idea of providing business owners with capital to purchase facebook and instagram ads in exchange for a percentage of their future sales, has raised $300M in a Series B. $50M of it is an equity investment led by Highland Capital. The other $250M will go into a fund that Clearbanc uses to fund small businesses, according to Fortune.

Clearbanc’s payment methodology is reminiscent of merchant cash advances and their factor rates range between 6% and 12.5%. Funding amounts range from $10,000 to $10M and the company is reportedly on track to fund $1 billion to small businesses.

Clearbanc President and co-founder Michele Romanow is a serial entrepreneur that is also a celebrity investor on the TV show series Dragon’s Den. She attributes the idea for Clearbanc to her experience on the show in which entrepreneurs were inappropriately seeking venture capital when it was really a specific type of working capital they needed, funds to advertise on facebook or instagram, for example.

The company was founded in 2015 in Toronto.