merchant financing

Is it Just us or are the Deals Getting BIGGER?

October 15, 2012 Two years ago, it was easy to say that the average Merchant Cash Advance (MCA) deal was about $20,000 to $25,000. The claim used to be, funding up to $250,000! And yet very few companies would actually go that high when it came down to it. But now?

Two years ago, it was easy to say that the average Merchant Cash Advance (MCA) deal was about $20,000 to $25,000. The claim used to be, funding up to $250,000! And yet very few companies would actually go that high when it came down to it. But now?

A million here, a million there… It’s all just business as usual. Nothing to see here everybody. Go on Tozzi, write another article about how MCA is for minuscule retailers that can’t get approved for a low limit credit card. Whether you call it MCA, Merchant Financing, or Merchant Lending, there’s no doubt that capital has become more accessible to businesses across the country. And the amounts being disbursed are getting BIGGER.

On October 12, 2012, Rapid Capital Funding (RCF), a mid-sized funder in Miami, FL provided $1,250,000 to a national convenience store chain. RCF published an official company announcement about it, but we actually got wind of the deal a week before it closed. deBanked staff is friendly with the folks at RCF, particularly with their lead underwriter, Andrew Hernandez. Hernandez is an industry veteran, with five years of MCA underwriting experience under his belt. So while RCF hasn’t had the reputation for taking on big paper in the past, we can’t say that we’re shocked that they’re marching down that path.

Other big deals this year in the MCA space:

United Capital Source – $1,250,000

YellowStone Capital – $751,000

Do you think we’ll be seeing more of this? Send us your comments.

– Merchant Processing Resource

https://debanked.com

Legal Questions about Merchant Financing?

October 9, 2012 “Many merchant advance agreements state that the sales agent can only send merchant advance contracts to the one merchant advance company. It is important to identify such exclusivity terms and make sure they are deleted from the agreement. Just to make sure, you would also want to add a provision that states unequivocally that the relationship is non-exclusive. Otherwise, if you send merchant advance contracts to a competitor, the merchant advance company that thinks you are exclusive could use that act as a reason to termination your compensation under the agreement.”

“Many merchant advance agreements state that the sales agent can only send merchant advance contracts to the one merchant advance company. It is important to identify such exclusivity terms and make sure they are deleted from the agreement. Just to make sure, you would also want to add a provision that states unequivocally that the relationship is non-exclusive. Otherwise, if you send merchant advance contracts to a competitor, the merchant advance company that thinks you are exclusive could use that act as a reason to termination your compensation under the agreement.”

– Paul A. Rianda

Whether you’re an agent, ISO, or funder, you will at some point need sound legal advice. There is very little information on the Internet and hiring an attorney is expensive (though we highly recommend it!). If you feel like you just need a little guidance, we recommend you check out the publications by Paul A. Rianda, an attorney that has worked extensively in the bankcard and merchant financing industry. Below are a few articles that everybody should read:

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource

Merchant Cash Advance Industry is Waiting for its Big Moment

August 25, 2011Originally Posted 7/28/2011

According to an article in ISO&AGENT Magazine, the Merchant Cash Advance (MCA) industry has had significant success but “the companies that fund them acknowledge the cash-advance market is still waiting for its big moment.” This echoes our earlier opinion that a lack of collective marketing is keeping this financial tool from reaching its true potential.

How is it that in an ultra tight credit market that small businesses have not heard of MCA? With lax credit score standards, fast turnaround, minimal documentation, and a flexible method of repayment, it’s absurd that the industry has not reached so many that are looking to borrow. ISO & AGENT points to a negative image crisis and fingers the costs involved as a possible culprit.

The costs are a non-crisis. MCAs would be less expensive if they required collateral, perfect credit scores, fixed terms, ten years in business, and a 3 month underwriting process. If a small business meets those requirements and does not have a time sensitive opportunity they are looking to capitalize on, they should be going to their local bank. But most small business owners either do not meet that criteria or need the funds for a project they have going on today. Hence the product has to be more expensive for it to make sense for the firms providing the funds.

ISO&AGENT claims the industry has been compared to payday loans, an untrue characterization. In fact, that comparison has so rarely been made, that we can pinpoint the exact place they got that from. Inc.com published a very unflattering article on April 1, 2008 titled ‘Thanks, But No Thanks‘, in which they explain MCAs as “the business equivalent of a payday loan.” That was three and half a years ago! The article was not only biased and unfair, but was also written at a time when everything related to Wall Street, banks, or lending was being demonized as the nation sat on the verge of the Great Recession and economic collapse.

Still one can’t help but notice that buried deep within their criticism, is the answer to why MCAs are a tad bit more expensive:

The fact that collateral isn’t necessary is another important part of the MCA providers’ pitch. Entrepreneurs sometimes risk losing their homes if they can’t repay a bank loan, but they have no legal obligation to repay merchant cash advances if their companies fail, as long as they strictly follow the terms of the contract. They can’t encourage customers to pay in cash, for example, and they cannot switch credit card processors (typically, the MCA provider gets paid directly by the processor, rather than by the merchant). “If Diane’s Bistro goes out of business because Lauren’s Bar & Grill opens up across the street, we have absolutely no recourse to Diane, none whatsoever — as long as she follows the clearly defined covenants in our contracts,” says Glenn Goldman, AdvanceMe’s CEO.

And if you had any more reason to suspect MCAs are not as bad they tried to make it out to be, Inc.com published that article on April Fools Day. Case closed.

But there is indeed an image crisis and it’s that many businesses haven’t been exposed to the concept of MCA and thus cannot consider the pros and cons at all.

For instance: Most people can make the case for or against consumer payday loans. They’ve already got loads of information from the media, newspapers, banks, and lawmakers on which to base their argument. It’s become a well known household accepted form of financing. Whether or not payday loans can help the consumer is a separate debate.

That’s the difference. MCA is rarely spoken about by newspapers, banks, or lawmakers. Its presence in the media is limited and as a result we’re referring to stories published over three years ago. We have many friends employed as small business loan officers across the country and the only reason they’re aware of how MCAs work is because we told them. It’s embarrassing. And for an industry that funded over $500 Million last year alone, it really makes no sense.  We blamed antiquated marketing techniques: cold calling, junk mail, useless internet marketing, and spamming. The industry has gotten lazy and has a propensity to market their financing to small businesses that have already secured a MCA. This comes with bold promises of lower rates and other gimmicks. This inner competitiveness leads to both smaller margins and lower conversion rates. It does nothing to grow the industry as a whole.

We blamed antiquated marketing techniques: cold calling, junk mail, useless internet marketing, and spamming. The industry has gotten lazy and has a propensity to market their financing to small businesses that have already secured a MCA. This comes with bold promises of lower rates and other gimmicks. This inner competitiveness leads to both smaller margins and lower conversion rates. It does nothing to grow the industry as a whole.

That’s complemented by carpet bombing the public with an approach their customers learned to ignore a long time ago. Cold calls and junk mail. Really? Yes, really. There will always be a sliver of effectiveness from these methods and the firms that employ them will defend their success to the death. These methods may score some deals and perhaps even work well enough to grow a MCA firm, but it will not lead to the industry’s ‘big moment.’ Same goes for internet spam, poorly constructed articles that serve no purpose other than to boost some company’s SEO, and useless blogs kept by both respectable firms and no-name websites set up to harvest leads. Sure that’s the way of things on the internet these days but there isn’t anything beyond that. There are no mainstream media articles about MCA, forums for business owners where it is actively discussed, nor any public endorsements by anyone of high political or business stature.

Sounds like we have an image crisis on our hands. The Merchant Cash Advance Resource (the site you’re on right now) has been in existence for 1 year. In that time, we’ve made significant additions to the information that can be accessed here. We constantly receive emails from business owners and MCA brokers alike with the hope that we can provide them with an unbiased answer. And guess what? We do just that. By having no commercial affiliation, we give the best advice we can. The e-mail volume has gotten so heavy that our volunteer editors have trouble answering them all. But we try anyway.

And along the way we’ve managed to get some formal offers to convert this resource into a commercial site to generate sales leads. A six figure buyout offer here and there coupled with some lengthy, legalese filled non-disclosure agreements. We say ‘no’ every time. The Merchant Cash Advance Resource is designed to provide information, opinions, critiques, data, guides, and an independent ‘thumbs up’ to an industry that’s destined to do great things for small business.

Why do we spend the time, money, and effort to provide this service? We’re looking at the big picture of MCA. Big picture… Big moment…

And we’re on our way.

deBanked

https://debanked.com

The Fork in the Merchant Cash Advance Road

August 23, 2011Originally Posted on April 25, 2011 at 10:48 PM

The Merchant Cash Advance (MCA) industry is growing, albeit slower than some may have you believe. But it’s moving in two opposing directions, a condition that’s making it tougher to describe the financial product itself in general terms. MCAs are becoming more expensive and a lot cheaper at the same time. HUH? You read that right.

Originally aimed at business owners with poor credit, the risk of default or delinquency was overcome by withholding a percentage of sales revenue directly. As the credit crisis and Great Recession took hold, it attracted businesses of all credit backgrounds and today it’s widely accepted as a lending alternative, rather than a solution to poor credit.

As MCAs pushed forward to compete for customers normally accustomed to bank credit lines, the cost was stiffly resisted. These businesses had a tough time envisioning their financing terms to be anything outside of some percentage over the Prime Rate. Since a MCA is supposed to be structured as a sale, there is no APR equivalent, no timeframe, no amortization, nor any real familiarities of a loan. As the past couple years have passed, the product is more publicly understood, but for it to actually catch on, the costs had to come down. Many funding providers now refer to such high credit, low cost accounts as premium, platinum, preferred, gold, etc.

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

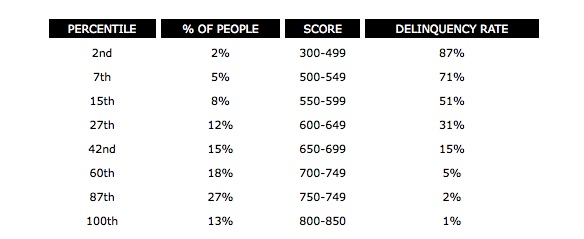

No matter which company ran the figures or how secret these portfolio statistics were, every funding provider came to the same realization. The lower the credit score of the business owner, the greater the chance of a problem. Why this came as any surprise, is a surprise in that of itself. The Fair Isaac Corporation (FICO) will have you know that any individual with a score below 499 has an 87 percent chance of being delinquent on a credit payment within the next 2 years. Delinquent, is defined as a payment of 90 days or more past due.

But wait… if a MCA is not a loan, nor does it depend on the business owner to make payments, then how can there be a risk of delinquency? Intentional manipulation of the revenue flow back to the funding provider can be relatively easy to do. A business owner could use spare POS equipment to accept card payments for which the funding provider is not aware of and therefore prevent the collection of funds. That’s a method known as splitting, and serious consequences can result when discovered. (Read more on what happens in the case of default or deliquency on a MCA in a previous article)

But outside the scope of malice, there’s the traditional reason, the inability to make payments. If the suppliers and wholesales aren’t being paid, then the business isn’t going to have inventory on hand to sell. If the rent isn’t being paid, then there’s not going to be any location to generate these sales. Essentially, the funding provider has a mutual interest in the business being able to satisfy ALL of their obligations, not just the MCA itself.

If there is an 87% chance that suppliers, landlords, or other essential creditors will not be paid on time in the next 2 years, then there’s an excellent probability that the business will be unable to operate at the same level. With no collateral as protection, the MCA industry has adapted to the challenge by raising the cost. Business owners with poor credit can expect funds to be expensive and the terms to be more restrictive. Lower funding amounts, higher withholding percentages, and the sacrifice of any negotiation is the price the MCA industry has set to make funding to the maximum risk group possible. These programs, which are now often referred to as starter advances, don’t work for everyone so the pros and cons should be weighed prior to executing a contract.

Both the premium advances and starter advances have experienced extraordinary growth to the point where they have become niches of their own. There are now starter advance companies and premium advance companies. Funding providers like Strategic Funding Source have taken the product a step further and reportedly did a MCA for an exhibit at the Tropicana Hotel in Las Vegas for $4 Million. Contrast that with deals that are struck for as little as $750. And we can’t fail to mention that some have taken it back to the basics, a loan. ForwardLine in Woodland Hills, CA lends money to businesses which are then repaid in accordance with a predetermined, fixed pace through the card sales. They have reintroduced concepts like APR back to the finance world.

If we continue at the current pace, MCAs will become less expensive, more costly, a lot bigger, and markedly smaller. We’ve come to the fork in the road for what the Merchant Cash Advance industry seeks to brand itself as. Loan alternative? First choice? Backup plan? Is it for smaller businesses or larger ones? Should it go the way of lending or continue to remain a structured purchase of future card sales? Is industry cohesion really necessary or will increased decentralization lead to greater acceptance of this financial product a whole? Will there come a time when America’s big banks swallow the industry up, buy out the existing portfolios, and add this product to their financing arsenals?

These are tough questions. Merchant Cash Advance is evolving, growing, and no longer moving in one direction. While we contemplate our next step, one thing is for certain, there’s no turning back.

– deBanked

www.merchantprocessingresource.com

Deja vu? Merchant Cash Advance in Wall Street Journal

August 10, 2011 Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

Have you ever had a deja vu moment where you feel like something has happened already even though it hasn’t? And then all of the sudden it happens? Yeah, we just got a little of that. Or maybe we’re just psychic.

It was just a couple months ago that we published a scathing editorial on the failure of the Merchant Cash Advance (MCA) industry to reach mainstream acceptance. (See: The Colossal Marketing Failure of the Merchant Cash Advance Product – June 28th, 2011). Most of our readers acknowledged the shortcomings but were at a loss for suggestions to overcome them. ISO&Agent Magazine quickly added their two cents by claiming that MCA was waiting for its big moment (See: Cash Advances: Negotiating a Maturing Market – July 26th, 2011) but completely missed the mark when they identified cost as the obstacle holding it back. It’s not cost, it’s communication.

How often is MCA cited in mainstream news publications? Wall Street Journal? New York Times?

-direct quote from our piece on June 28th

Today we can say that Merchant Cash Advance got its mention in the Wall Street Journal. :::Applause::: Though it’s only in their blog section, most people today get their news online anyway. The article features AdvanceMe, the largest and oldest player of the bunch. So how does the glorification of one company carry over to the industry as a whole? There were a bunch of good messages in there that describe the product itself: The article title implies it’s becoming more popular: “Cash-Advance Demand Rising” A description of how it works: “Merchant cash advances, which first appeared about a decade ago, provide capital in exchange for a share of future debit or credit-card sales. As such, they tend to be used by retailers, restaurants and other small businesses where a large number of customers pay with cards.”The common uses for it: “Business owners use the cash to buy new equipment, restock inventory or pay off debt” Yes, Yes, and Yes. Good for AdvanceMe and good for the MCA industry but this is only the beginning.

Every business owner should be aware of MCA, not just the ones that read the Journal today. It is Un-American (Yeah, that’s right) to withhold information from business owners that may enable them to capitalize on opportunities. With no bank loans available, most projects in this country are on hold. It’s simply not fair. We badly want to take the credit for today’s Journal mention, especially since we delivered our two previous articles on this topic to their editors in July. But the real hero here is AdvanceMe. Their press release the day before clearly caught the attention of the mainstream media. Great job guys. And we’d be remiss if we didn’t point out they forecasted an increase in funding by $1 billion in the next 2 years. That’s about equal to the industry’s entire volume combined. Is Merchant Cash Advance about to hit its growth spurt? AdvanceMe seems to think so. If they’re about to have their ‘moment‘, they’ll likely pull everyone else along with them.

– deBanked

https://debanked.com

Merchant Cash Advance and Startup Businesses

October 20, 2010 Kudos to the entrepreneurs taking a chance in the worst economic period of modern times. Starting a business is already a truly challenging task in itself but before we shower you with praise for being the ultimate warrior of capitalism, let’s put everything into perspective.

Kudos to the entrepreneurs taking a chance in the worst economic period of modern times. Starting a business is already a truly challenging task in itself but before we shower you with praise for being the ultimate warrior of capitalism, let’s put everything into perspective.

Risk takers are a minority in today’s startup community. A persistently high rate of unemployment is breeding a culture of survivalists; Individuals that have been pushed to the limit via pay cuts, layoffs, and robo-signing foreclosing bankers. It’s resumé rejection, employer double talk, and anger at how Wall Street bankers continue to live. The new entrepreneurs are a resounding chorus of “If I can’t get a job, I’ll make my own job!” These people are going for it on 4th Down and Long and running it up the middle for a touchdown. It’s as if Charles Darwin spiked their Corn Flakes.

Startup survivalists are just as inspiring as their risk taking counterparts. Both groups have the drive and that’s essential. But you can’t forego some basic tools. Financing is a must. No capital, no business. Unless you are fortunate to start with deep pockets, you need access to cash.

New businesses are not likely to be offered credit terms by vendors, nor can you push back overhead expenses such as rent, until you’re generating revenue. If unforeseen demand overwhelms your capacity, a cash shortage can do irreparable damage to your success.

Rather than spew rhetoric about the importance of funds, and shortchange you with a bullet point list of vague sources whom in reality are so illiquid, they’re not actually viable, we’ll offer our real 2 cents.

Banks. For a startup? Not happening. Angel Investors and Venture Capitalists? Slim to no chance. Unless these private investors live in your community, they’re not going to invest in your business. More than 90% of startups fail. For an investor to take that much risk, they’re going to do some hands on management or want to follow you around and critique how you’re spending their money. That’s not necessarily a bad thing. It just means that one can’t reasonably expect a return on their investment without intimate knowledge of the demographics and community the business is situated in.

Looking for private investors over the internet? Don’t. Your pro forma financial statements, data research, and business plan won’t help. Do you know how many businesses fail to open even after they incorporate, sign a lease, purchase inventory, advertise, and make preliminary hires? An astounding number are eclipsed by failed health inspections, license/permit rejections, and building code violations. This reasserts that unless an investor is personally intimate with your progress, the odds are stacked against them.

Lastly, you need not pay to get approved for capital. We’ve spoken with many start ups over the last year and are flabbergasted by the amount of new businesses that are convinced they have to pay a $3,000 upfront fee to get approved for a loan. The ones that actually pay are quick to learn what town the lender is based in; It’s called Scam City.

Real Option? Merchant Cash Advance. A Merchant Cash Advance offers a business with a lump sum of capital upfront. In return, a piece of every sale the business makes will go towards paying it back plus a predetermined fee. There is no due date or set term for repayment. That means if sales are slow to get off the ground, then funds will be repaid slower and with no penalty.

A Merchant Cash Advance provider entrusts you with their capital because of the unique security the repayment method offers. The business itself must accept credit cards as a form of payment. The credit card processing company will automatically deduct the agreed percentage piece of each sale transacted and forward it to the Merchant Cash Advance provider on your behalf for repayment.

A startup can qualify with as little as 1 week in business. As long as you open, you can get funding. Credit can play a limited factor and the cost can be hefty, but the access to capital is unmatched. From the date you apply, funds can be received in as little as 5 days.

Purchase inventory, pay the rent, advertise, hire, or seize an opportunity. Whichever shortcoming you face, it can be overcome with a Merchant Cash Advance. Industry experts project that funding is on pace to reach over $600 Million for 2010 alone. With advances ranging from as small as $1,000 to as high as $500,000, there is proof that numerous deals are being made every day.

We’ve seen the same books, guides, and expert advice columns that you’ve seen and all of them seem to be a reprint of useless suggestions like the SBA and searching for angel investors online. These people earn a living writing. Whether or not the money expert column in your newspaper actually helps you, makes no difference to them. We have many years experience in the Merchant Cash Advance industry and we make careers out of funding you, not telling you about funding.

We try not to promote any one company over another. There is no harm in enlisting the service of a middleman or reseller for one of the direct funding sources. It may actually benefit you. If you are open for business, you can obtain a Merchant Cash Advance. If you have been in business for a long time, a Merchant Cash Advance is still a fantastic option.

It’s 4th Down and Long. You’re ambitious, focused, and ready. You are the ultimate warrior of capitalism. A Merchant Cash Advance will supply the cash. Grow, take risks, survive, and don’t be surprised if your Corn Flakes taste funny.

Merchant Cash Advance Blacklist

August 5, 2010If you default on a Merchant Cash Advance naturally or by breach of contract, there is virtually no chance you will be able to obtain a Merchant Cash Advance in the future. 2008 was a particularly brutal year for Merchant Cash Advance firms. Not only had the recession weakened the most aggressive players but merchant fraud was abundant. 90% of the time this business is conducted by phone. Being vastly easier to obtain than a loan, many merchants rigged the process to get funding from multiple firms at the same time. Some would “go out of business” only to obtain more funds under a different name.

Merchant Cash Advance providers have stuck by their mantra of providing a simple process to their clients and have created solutions to prevent fraud. Industry groups such as the North American Merchant Advance Association provide a live database exchange of clients in default. A merchant’s most sensitive information is not revealed but public information such as legal name, dba, owner name, business address, and phone numbers (to name a few) are all stored in the database. Live funding activity is also shared in some capacity. For instance, if you apply to funding firm A and funding firm B at the same time but are funded by firm A today, then Firm B will automatically be alerted not to fund you.

These deterrents and live databases are not broadcast to the public and thus some businesses try to obtain additional advances after having defaulted on one already. If you are a merchant and you are trying to hide the fact that you currently have an advance or defaulted on one previously, you will not be successful in obtaining funds from another firm.