Business Lending

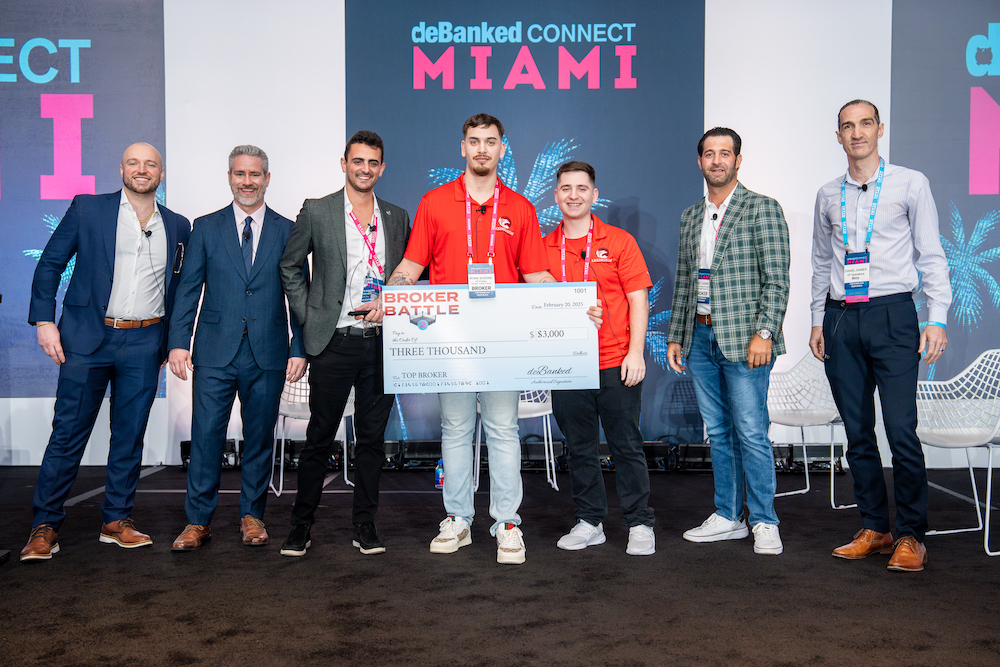

Ryan Showe on Winning This Year’s Broker Battle

March 3, 2025 “What being a broker means to me is servicing your clients in the best way possible, really putting their needs before anyone else’s,” says Ryan Showe, VP of Sales at Long Island-based Lexington Capital Holdings. “Ultimately, at the end of the day, we don’t have a job if our clients aren’t happy, so just constantly doing the right thing, putting your best foot forward, and making sure that you’re doing everything ethically and honest.”

“What being a broker means to me is servicing your clients in the best way possible, really putting their needs before anyone else’s,” says Ryan Showe, VP of Sales at Long Island-based Lexington Capital Holdings. “Ultimately, at the end of the day, we don’t have a job if our clients aren’t happy, so just constantly doing the right thing, putting your best foot forward, and making sure that you’re doing everything ethically and honest.”

Showe was the winner of the 2025 Broker Battle at deBanked CONNECT Miami for the revenue-based financing category, earning him the recognition of Top Broker and the recipient of some prizes along with it. Showe has been in the business for just a little over three years, starting at Lexington during its beginnings. Back then, learning the ropes while doing the work meant putting in 70-80 hour weeks on a regular basis. That included not only seeking out advice from the experts but also watching videos and reading books to fully immerse himself in the mindset of what it would take to become successful.

That effort is paying off and today Showe specializes in the most delicate part of the process at Lexington, helping clients who have applied get to the finish line with a deal while managing lender-side negotiations and communications. On the latter side, that means being highly familiar with the guidelines of more than 60 financial service companies at any given time.

“Anybody can get someone to apply and just fill out a quick one-page application, send over a couple bank statements, but really selling the deal, there’s a specific art to it,” says Showe. “It’s really important to be an expert in your industry and know all the lender guidelines, know what the backend process looks like, because every lender is going to have a different process, whether there’s certain steps that some lenders want, whether it’s a manual-login or DecisionLogic. There’s so many ins and outs to every different lender. And just being able to know all that off the top of your head and just really sound like an expert.”

At Lexington, one of the recent educational team-building strategies was to host an internal Broker Battle in which 30 employees participated in a double-elimination competition. The company’s CEO, Frankie DiAntonio, devised the format and questions—not only role‑playing scenarios but also testing general industry knowledge with trivia. Showe says it’s good practice to be put on the spot in front of a crowd, because a key part of sales is thinking on your feet and executing when it counts. Doing it together with colleagues made for a fun experience in a company that prides itself on a family‑like atmosphere, while also mirroring the competitive nature of the industry where many brokers vie to serve the same customers. It’s game time all the time.

“I even tell my clients, ‘competition is always going to breed the best results,'” Showe says. “If you want the best of the best, you have to make people compete. And it goes down to even selling a deal, right? So if I have a deal and another company has a deal, compare my numbers against their numbers. I’m going to do anything I can to win that business.”

By happenstance, Lexington’s Corey Digiantomasso was one of the six finalists selected to compete in deBanked’s inaugural Broker Battle in 2024, where he put up a very impressive performance. This year was Showe’s turn where contestants weren’t given much background on the format other than that it would be roleplay-based. Showe kind of liked the mysteriousness of it.

“I’m best at showing up and just getting the job done,” Showe says. “So just doing what I do every single day made it easier for me at least.”

On his victory, Showe described the feeling as awesome while also recognizing that his opponent in the Battle, Joe Sasson, was a very worthy competitor. A large crowed showed up to support both of them during the championship.

“It was great to just see all the hard work that I’ve been putting in over the last three years pay off and be crowned #1 in the industry. It goes a long way for not only myself, but for the company as well.”

NerdWallet: Still Pressure in SMB Loan Originations

March 2, 2025NerdWallet’s CEO Tim Chen explained during the company’s Q4 earnings call that headwinds across both consumer and SMB lending have not let up.

“We continue to see pressure in SMB loan originations with rates remaining elevated and underwriting remaining tight, while also seeing increased pressure in our renewals portfolio as the 10-year rates reversed course and began to climb,” he said.

NerdWallet originates borrowers through the internet, a significant portion of which comes from organic search traffic. That organic traffic dipped about a year ago after changes to Google’s algorithm but has been recovering over the last two quarters for SMB loans. During the earning’s call, one analyst, Ralph Schackart of William Blair & Company LLC, had a question about the continued reliance on that channel given the rise of competing AI chat assistants.

“I guess as you are sitting here today and sort of operating this business, obviously for a while here, how different do you think these changes are to the business with AI overviews?” Schackart asked. “And some digital buyers are saying that the ads that are generated from Gen-AI are actually performing better than some of the organic results. Just kind of curious, what’s your confidence that this is something you’ll be able to navigate longer term versus your previous history? ”

This was Chen’s response:

“I’ll split it up between kind of the shorter-term stuff we’re seeing and longer-term thoughts. I mean in the near term, there’s two drivers here. Which is, one is more ads and modules on top of the search results. And the other factor is rank. Where in the very recent past, financial institutions and some government websites are winning in some areas where they traditionally haven’t, which as I’ve alluded to in past calls, is a bit of a head scratcher when considering consumer intent.

We do think this period of frenetic testing will eventually stabilize, and when that happens, it should play to our favor. Longer term, I do think that it’s important to look at broader industry trends. First, AI search engines or chatbots, are they taking share from traditional search engines?

I mean from what we can tell, not really. If you look top-down, more people are using search engines than they did last year, but you also see triple-digit growth in AI usage. Which says to me that people are basically just asking more questions that they weren’t asking before. And second, the things like AI overviews, how is that affecting the ecosystem?

So I know we’re not focusing on MUUs operationally, but it’s helpful to understand that if simple questions have simple answers, and if a search engine can serve that up in a faster way that consumers prefer, then that’s good for the ecosystem.

And for us, we’re seeing these features do a really good job of answering simple educational questions, and that’s affecting traffic to some of our noncommercial pages. That has not been the case yet for our monetizing pages, which are fundamentally just a little more complicated.

Like if you need to shop for a mortgage for instance, you really need to go through a marketplace experience. So yes, on balance, we think that this period of frenetic testing will stabilize. We’ve seen a few things like this in the past, and we can grow from there.”

Square Loans Originated $5.7B in Business Loans in 2024

February 25, 2025Block subsidiary Square Loans had a huge Q4, originating $1.54 billion in business loans. That brought the year-end total to $5.7 billion, enough to continue their streak as the largest online business lender that deBanked tracks. Enova is #2.

Square Loans customers typically experience growth when taking the funds. Block CEO Jack Dorsey said this of the program in the previous quarter:

“In 2013, we began offering capital to sellers because we saw a meaningful gap in the market: small businesses were often denied access to credit, in the same way they were once denied access to accepting credit cards. We utilized our deep understanding of the seller and their business to build a technology that invited them to accept a loan with transparent rates, and pay back simply by making sales to their customers. We called it Square Capital (which is now known as Square Loans).

Since then, we’ve underwritten more than $22 billion in loans globally, with aggregate loss rates below 3%. And we’ve proven we can expand access: 58% of Square Loans are to women-owned businesses, and 36% are to minority-owned businesses, both of which are higher than the benchmark we track If our sellers grow, we grow – and we believe Square Loans has a direct impact on our sellers’ growth. Sellers who take out a Square Loan grew on average 6% faster than sellers who did not take out a loan.

Many financial products trap borrowers in cycles of revolving debt. We don’t allow customers to take on new loans if they have an overdue balance. And repayment is built into how our products work: Square sellers repay loans through a fixed percentage of their revenue, creating a manageable-real-time payment flow.

On credit risk management, we have a long history of maintaining stable loss rates and these products act as working capital, which means they are usually short in duration. What that means for us is that a dollar used on our balance sheet can turn multiple times, driving capital efficiency while providing us with high-quality data to continually refine our technology-driven underwriting.”

-Jack Dorsey

What to Look Out For in Back-up Servicing

February 17, 2025 “There is a misconception that back-up servicing is merely an Insurance Policy,” states Larry Chiavaro, Chairman of Paramount Servicing Group, in a recently released White Paper on the subject. “That is not the case in today’s rapidly changing markets. Fluctuating interest rates, the creation of many new asset classes, and emerging technology have created many new opportunities for all.”

“There is a misconception that back-up servicing is merely an Insurance Policy,” states Larry Chiavaro, Chairman of Paramount Servicing Group, in a recently released White Paper on the subject. “That is not the case in today’s rapidly changing markets. Fluctuating interest rates, the creation of many new asset classes, and emerging technology have created many new opportunities for all.”

The 12-page paper on back-up servicing dispels many myths while educating lenders about what to look out for when choosing a servicer. It is clear that the selection process should not be an afterthought and can be very consequential for one’s business. Chiavaro breaks it down well. You can download the paper here.

Shopify Capital Originates ~$3 Billion in Merchant Funding in 2024

February 11, 2025 Shopify Capital originated ~$3 billion worth of MCAs and business loans in 2024, up by 50% over the prior year. For the sake of comparison, online small business lender Enova originated $4 billion in 2024. Shopify is an e-commerce platform first, however, and is growing on all fronts

Shopify Capital originated ~$3 billion worth of MCAs and business loans in 2024, up by 50% over the prior year. For the sake of comparison, online small business lender Enova originated $4 billion in 2024. Shopify is an e-commerce platform first, however, and is growing on all fronts

“2024 was a stand-out year for Shopify,” said Shopify President Harley Finkelstein. “We seized every opportunity to fuel our growth and it showed in the results quarter after quarter. Heading into 2025, we are committed to making entrepreneurship more common and further establishing Shopify as the go-to commerce platform for businesses of all sizes. With our proven track record, the agility of our platform, and our relentless focus on merchant success, we like our odds in this evolving technology landscape, and are excited about the opportunities it brings for Shopify and our merchants.”

Enova: Record Q4 originations with little competition in sight

February 5, 2025 Enova originated $1.1B in small busines loans in Q4 2024. And it’s a wide open market, according to the company. “We’ve not seen kind of a sustained competitive push on either the consumer or small business side in a very, very long time,” said Enova CEO David Fisher during the quarterly earnings call. “And again, I think evidenced by our ability to take really significant volume in Q4 shows that to be the case.”

Enova originated $1.1B in small busines loans in Q4 2024. And it’s a wide open market, according to the company. “We’ve not seen kind of a sustained competitive push on either the consumer or small business side in a very, very long time,” said Enova CEO David Fisher during the quarterly earnings call. “And again, I think evidenced by our ability to take really significant volume in Q4 shows that to be the case.”

Fisher added that “you do see people kind of poking in and out” of the market “but they tend to be small and they tend to be fleeting.”

The economy is also playing into their success.

“On the small business side, I would say if anything, we feel better about the health of small businesses across the country,” Fisher said. “I think they’ve had one more year to build strength, kind of following the pandemic and following the high inflationary years of 2022, early 2023. And so we’re feeling also very good about the general health of small businesses.”

Fisher cited a joint report it prepared with Ocrolus this past November in which a survey found “that small businesses feel increasingly optimistic about future growth as over 90% of small business owners are expecting moderate to significant growth over the next six months.” It also showed “a meaningful shift in where small businesses are first seeking capital as nearly 75% of small business owners reported bypassing traditional banks in favor of alternative lenders like Enova.”

Charge-offs have been on a downward trend for Enova as well and the company feels good about how diversified its portfolio is.

PayPal: Our merchants grow after taking a business loan from us

February 5, 2025 PayPal is feeling optimistic about its business loan program now that it has been reset on a path toward growth. “As the business matures, PayPal Business Loan offers more traditional merchant financing to match the increasing complexity and multichannel nature of larger businesses,” said CEO Alex Chriss during the Q4 earnings call. “Our business financing solutions increase loyalty and engagement, driving the PayPal flywheel. Merchants typically increase their PayPal volume by 36% after adopting PayPal Working Capital and 16% after taking a PayPal Business Loan. Our merchant lending originations were $3 billion in ’24, demonstrating our leadership and that there’s plenty of room to grow to support our customers.”

PayPal is feeling optimistic about its business loan program now that it has been reset on a path toward growth. “As the business matures, PayPal Business Loan offers more traditional merchant financing to match the increasing complexity and multichannel nature of larger businesses,” said CEO Alex Chriss during the Q4 earnings call. “Our business financing solutions increase loyalty and engagement, driving the PayPal flywheel. Merchants typically increase their PayPal volume by 36% after adopting PayPal Working Capital and 16% after taking a PayPal Business Loan. Our merchant lending originations were $3 billion in ’24, demonstrating our leadership and that there’s plenty of room to grow to support our customers.”

PayPal offers this product in the US, Germany, France, the Netherlands, UK, and Australia.

“The PayPal Working Capital product allows businesses to access a loan or cash advance for a fixed fee, based on their annual payment volume processed by PayPal,” the company states. “The PayPal Business Loan product provides businesses with access to short-term financing for a fixed fee or interest based on an evaluation of the applying business as well as the business owner. In the U.S., these products are provided under a program agreement with an independent chartered financial institution.”

Between them, PayPal is one of the largest online business lenders in the US.

With Trump’s Freeze on New Regulations, What to Make of the New CFPB Rules?

January 23, 2025 On January 20, Trump’s ceremonial display of taking action and signing orders on his very first day might warrant a closer look for those in the small business finance industry. That’s because he signed a regulatory freeze order that could potentially affect rules promulgated by the CFPB on small business loan data collection that have yet to go into effect.

On January 20, Trump’s ceremonial display of taking action and signing orders on his very first day might warrant a closer look for those in the small business finance industry. That’s because he signed a regulatory freeze order that could potentially affect rules promulgated by the CFPB on small business loan data collection that have yet to go into effect.

Specifically Trump’s order not only puts a freeze on issuing new rules but also mandates rules be withdrawn if they’ve been sent to the Office of the Federal Register. And then lastly, and most relevant, it orders agency heads to “consider postponing” any rules that have been published or “any rules that have been issued in any manner but have not taken effect, for the purpose of reviewing any questions of fact, law, and policy that the rules may raise.” It asks for a 60-day review period overseen by an agency head appointed or designated by Trump to review and approve the rule.

“Should actions be identified that were undertaken before noon on January 20, 2025, that frustrate the purpose underlying this memorandum, I may modify or extend this memorandum, to require that department and agency heads consider taking steps to address those actions,” the order concludes.