Business Lending

Loan Brokers: Fight Back and Defend Your Brand

January 16, 2016 LIFE DOESN’T PLAY FAIR AND NEITHER DOES YOUR COMPETITORS

LIFE DOESN’T PLAY FAIR AND NEITHER DOES YOUR COMPETITORS

Let’s face it, a big part of our job is customer service. As a direct funder or lender, or as a large or small brokerage, a big part of our job is to service our existing customers, partners, vendors and suppliers with the utmost integrity, efficiency and ethics. But even the best of customer service intentions can become scarred when those who compete against you, choose to compete unfairly through vile fabrications, defamations and falsehoods.

MORE MONEY, MORE PROBLEMS

Not many people (including myself) are too fond of hip hop music as most of the time the lyrics are questionable, but in 1997, everybody agreed with The Notorious B.I.G. when he touched on the concept of making more money and having to subsequently deal with new problems.

The bigger and more exposed you get, the higher the probability that you’ll have a run-in with dissatisfied merchants, partners, vendors and suppliers. This is common knowledge, as many of the largest ISO/MSPs and MCA firms are all over the ripoff reports in one form or fashion, with current and prior customers blasting the companies over sometimes legit issues, and other times issues of a petty nature that could have been resolved in means of a lesser depiction. But continuing on, the bigger you get, the bigger your “haters” will get as well. The rise of the internet has multiplied the presence of haters and trolls to a population standing taller than ever before. These haters love to use online discussion boards, social media, blogs, and review sites to spread their lies, hatred and vile.

JUST BECAUSE YOU SMELL SMOKE, THAT DOESN’T MEAN THERE’S A FIRE BURNING

I’m not sure who the author of this quote is, but it says the following: People will question all the good things they hear about you, but believe the bad without a second thought. Haters know this quote to be true and are quick to spread their venom knowing that if it’s coming from multiple sources, then far too many people will take them at their word using the flawed logic of “where there’s smoke, there must be fire.”

Well, I say just because you smell smoke, that doesn’t mean there’s a fire burning. Instead, you could more than likely have a group of haters who have perfected the art of blowing smoke, which is to make unfounded or exaggerated claims. As a result, you need to protect your brand against haters. There are those of you who believe that if you just ignore them then they will go away. Well, I disagree with that notion and so does Motorhead’s Lemmy Kilmister. “I don’t understand people who believe that if you ignore something, it’ll go away,” he was once quoted as saying “That’s completely wrong because if it’s ignored, then it gathers strength. Europe ignored Hitler for twenty years, as a result he slaughtered a quarter of the world!”

LOOK AT DONALD J. TRUMP

If he wins the candidacy or not, Donald Trump will go down as perhaps the most fiery presidential candidate of all time. When Trump believes something, he says it, without filter and without care of political expediency. When Trump is “attacked” by the media or one of his fellow GOP opponents, he fires back. On the O’Reilly Factor after the final GOP debate of 2015, Trump clarified that if the media or one of his GOP opponents makes a valid criticism about him, he’s perfectly fine with that, but what he has a problem with is when they flat out lie about something he’s said, done or believes in.

While I’m an Independent and not sure who I will support for the 2016 Presidential election, I find myself in agreement with Trump on a number of things, including how Trumps responds to “haters.” My stance is that if you have a valid criticism about something I’ve said, done or believe in, then I’m all ears! But when you flat out lie about me, now you are going to tick me off.

GET MAD, GET MAD!

One of the reasons for Trump’s surge in the polls is the fact that a lot of people are angry at leaders in Washington and aren’t going to “take it” anymore. Trump’s fiery persona attracts people to the real estate tycoon, causing him to have a massive lead in the Republican race. Like Trump, you should get mad as well if you have worked to build your brand, resumé and marketplace standing, and then all of a sudden here comes some anonymous troll spitting out all types of defamations across the internet:

- Don’t work with XYZ Company, they are a scam!

- XYZ Company stole my money!

- XYZ Company’s President is a criminal!

- XYZ Company backdoors deals!

The definition of libel is to write something about an individual or a company that is defamatory, which is a statement that is false but written in a way to convince the public that it’s true. The internet has increased the presence of libel so much, that insurance companies market their personal umbrella policies as a form of insurance in case you are sued for libel. Some people don’t realize that typing something on the internet can get you in trouble if you are lying about the person or the company in question. Now, I’m not advising you to run out and sue everybody who lies about you online, as that would be very costly, however, I am advising you to get mad by fighting back and doing some of the following to protect your brand.

FLOOD THE MARKET WITH TESTIMONIALS

Begin to flood the market with positivity. When a prospective client searches for your company in Google and finds the negative reviews, they can also see the various videos, blogs and review sites where your customers, partners and vendors are praising you. You can always say: Look at the many customer testimonials that we have and look at the size of our customer portfolio, clearly more people are satisfied with us than dissatisfied.

THE BETTER BUSINESS BUREAU

The BBB will provide you an “A+” or “A” rating as long as you respond to any complaints filed in a timely manner. You can use your “A” rating status in marketing and in response to prospective clients inquiring about negative reviews. You can always say: We have an A+ rating with the BBB, we must be doing something right.

PUBLIC RELATIONS

A lot of direct funders and large brokerages have large sources of operating capital to play with, so why not hire a PR Team? Have a PR Team speak with the media often to generate as much positive press as possible to help balance out the negative press. In addition, have the company CEO and other high ranking officials do various forms of PR when available.

TAKE THE FIGHT TO THE TROLLS

Go to the discussion board, social media post, blog post, vlog post, or website, and directly respond to the person creating the negative press. Debate your points, prove them to be wrong, show them to be a liar, and encourage your employees, vendors and partners to join in on the fight. Silence can be taken in one of two ways, either people will think you are “too big” for this petty non-sense, or they will think that you are silent because you are guilty. I say take the fight to the trolls, debate your points and then move on after you’ve put the verifiable truth on the table.

THE FINAL WORD

Some people will already know something is a lie, but choose to believe it anyway because they want it to be true regardless. Sean Parker’s character from the Social Network said that, “even if you’ve managed to live your life like the Dalai Lama, they’ll still make things up because they don’t want you, they want your idea.” The honest truth is that most of your haters are just jealous of you because, you have something that they want but don’t have. So, don’t allow them to throw you off your game.

As a quote I read the other day from some unknown source said, “you should never hate people who are jealous of you, but instead respect their jealousy as they are the people who think that you’re better than them.” Having haters is a sign that you’re doing something right. Your prospective customers and partners with good judgment should be able to read between the lines to see the truth, and for those that can’t, well, maybe they are too gullible (and stupid) to be doing business with anyway.

OnDeck and Bank Partnership Concept Debated on CNBC

January 13, 2016On CNBC’s Squawk Box, OnDeck CEO Noah Breslow responded to questions about why the fintech goal post of putting banks out of business has seemingly been readjusted. Breslow said that their mission all along has been to extend the market for credit, namely by originating small dollar loans (under $1 million) that banks can’t or have been unwilling to do. He supported that by saying that this market has always historically been underserved and is not just a consequence of the last recession.

More importantly though is the debate over whether or not banks should build, buy or partner with alternative lenders. (Hello marketplace Lending Hunger Games!) OnDeck believes their 8-year head start is an attractive reason as to why banks should “partner” with them.

On regulation, Breslow classified OnDeck as a “non-bank commercial lender,” which may be true from a regulatory perspective, but it’s a big departure from the sexy technology marketplace platform characterization that they’ve historically campaigned under.

Lastly, the OnDeck – JPMorgan Chase deal apparently does carry exclusivity and it is possible for them to engage in other partnerships.

Full video on CNBC below:

Bernie Sanders is Probably Not the Marketplace Lending Candidate of Choice

January 6, 2016 Perhaps the fastest way for Americans to become deBanked is to elect Bernie Sanders as President. In a proposal he laid out on Tuesday, Sanders pledged to break up commercial banks, shadow banks and insurance companies that he believes are “Too-Big-to-Fail.” While not everyone would be especially sad to see something like that happen, there’s a whole bunch of other reasons Sanders might not be the marketplace lending candidate of choice.

Perhaps the fastest way for Americans to become deBanked is to elect Bernie Sanders as President. In a proposal he laid out on Tuesday, Sanders pledged to break up commercial banks, shadow banks and insurance companies that he believes are “Too-Big-to-Fail.” While not everyone would be especially sad to see something like that happen, there’s a whole bunch of other reasons Sanders might not be the marketplace lending candidate of choice.

Here’s a summary of what he said:

- The Business Model on Wall Street is Fraud.

- All consumer loans should have an interest rate cap of 15%.

- Lenders who charge more than 15% are awaited in the Seventh Circle of Hell.

- Quote: “Today, we don’t need the hellfire and the pitch forks, we don’t need the rivers of boiling blood, but we do need a national usury law.”

- Big banks need to stop acting like loan sharks and start acting like responsible lenders.

- Post offices should become government banks so that free market lenders will go out of business.

While Sanders admittedly said we don’t need the rivers of boiling blood, a large portion of lenders, marketplace lenders included, apparently have a special place in hell reserved for them. His over the top statements come on the heels of a gaffe, in which he revealed very publicly on twitter his ignorance over how loan underwriting actually works.

Will you be voting for Bernie Sanders this primary season?

Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

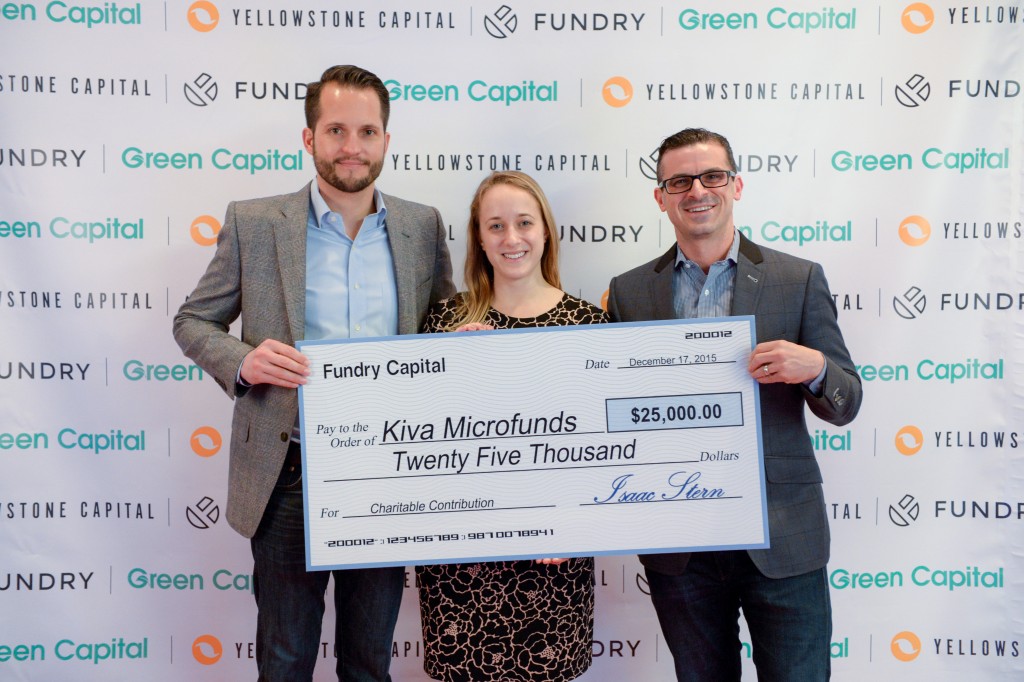

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

deBank the World: See the Times Square Ad Campaign LIVE

January 1, 2016If you didn’t make it to Times Square for the New Year’s Eve celebration, you’re probably a lot better off. But if you’re not going to be in that neighborhood any time soon either, you can still catch a LIVE glimpse of three very important company logos that are broadcasting on a video billboard above 43rd and Broadway. (hint: look at the top left)

The deBanked ad in particular, which only makes a handful of appearances every hour in the rotation, can be viewed in the continuous live stream hosted by Nasdaq. (Update: The ad was retired in early 2016)

What isn’t visible is the half of the screen that wraps around the building. On that side is the story produced by BizBloom, the company behind the campaign. In the video above, you will occasionally see the logos for deBanked, BizBloom, and Quick Bridge Funding in the top left hand corner. The live stream has the ability to rewind up to the previous 3 hours. So if you don’t want to wait, rewind to different parts until you spot them.

Below is the video footage you can’t see that wraps around the other side of the building:

The purpose of the campaign, according to BizBloom’s Thomas Costa, is to tell the story of the American Dream, particularly the struggles and accomplishments of entrepreneurs.

Happy New Year.

‘Twas the Day Before New Year’s for Funders

December 31, 2015 ‘Twas the day before New Year’s, and all through the floor

‘Twas the day before New Year’s, and all through the floor

The staff was busy catching up, but being pushed for more

Submissions kept coming, most missing some stips

The most simplest of standards, the brokers always miss

The underwriters were dizzy, crunching numbers for hours

Getting hustled for approvals because they hold all the power

And management holding meetings, going over collections

Returns and defaults, and next year’s projections

When out of the blue, there arose such a clatter

The originators sprung up to see what was the matter

An announcement being made, attentive they listened

“Employees of the company!” said a face that glistened

With cheer in his eyes, and a non-familiar glow

Everyone was excited and frightened at the same time to know

He continued to explain, news that was both bad and good

Reflecting on the year, in terms they understood

With a lot of fluff talk, numbers, and percents

They knew at that moment, how it all made sense

Understanding their roles, and those who contribute

Appreciating their time and how they distribute

Now, closers! Now, admins! Now, marketing and relations!

Now, underwriting and sales! Anyone who had patience!

To the breakroom! To the breakroom with you all!

And they all huddled in, without an argue or a brawl

There on the table sat a wonderful spread

Snacks and desserts, more than enough to be fed

Stuffing their faces with enough food for two

The staff laughed and chatted though there was so much to do

“We can’t take a break! there’s so much to complete!”

“Though this is more than I ate all this week!”

This much is true- as many don’t know

They don’t leave their desks often, like elves at the North Pole

So back to their seats, with plates by their side

Back to reality, but they did it with pride

The realization of all of their hard work

It isn’t all that bad when you look at the perks

As the manager swung by to view his whole team

He realized it too, what isn’t always seen

It takes more than just one, it takes more than just vision

It takes a plan and people, to carry out the mission

As the time grew later, he knew what to do

Since nothing was funding in the late afternoon

He had another announcement which he said with great cheer

You’re all getting out early and have a Happy New Year!

Year of The Broker Concludes – 2015 Recap

December 31, 2015 It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

But there’s money being made. One broker is on pace to do more than $100 million worth of deals annually after working as a plumber eight years ago. Another went from sleeping in his car to driving a Ferrari. Meanwhile, brokers like John Tucker are basically saying just the opposite. Tucker has repeatedly taken to deBanked to preach things like “minimalism,” a practice of living below your means to a point where you can survive, and telling everyone it’s okay to embrace the satisfaction of a middle class life.

So is it the end of days or just the beginning?

In October, initial survey results of top industry CEOs revealed a confidence index of 83.7 out of 100, but out there on the street for the little guy, it’s been a tumultuous year. Things like commission chargebacks have hit brokers at unexpected times, with several funders privately telling us over the year that rogue brokers have closed their bank accounts or frozen the ACH debits in order to avoid giving the commissions back.

In 2015, brokers sued their sales agents and sales agents sued their employing brokers. Deals got backdoored, deals got co-brokered, and soliciting deals anonymously got banned from industry forums. Stacking continued mostly unfettered but is being pursued in the court system by funders allegedly injured by it. Brokers took over Wall Street and are supposedly being watched by regulators. Oh, and robo-dialing? Brokers should probably steer clear of that, just as underwriters should ditch paper bank statements.

It’s a lot to manage. Sometimes for a broker, just losing a deal can make them so sick that they have to go home. That’s apparently what happens when you don’t answer the phone fast enough. At least one said there’s no room left for more competitors so if you were thinking of starting a brokerage now, $2,000 won’t be enough.

But things could be worse. In 2015, IOU Financial was under attack by Russian nuclear scientists, a story that was more truth than exaggeration. In the end, Qwave Capital acquired a 15% stake in IOU.

An OnDeck class action lawsuit that looked bad at first turned out to be mostly based on the words of a convicted stock manipulator with a short position in the stock. The case is still ongoing and OnDeck’s stock price is down 50% from their IPO.

In 2015, two guys lost God but found $40 million (although numerous sources say that number is off).

“Madden” no longer means the football video game and Section 1071 is not a seating area in a stadium.

An RFI turned out to be something not to LOL about. Despite an overwhelming response from lenders and funders, the Treasury isn’t completely sold.

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Lobbying coalitions formed. NAMAA became the SBFA. The CFPB lied and community bankers testified.

But things are looking up. Brokers can obtain outside investments, get acquired, or make millions through syndication.

Bad Merchants are now ending up in more than one bad database, though a deal for the ages slipped through the cracks. Other merchants went to jail. Square went public and brought merchant cash advances along with them. The industry beamed its message through Times Square and one Democratic congressman has asked God to bless it all.

It was a crazy year. Marketplace lending became an acknowledged term (and the name of a conference) and already companies under that umbrella have been linked to presidential candidate (and desperate loser) Jeb Bush and the San Bernardino Terrorists. The FDIC had a few things to say and SoFi went triple-A. Marketplace lending is making a lot of people money, but when looking at the tax implications is there something funny?

In 2015, the big boys shared their wisdom and their figures. Turns out, it was beyond hyperbole. Brokers experienced an incredible rise or they pawned their ferrari to the other guys. Some focused on a specific crop, while others are trying it over the top. California sucked, John Tucker tucked, and one lender got totally F*****. In 2015 some funders got tanked, so in 2016 we’ll all be deBanked.

Happy New Year!

Details Emerge About the OnDeck – JPMorgan Chase Deal

December 30, 2015 The Wall Street Journal recently published many details about the recent OnDeck/JPMorgan Chase deal that everyone has been wondering about. Here are the cliff notes:

The Wall Street Journal recently published many details about the recent OnDeck/JPMorgan Chase deal that everyone has been wondering about. Here are the cliff notes:

- OnDeck will get fees to originate and service loans for Chase up to $250,000

- Chase’s small business loans will have terms of 6, 9, and 12 months

- Chase customers won’t know OnDeck is involved at all

- OnDeck will not get Chase’s declines

- OnDeck will process Chase’s business loan applications in a matter of hours instead of weeks

Perhaps most interesting of all is that Chase will be doing 6-12 month small business loans. 2016 should be a unique year. With a Chase loan approved in hours, the days of banks taking weeks or months to underwrite an application will be a thing of the past.