AI

Lending Tree: LLM Referrals Are Very “High-Intent Consumers”

March 3, 2026 During Lending Tree’s Q4 earnings call, CEO Scott Peyree echoed the same conclusion on LLMs that was uttered by rival NerdWallet, that LLM referrals convert better than normal search referrals.

During Lending Tree’s Q4 earnings call, CEO Scott Peyree echoed the same conclusion on LLMs that was uttered by rival NerdWallet, that LLM referrals convert better than normal search referrals.

“There are a number of fronts we are working on there,” said Peyree. “There is obviously the SEO front where you are getting referenced by the LLMs, driving consumers to our site. We continue to focus on that and it continues to grow. It is very high-intent consumers, as I have mentioned on previous calls. I would say, materially, it is still a pretty small percentage of our overall consumer base, but it is continuing to grow.”

Lending Tree hinted that there was an opportunity to capture more LLM traffic through paid LLM advertising going forward but that they couldn’t say to what extent yet for 2026.

“Some of the LLMs, ChatGPT being an example, are looking to start testing some advertising, which we are excited about participating in,” Peyree said.

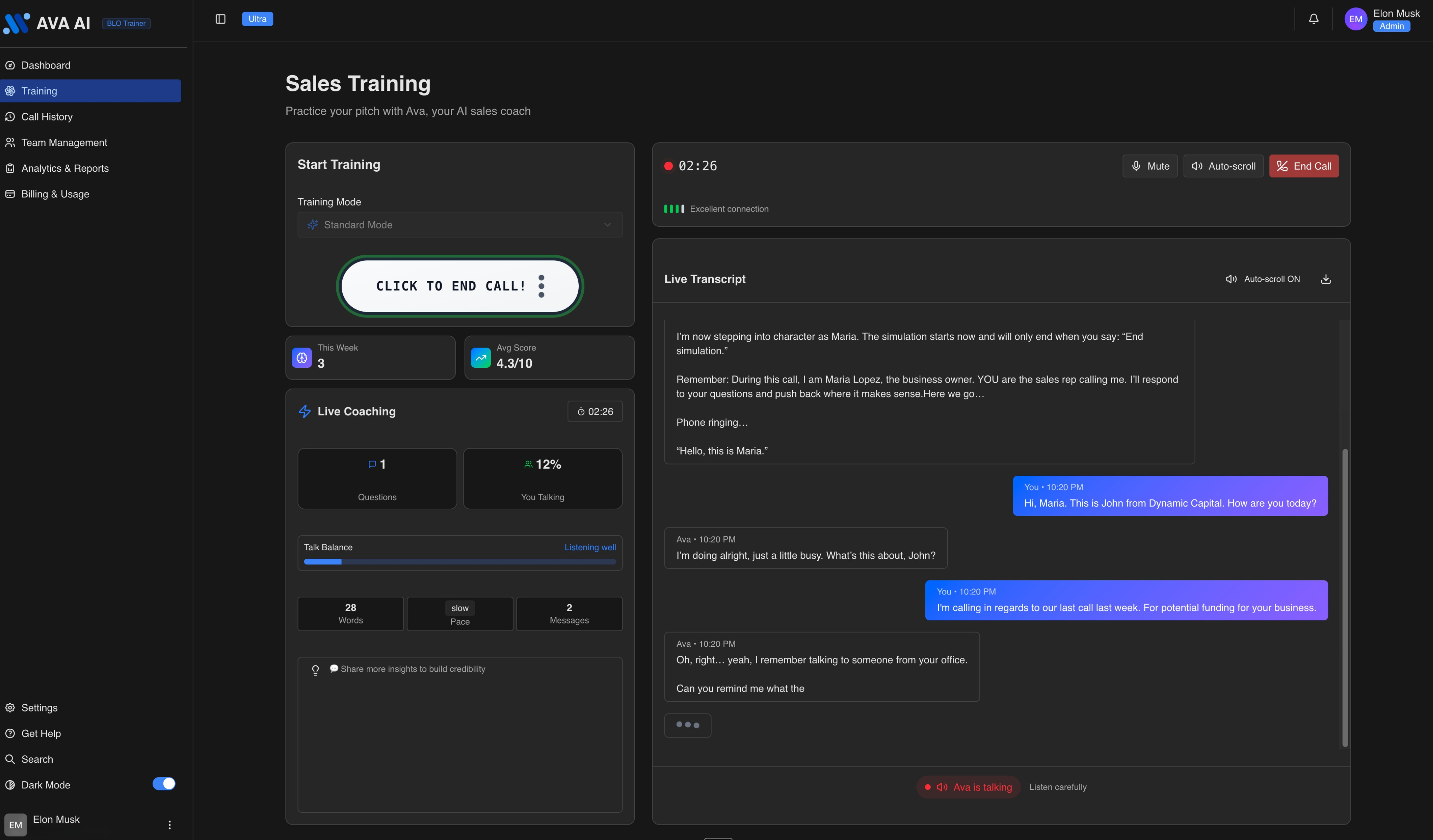

Getting Your Reps to Perform at the Ultimate Level? This ISO is Using AI to Train Them

February 2, 2026“I‘m unable to get 80, 90 guys to work in the area that I am in so I have to actually max out the team that I have,” says Steven Edisis, CEO of Dynamic Capital. “So my whole thing is onboarding guys and getting them to perform at the ultimate level.”

Edisis says that training small business finance sales reps takes extreme discipline, hours and hours of manual training. Training in the morning. Training in the afternoon. Training at night. Training and then some more training. Some of that training involves roleplaying. Other times it’s live calls. In either case, he’s found there are weaknesses in those systems. For instance, in a roleplay, the trainer has to contend with maintaining rapport with the individual they’re training. Persistent unfavorable feedback, even if warranted, could actually be demoralizing and create tension in the relationship.

“When you’re roleplaying with your buddy, your buddy’s a human,” Edisis says. “After two or three or four times of them getting it wrong, do you just stop correcting it? And you let it go.”

The end result is that they’re not actually in top shape and ready for calls, but they could be deceived into thinking that they are. Meanwhile, live-call training presents another dilemma. If you give the trainee good leads and they mess up, are the good leads wasted? And if you give them really cheap leads and they don’t get anywhere with them, how are they supposed to be judged or learn from it?

For Dynamic Capital, the solution to all of the above has been AI. About a year ago, Edisis began using an AI agent called Ava, a product by Reech AI that’s led by CEO Liran Weissenberg. Ava does for Dynamic Capital what Edisis did for a long time, trains, but on steroids. Trainees, experienced reps, and even veteran pros at the game can roleplay with Ava, a voice AI, in any setup of circumstances they choose. It can be a straight-up cold call, a warm lead, or a follow-up, for example. It can be tuned to easy mode, regular mode, hard mode, or even impossible mode. The best part is that Ava knows how to play the role of a merchant, speaks in real time, and speaks with human-believable tones and emotions. Voice AI technology, once considered clunky or plagued by latency in years past, has finally become virtually indiscernible from a real person.

In a live demo performed for deBanked to show it in action, the AI answered the phone and Edisis went right into the normal flow of business.

“This is Steven with Dynamic Capital. Last week you went online, requested some information for some working capital for your business, how are you today?”

“I’m ok, just a little busy right now,” Ava responded somewhat suspiciously. “yeah, I remember poking around online. I put in my info but I never really got a clear idea what you guys actually do.”

From there, Edisis played it out to a conclusion. When it was over, Ava rated him on his performance, gave him a score, and shared what he did well, as well as things he could have done better. It seemed to understand the relevance of open balances a merchant might have with loans or MCAs, which is key to making it impactful. Ava’s an AI, so a trainee would not be able to attribute the constructive criticism it offered to being singled out or picked on. For instance, if the AI said the trainee needed to work on tone and pacing of speech, there’s no way for the trainee to attribute that to personal bias from a trainer.

“The cool thing is that we can model the AI to behave in very specific scenarios and to have very specific analysis,” said Weissenberg of Reech AI, who created Ava.

Meanwhile, no real leads were wasted in the process. This is especially valuable since Edisis says that he teaches a specific technique—or rather, an art—called the interruption, a very delicate tactic used to keep a call on track. But it only works if delivered correctly, because it involves literally interrupting the prospect while they’re speaking. Learning how to interrupt in the circumstances that call for it is a massive gamble that could not only lead to lost sales revenue but also negative customer feedback if executed poorly. This is a perfect example of where AI training comes into play.

“It’s really nice to [practice it] on Ava versus blowing up and getting negative reviews from a live person,” Edisis said. “So that’s a really cool way that I can train people.”

Weissenberg said that when Ava is being used across a whole sales floor, a sales manager can view transcripts of all the calls, along with feedback and analytics. One could literally have a full-on simulated call center where all the prospects are AI agents being used to train reps.

“The coolest thing about the app is the analytics,” Weissenberg said. “It’s only going to get better too because AI is getting smarter and it’s getting more human.”

“On top of [new trainees], my other guys over the years—some have been here up to ten years—every once in a while they get a little rusty, revert back to bad habits, etc.,” Edisis said. “This allows me to keep them honest. And when some new person comes to me and tells me my leads are bad, I say, “let’s go to Ava… you tell me your pitch, I’ll do the same pitch.”

If Edisis significantly outscores them, it becomes evident that lead quality isn’t the issue, but rather all the other factors that go into having a successful call.

“It keeps some honesty between the program and reality,” he said.

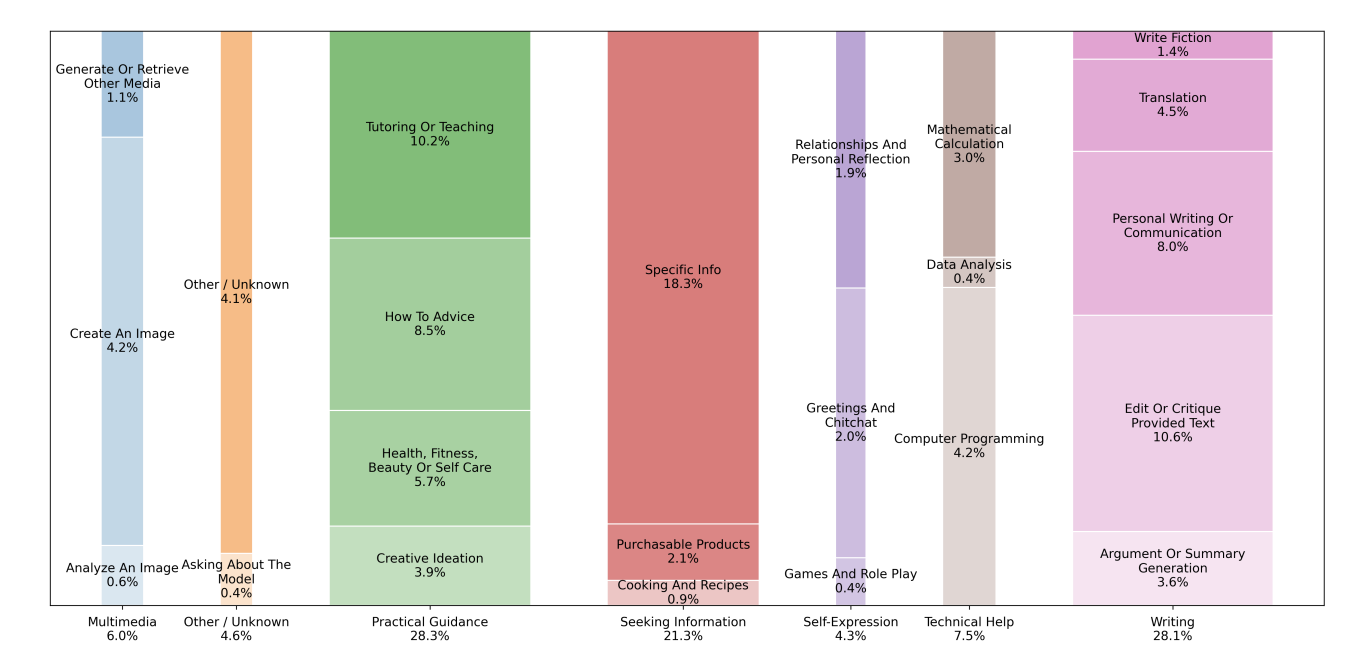

People Are Using AI as a Replacement for Search

October 6, 2025It used to always be Google when it came to search, but a recent study shared by OpenAI shows that people are using LLMs in a manner that is very similar to how they used Google.

21.3% of ChatGPT interactions, for example, are about seeking information, 28.3% are about practical guidance, and 7.5% are about technical help.

The data was based on 1.1 million sampled conversations between May 15, 2024 and June 26, 2025.

“While users can seek information and advice from traditional web search engines as well as from ChatGPT, the ability to produce writing, software code, spreadsheets, and other digital products distinguishes generative AI from existing technologies,” the report says. “ChatGPT is also more flexible than web search even for traditional applications like Seeking Information and Practical Guidance, because users receive customized responses (e.g., tailored workout plans, new product ideas, ideas for fantasy football team names) that represent newly generated content or novel modification of user-provided content and follow-up requests.”

ChatGPT’s crossover as a search engine is already going one step further. Last week the company announced that it was partnering with Stripe on in-chat checkout.

“The flow is simple: a ChatGPT user asks for product recommendations in the chat,” Stripe said of it. “When they are ready to buy, they are presented with a Stripe-powered checkout inline in the chat.”

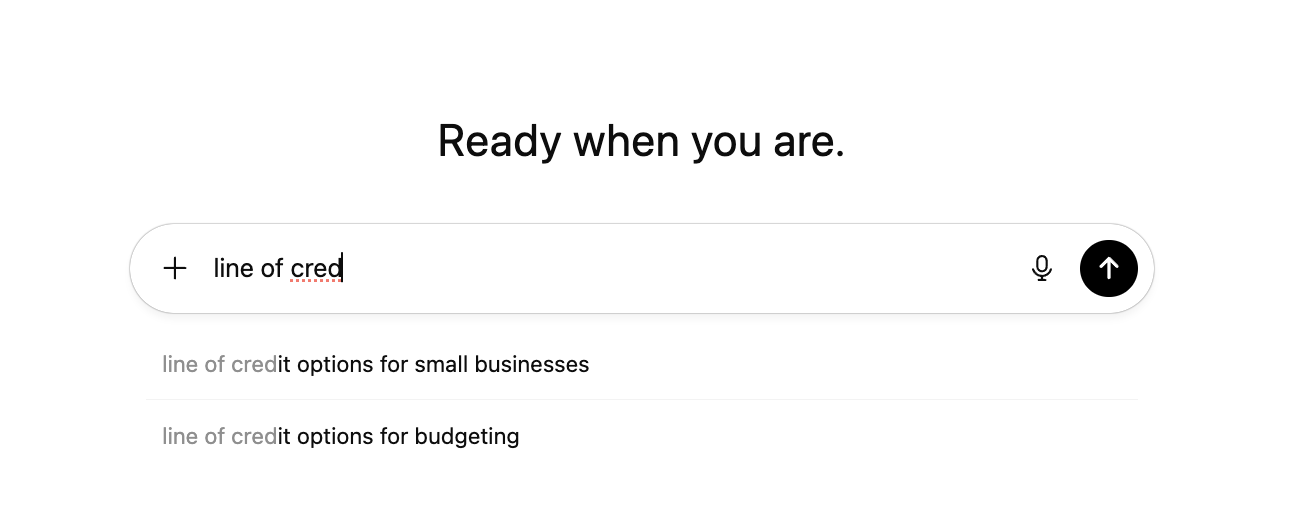

And just as recently, ChatGPT is now also leaning into auto-complete queries, similar to what Google already does.

Typing “line of cred” into a query box, for example, shows “line of credit options for small businesses” as a potential query for the user to choose from.

LendingTree: ‘Small Business Loan Originations Up 40% On Our Platform’

August 1, 2025LendingTree’s small business loan origination volume is up 40% YoY, according to the company’s latest quarterly earnings report.

“In small business, we made a strategic investment to grow our sales force and it has paid off in more business and more efficiency,” said LendingTree CEO Doug Lebda. “I think that small business can be a real growth driver for us.”

Lebda added that profitability had been consistently growing each quarter and that the company was “on a roll.” And part of that is being attributed to staying on top of AI.

“Eighteen months ago, I told our board and our company that we’re going to be an AI first company,” Lebda said. “And today, effectively, all of our employees are using AI in their day jobs, including having enterprise GPT for everyone.”

How SoFi is Approaching AI and Blockchain

July 30, 2025“We’re implementing and testing AI applications across our business from enhancing back office processes like dispute resolution and filing suspicious activity reports to improving how we interact with our members to help them get their money right, and we brought on teams of engineers to drive these efforts forward,” said SoFi CEO Anthony Noto during the Q2 earnings call.

While the company is using other innovative technologies like blockchain to allow customers to move money over crypto rails or to invest in the underlying cryptocurrencies themselves, they also see a role for it to effectively reintroduce peer-to-peer lending/investing.

“As we look further down the road, we see the potential to tokenize SoFi loans to make them more widely available in liquid markets in increments of dollars rather than tens of thousands of dollars such that anyone can invest in loans just like they do equities,” Noto said. “Crypto is a key area of focus for our management team and when we have brought on board significant expertise, including substantial engineering talent to advance these new initiatives.”

How AI is Scaling a Veteran Small Business Financing Brokerage to New Heights

March 19, 2025 “There are [AI] voice systems out there that have just blown me away,” said Cheryl Tibbs, owner of Atlanta-based Commercial Capital Connect. “So we are using those and I’m implementing some in my office in my day to day—we have an AI receptionist that answers the phone, it just frees up time.”

“There are [AI] voice systems out there that have just blown me away,” said Cheryl Tibbs, owner of Atlanta-based Commercial Capital Connect. “So we are using those and I’m implementing some in my office in my day to day—we have an AI receptionist that answers the phone, it just frees up time.”

As a broker, Tibbs recognizes the value of being able to answer a potential client anytime, anywhere, but there needs to be time to sleep, train others, and expand as well. And thanks to the advent of actual AI, it’s now become increasingly possible to scale on multiple fronts where it wasn’t before. Tibbs told deBanked that she’s been using AI to duplicate herself across anything she can.

“So we train these models on everything about our business, everything about us, and it can just answer questions, either through chat or having a conversation,” she said.

AI can call leads or qualify a customer through online chat at three in the morning if need be—not theoretically; it’s doing it for her already.

“Some mornings I wake up, I see full conversations between the conversational AI and somebody that filled out a lead form,” she said. “The chat agent has the ability to send them a text message with our full application link, or book them on our calendar.”

But more customers coming in the door means more questions from her team about where to place a deal. She’s got a solution for that, a bot she created named BrokerBuddy that can answer on her behalf when she’s not available to do it herself.

“I trained it on most of the lender guidelines that we work with, so they can just go in and just type a question, you know, ‘hey, BrokerBuddy, I’ve got a customer with a 680 FICO score.’ He says, ‘two years time in business, looking to buy a $40,000 skid steer. What else should I ask him? Which lender in our organization do you think will do this deal?'”

There’s a role for AI to just skip the questions and place a deal all by itself using advanced algorithms, something many tech companies tout these days, but the human nuance is a key component to her service, since any deal could be equipment financing, SBA, or working capital rather than solely one thing. It’s not always immediately obvious which one it’s going to be or what the customer would prefer. Way back in the day, Tibbs started purely with MCAs, back when they could only be done via a credit card machine. Since then she added equipment financing, working capital loans, and SBAs. For a long time now, she’s offered it all. She pairs up customers with the best fit and relies on her knowledge and relationships to know what’s going to work and what’s not.

“SBA is a hot button right now and merchants are really excited to know that this is definitely a possibility,” Tibbs said.

One opportunity with SBAs in particular is to consolidate MCAs, which, if the business owners qualify, can have a tremendous impact. Sometimes these business owners find her by seeing her posts online, and they reach out. Maybe it’s her they’ll get right away, or maybe it’s her AI. In any case, all of her experience has long since led other brokers to refer their own business to her, since she has a reputation for being able to get the deals done.

“I’ve been operating as a super broker most of the 20 to 25 years that I’ve been in this alternative space,” she said, “and as a super broker, I’m able to offer my broker partners more stuff than they even thought about. […] I study this stuff. I eat, live, and breathe it.”

While it’s unclear if AI qualifies as alive, her band of automated agents are beginning to breathe the rush of it all right alongside her. So many brokers (and lenders) are diversifying their product sets that her referral business is escalating, and she wouldn’t be able to scale without the assistance.

“Even though we get appointments, if we’re not on the phone with that merchant usually within three to five minutes, sometimes it’s hard to get them back on the phone. And even if they make an appointment, they may not show up. Having that instant engagement it definitely helps.”

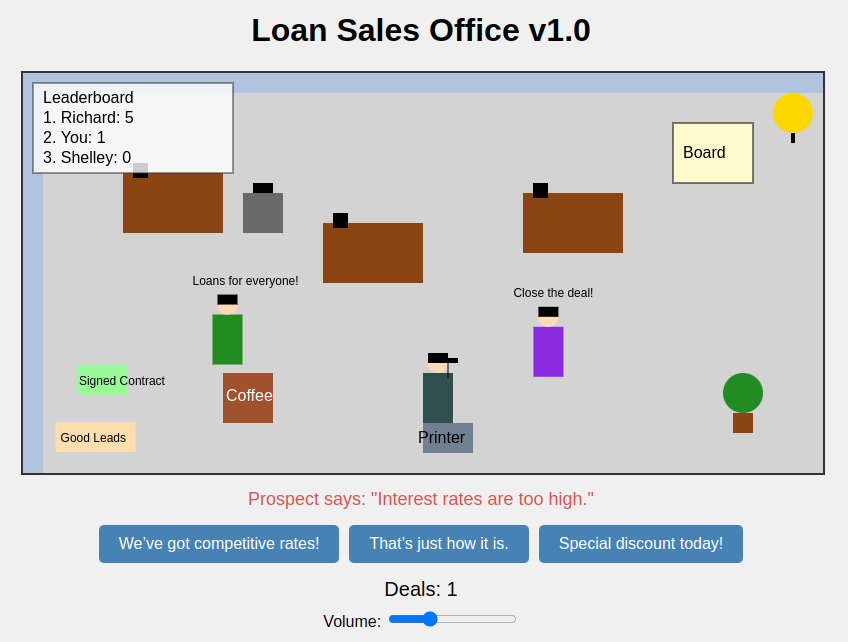

We Used AI to Make a Loan Broker Video Game

March 13, 2025As AI continues to progress beyond LLMs into doing just about anything one wants, I took the liberty of having it create a very simple javascript-based online game (for Desktop browsers only) to see what would happen. With about 5 minutes worth of work, it created something functional that it calls Loan Sales Office v1.0. The game gives the user the option to earn points either by answering a customer objection correctly or by moving the character around the office and racing against the NPC competitors to collect signed contracts. First one to 50 wins. It created the questions and answers itself.

The purpose of the exercise is to bring further awareness to AI.

If you are on a desktop browser, click below to try the game.

HOW TO PLAY

Compete against two other sales reps. First one to 50 deals wins.

Move your character with the keyboard arrows or the on-screen controls.

Collecting a signed contract = 5 deals

Answering a question right = 1 deal

The good leads are elusive. Signed contracts spawn at random.

Must use desktop browser. Good luck!