Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Trump, Republicans To Take Over in 2025

November 6, 2024 With the 2024 election results in, the regulatory and legislative environment for the small business finance industry could shift significantly at the federal level in the coming years. In particular, it will be worth paying specific attention to what happens with the Consumer Financial Protection Bureau (CFPB). As many readers are aware, the largest regulations ever imposed on the small business finance industry, promulgated by the CFPB, are slated to go in effect in July 2025. That date comes after fifteen literal years (Since Dodd-Frank was passed in 2010!) of delays caused by confusion, debates, and disputes over the CFPB’s right to exist, the meaning of the law’s statute, and court orders pushing it forward or temporarily delaying it. Feelings about the CFPB were so contentious under Trump’s last presidency that the agency temporarily rebranded itself as the BCFP (Bureau of Consumer Financial Protection) as a symbolic gesture of statutory defiance.

With the 2024 election results in, the regulatory and legislative environment for the small business finance industry could shift significantly at the federal level in the coming years. In particular, it will be worth paying specific attention to what happens with the Consumer Financial Protection Bureau (CFPB). As many readers are aware, the largest regulations ever imposed on the small business finance industry, promulgated by the CFPB, are slated to go in effect in July 2025. That date comes after fifteen literal years (Since Dodd-Frank was passed in 2010!) of delays caused by confusion, debates, and disputes over the CFPB’s right to exist, the meaning of the law’s statute, and court orders pushing it forward or temporarily delaying it. Feelings about the CFPB were so contentious under Trump’s last presidency that the agency temporarily rebranded itself as the BCFP (Bureau of Consumer Financial Protection) as a symbolic gesture of statutory defiance.

The CFPB’s looming oversight of small business finance starting next year had particularly alarmed those in the merchant cash advance space. Its current head, Rohit Chopra, had previously disclosed that his mission was to “wipe out” merchant cash advance companies. He had also said that the structure of their products “may be a sham.” In response, one trade group representing such companies filed a lawsuit against the CFPB earlier this year. That case has not been decided yet. Other segments of the small business finance industry will be watching the CFPB closely in 2025 as well.

Another outcome is that it could mean that individual states that lean the other way politically become more aggressive. As readers are aware, the stream of disclosure legislation over the last few years all came from the state level. It’s possible that environment starts to accelerate even faster.

Meet the CAFE That Can Accelerate Your Fintech Startup

October 14, 2024 Newer fintechs on a mission to advance financial health and wellness for low-to-moderate income individuals and underserved populations may not have to weather the startup journey alone. Inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus, is the non-profit Center for Advancing Financial Equity (CAFE). Supported by numerous partnerships including the Small Business Administration, Discover, the Small Business Development Center (SBDC), the American Bankers Association, and more, one of its signature initiatives is its bi-annual fintech accelerator, which aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort of the accelerator. One of those selected this past Spring, Parlay, offers a powerful tool to improve small business loan applications. Another, Stratyfy, offers interpretable AI solutions that enable financial institutions to make more accurate, efficient, and fair financial decisions in credit risk, fraud, and compliance.

Newer fintechs on a mission to advance financial health and wellness for low-to-moderate income individuals and underserved populations may not have to weather the startup journey alone. Inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus, is the non-profit Center for Advancing Financial Equity (CAFE). Supported by numerous partnerships including the Small Business Administration, Discover, the Small Business Development Center (SBDC), the American Bankers Association, and more, one of its signature initiatives is its bi-annual fintech accelerator, which aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort of the accelerator. One of those selected this past Spring, Parlay, offers a powerful tool to improve small business loan applications. Another, Stratyfy, offers interpretable AI solutions that enable financial institutions to make more accurate, efficient, and fair financial decisions in credit risk, fraud, and compliance.

Being accepted into CAFE requires a startup to already be up and operating.

“[These companies are] in market, the products are built already,” said Kristen Castell, Managing Director of CAFE. “They do have some customers, some of them are enterprise customers like banks, a full time team, and many of them have raised money already.”

Castell tells deBanked that the companies applying to the accelerator still need a lot of help in terms of making industry connections, scaling distribution, and developing the right partnerships. It’s an eight-week program, some of which takes place on location at the Fintech Innovation Hub in Delaware. The rest is virtual. Applicants and those selected can be from anywhere in the US. The founders, all connected by some level of common interest, are bound to form a bond throughout the unique experience. Last week for example, the members of the Fall cohort went on a field trip to the Wilmington, Delaware headquarters of Best Egg (F/K/A Marlette), an online lender, and got to learn about their path from being a startup in 2014 to the fintech stalwart they are today.

“This time, we have some opportunities to meet the American Bankers Association in Washington, DC,” Castell said. “We also meet the regulators at CFPB in Washington, DC. There’s some other conference opportunities like another accelerator called RevTech Labs that has an investor conference in Charlotte. So there’s an opportunity to pitch there to investors.”

The learning curve for any company coming through the accelerator is dramatically shortened by the access and guidance they get, whether that be from other fintechs, from bankers, from regulators, or the largest fintech trade association, the American Fintech Council.

At the end of it all there’s a demo day in person at the Fintech Innovation Hub in Delaware, where they present to investors, bankers, academics, industry and community leaders, non-profit organizations and entrepreneurs alike to show what they’re made of.

Castell, a former banker herself that previously worked for JPMorgan and BlackRock, also experienced a taste of being a fintech entrepreneur when she became interested in impact investing. It’s a scene she loves. When the plan for CAFE was in development, the opportunity to be involved with financial inclusion, technology, and startups all in one was something she really wanted to take on.

“It’s really been an incredible opportunity to build the organization, to build the program, to work with all these partners, to bring all these stakeholders that I had mentioned earlier in and we’re not done,” she said. “We’re just getting started.”

The six members of the Fall cohort are Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm. Sponsors include the American Bankers Association (ABA), Siegfried Advisory, Delaware Prosperity Partnership (DPP), Wolf & Co, Delaware Tech Park, deBanked, and Discover Financial Services.

deBanked is expected to attend the demo day in November.

How Erica Bell of Tax Guard Won Second in The Poker Tournament

October 13, 2024

When the final hand of the B2B Finance Expo’s official poker tournament had concluded, Erica Bell, a Business Development Account Executive for Tax Guard, walked away with 2nd place. Bell has enjoyed poker for a long time and knows the game well. She’s even played in tournaments at the Ameristar Casino in Blackhawk, Colorado and won 1st place in one of them.

“The game’s strategy is what I truly enjoy,” Bell told deBanked. “A couple of individuals came up to me and congratulated me [on coming in 2nd].”

Bell, who at least took home a small prize, has worked for Tax Guard for 5 and a half years. For those not familiar, “Tax Guard is a 3rd party due diligence company who provides real-time insights into hidden tax debt of individuals and businesses by retrieving and analyzing IRS data directly from the source, the IRS,” she says.

The company’s services are primarily used by commercial lenders and financial institutions to assess tax-related risks associated with borrowers. Tax Guard is widely known throughout the industry and has been frequently referenced on deBanked. The company’s co-founder and CEO, Hansen Rada, even did a Zoom interview with deBanked during the early lockdown era of Covid.

The company’s value is pretty straightforward, a lot of tax debt is not easily discoverable, and they’ll get the info you don’t even know you’re missing straight from the source.

“By offering earlier visibility into potential tax issues, liabilities, liens, & levies, we help our customers make more informed lending decisions and mitigate financial risks,” Bell explains.

And if there is a hidden tax issue, Tax Guard can proactively work to resolve it and even negotiate a payment plan. One downside of ignoring tax debt as a lender is having to compete with the IRS when they ultimately move to enforce collection.

Clients can use the Tax Guard portal to run reports or integrate their API right into a CRM. Other critical information can be obtained as well including a wage and income transcript from the IRS. “This includes data from W-2s, 1099s, and other income forms, as well as withholding details,” Bell says. “This data provides a comprehensive view of a taxpayer’s reported income and can be critical when assessing financial risks, resolving discrepancies and verifying financial details.”

Obviously, Bell says that anyone interested in learning more can reach out to her directly.

“My role is highly dynamic, being sales, strategic partnership and relationship focused,” Bell says. “I really enjoy working with extremely talented people at Tax Guard, meeting new folks in the finance industry and learning from their perspectives.”

She’s also apparently planning to host her own upcoming friendly poker tournament so it’s safe to say she has no intention of letting her skills get rusty.

How Cesar Valero Won The Tournament And Gets Deals Done

October 2, 2024

When Cesar Valero, Business Development Executive at Spartan Capital, sat down at one of the starting poker tables late last month to participate in the kick-off tournament for B2B Finance Expo, it had been almost exactly a year since he last played. His colleague Ryan Capella had finished second that time, which coincidentally had also been for a business event in Las Vegas. But here at B2B in 2024, the Spartan team was competing against a mix of players eager to show off their skills, some of whom play semi-professionally on the side.

According to Valero, they didn’t do any kind of practice ahead of time. “Frank [the CEO] just said ‘make sure you represent,'” he said. And after two and a half hours of impressive play that’s exactly what he did. The dealer and a hired pit boss keeping an eye on all the cards declared Valero the winner where he took home the grand prize gold bracelet and other goodies.

“We were actually really happy because we noticed that–obviously we celebrated a little bit–and then noticed after we’re like, ‘of the top four positions of the last two years, we [Spartan] have two’ that’s pretty good,” Valero said.

But more importantly, at the industry’s largest conference of the year, everyone suddenly knew who Valero was if they didn’t before.

“You can flat out tell them the best marketing at B2B was to win the poker tournament,” Valero said. People came up to him throughout the next two days calling him out by name. “Hey, Cesar!” they shouted, after having heard about his win.

And being the guy everybody wants to talk to is pretty much his job anyway. Spartan Capital provides revenue based financing and works with a large number of referral partners. Valero’s day-to-day is typically spent communicating with ISOs, whether it be phone calls or Zoom calls or in-office meetings, he is catering to what they need and trying to get deals funded. When asked if having a relationship with an ISO is an important part of the job, he said it’s the whole job.

“We’re a fair funder,” he said of Spartan. “We really don’t snub anybody out. Whether you’re the biggest guy in the space or the smallest guy in the space, we’re going to do our best to give you the best customer service we can. Our reps, pretty much nobody is a brand new rep. Everybody’s got experience. They know what they’re talking about.”

“Most deals are pretty straightforward,” he said, “but you always have that 10,15,20% that need a little more love…so it’s a fast paced environment and just try to keep up with it, make sure we’re doing the right service to our customers whether it be an ISO or a [merchant].”

Overall, Valero feels like the industry is on a strong trajectory, especially with tech and e-commerce platforms having rushed in to offer similar funding products to their customers.

“If they’re in it, they see the demand right?” he exclaimed, “and if they’re putting out billions of dollars like I see every quarter in press releases from Amazon or from PayPal or from one of the big players, they’re out there and they’re creating buzz… so better quality borrowers will be flowing in because the need is there across the board.”

Valero isn’t exaggerating about the fast pace. After having gone from the flow of deals to Vegas to even more deals, he couldn’t afford to let our interview about his big win go over the allotted time.

“I got about an hour and 15 minutes to the wire cut-off,” he said emphatically while thanking me for the call. “Let me see if I can do a couple more deals!”

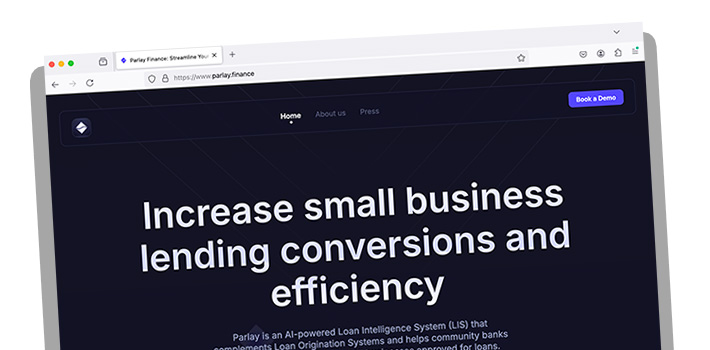

Applicant Didn’t Complete their Business Loan Application? They Might’ve Gotten Stuck

September 26, 2024 “Early discovery showed us in the market that over 85% of [small business] loan application packets were straight up abandoned,” said Jay Long, COO and co-founder of Parlay.

“Early discovery showed us in the market that over 85% of [small business] loan application packets were straight up abandoned,” said Jay Long, COO and co-founder of Parlay.

In an era where fintechs have sought to increase the speed and accuracy of the underwriting process, Parlay, an AI-native SaaS company, noticed that one major lingering challenge for small business lenders starts well before today’s tech stacks even come into play. For example, an applicant might not be sure what they’re supposed to be submitting to the lender in the first place and thus the process may never even make it to the fintech underwriting stage. This bottleneck comes at a cost for both a lender who fails to move a loan application forward and for a borrower who gets stuck and isn’t able to get what they wanted.

“A lot of small businesses when you request a bunch of stuff in an email or you just say ‘give me these things,’ they may not have the financial background, that financial education to know how to answer those questions,” said Alexandra McLeod, CEO and co-founder of Parlay. “And so what we’ve done is we’ve built a series of really intuitive, user-friendly, plain-English workflows that are easy and rapid to get through but also systematic.”

Parlay’s Loan Intelligence System (LIS) was drawn from interviews with hundreds of small businesses and also by observing how they did with existing workflows.

“We’re asking them yes-no questions, and based on how they answer, then the questions arrange themselves in a specific way,” said McLeod. “But also, we have tool tips in the platform, so if somebody doesn’t know what a term is or if they need help building something—like a debt schedule is something they have to provide, and people don’t know how to generate those, then we have these builders in the workflows to help them with that.”

At present, Parlay is focused on SBA 7(a) loans with their most common customer being a community bank or credit union. The company’s focus on the intake process has also enabled their technology to do even more, and that is to nurture applicants that are not eligible for approval to eventually become eligible through personalized actionable recommendations.

According to Parlay, their LIS easily integrates with existing Loan Origination Systems and it improves profitability without increasing overall business risk.

For McLeod, who has a prior background with financial inclusion initiatives and startups, she’s seen firsthand that there are financial institutions eager to provide capital to the underserved but that the economics to do it with legacy systems at scale have just made it too cost prohibitive. “The other side of the problem is the small business needs more hand holding,” said McLeod, “and the lender can’t provide it. And so this is a perfect application of technology where you can offer a scalable alternative where you can handhold the small business, you can provide a lot more insight to the lender as to the needs of those small businesses and you can generate that outcome of more booked loans because more people can actually get through the process.”

Notably, Parlay is a recent graduate of the Center for Accelerating Financial Equity (CAFE) Fintech Accelerator Program, which supports fintechs advancing health & wellness of underserved populations. CAFE is headquartered in the Fintech Innovation Hub building on University of Delaware’s STAR Campus, a building deBanked covered in 2022.

See You in Las Vegas

September 18, 2024 We’ll be in Las Vegas for the inaugural B2B Finance Expo (a deBanked / SBFA collaboration). Tickets are just about sold out so if you haven’t bought one already, check the site to see if registration is still active. It will turn off automatically.

We’ll be in Las Vegas for the inaugural B2B Finance Expo (a deBanked / SBFA collaboration). Tickets are just about sold out so if you haven’t bought one already, check the site to see if registration is still active. It will turn off automatically.

Here’s what you need to know:

Sept 22, Wynn, Las Vegas, 7-10pm: B2B Finance Expo Poker Tournament

- Anyone can attend to watch and network FREE. Cash bar on site.

- Seats to play are limited. Must be done in advance on the registration page. Seats almost sold out. Game is not for cash. $100 entry fee. All entry fees donated to GreenLedger, a new non-profit.

- Winner of the tournament gets a genuine gold B2B engraved championship bracelet.

Sept 23-24, Wynn, Las Vegas: B2B Finance Expo

- See agenda

- LOWER CONVENTION PROMENADE

- Tickets required for entry

Please be sure to stop by the Small Business Finance Association’s booth (SBFA) to learn more about the non-profit organization.

Other trade associations with representatives in attendance include the National Private Lenders Association (NPLA) and the Innovative Lending Platform Association (ILPA).

Trade media in attendance will include: deBanked, Coleman Report, and Equipment Finance News.

Please be sure to check out the booths of Kapitus & Rapid Finance (Diamond Sponsors) and Bitty & Lendini (Platinum Sponsors).

For event related questions email events@debanked.com. Event staff will not be able to answer calls after Thursday, 9/19.

B2B Finance Expo Poker Tournament Details

September 17, 2024 Seats for the B2B Finance Expo Poker Tournament are almost full. The non-cash competition is happening on the evening of September 22 from 7pm – 10pm PT at The Wynn Las Vegas. Anyone registered for the conference is eligible to register for the tournament while seats last. The grand prize is a 14k gold B2B championship bracelet, an optional interview for a story about your company on deBanked, and a few other goodies. The tournament is an excellent way to network with potential partners and peers while sizing up the competition!

Seats for the B2B Finance Expo Poker Tournament are almost full. The non-cash competition is happening on the evening of September 22 from 7pm – 10pm PT at The Wynn Las Vegas. Anyone registered for the conference is eligible to register for the tournament while seats last. The grand prize is a 14k gold B2B championship bracelet, an optional interview for a story about your company on deBanked, and a few other goodies. The tournament is an excellent way to network with potential partners and peers while sizing up the competition!

Location: The Wynn Las Vegas – Pomerol Ballroom + outdoor patio

The entry fee is $100 (select the poker tournament at checkout). 100% of the revenue collected from the entry fees will be donated to GreenLedger, a new non-profit initiative to curtail predatory debt consolidation companies in the small business finance industry.

“GreenLedger’s mission is to work directly with our small business clients to stabilize their revenue-based financing debts and avoid defaulting on their agreements, eliminating the need for potentially predatory middlemen and bad practices of debt consolidation.”

Anyone who wishes to watch but not play can attend FREE. There will be a bar there.

They Offered to Reduce My MCA Payments. I Played Along.

September 3, 2024 It started when I got a cold text that said my merchant cash advances could be reduced by 80%. I didn’t have any advances but was intrigued by the audacity of the offer. REDUCE THEM BY EIGHTY PERCENT!

It started when I got a cold text that said my merchant cash advances could be reduced by 80%. I didn’t have any advances but was intrigued by the audacity of the offer. REDUCE THEM BY EIGHTY PERCENT!

“Ok,” I thought to myself, “I’ll bite to see where this goes.”

I replied and was assigned a rep via text who introduced himself by name, Mark.

I told Mark I believed his offer to be a scam and sent him a link to an article (that was literally on deBanked) in which someone making similar offers had been arrested by the FBI. I was 100% confident that he would disappear but he was undeterred.

“Those were shady companies,” Mark said, assuring me he had nothing to do with them. I wondered if Mark had caught on to who I was because he seemed eager to convince me he was legit. He told me that I’d still have to pay my advances in full but that he would just get the payments for them reduced. That seemed unusually tame compared to what I’d heard about these type of encounters with “debt relief” companies but Mark kept talking.

By signing up with them I’d be assigned a lawyer who would have “leverage” over my MCA provider due to them likely being in default on their own contract. He explained that they were always in breach for failing to reduce the daily payments (a likely reference to reconciliation clauses). Mark’s fee for helping me take advantage of this, the cost of which was not mentioned, would be included in my new regular payments they’d negotiate for me.

Just as I was beginning to realize that I’d be on the hook for paying them for their service on top of apparently still paying my advances, the messages over texts stopped, and he tried to only continue the conversation by phone, which I avoided.

From there robocalls hit my phone 4-5x per day as they attempted to reel me back in until they eventually tried texts again. When they did the offer had changed from them being able to reduce my payments by 80% to only 50%. Weird. Nevertheless, I wanted to get back to where we had left off, finding out the cost of this service, of which I now learned included legal representation by an attorney and a separate case manager. It sounded like it would be very expensive for me and I let him know my concerns. If Mark had known who he was actually speaking to before, the attempt to play it off now had been forgotten.

From there robocalls hit my phone 4-5x per day as they attempted to reel me back in until they eventually tried texts again. When they did the offer had changed from them being able to reduce my payments by 80% to only 50%. Weird. Nevertheless, I wanted to get back to where we had left off, finding out the cost of this service, of which I now learned included legal representation by an attorney and a separate case manager. It sounded like it would be very expensive for me and I let him know my concerns. If Mark had known who he was actually speaking to before, the attempt to play it off now had been forgotten.

“Our program is not designed to cost you any additional money,” Mark said. “We go after unpaid fees and interest. You will never have to pay us out of pocket.”

And so that was the pitch, wordplay designed to make it appear the service was free and I would never have to pay them.

The website they referred me to included obviously fake testimonials with stock photos. They were “Trusted”, “Approved” and had been seen on various TV networks. It promises to stop withdrawals from funding companies and that their “in-house licensed attorneys” based in Florida and New York will take care of everything. The 7 month old website, which lists no business address, also claims the team has a decade of experience while the legal entity itself does not appear to exist, at least not in all the states I checked.

As I attempted to track down anything about this company I could find, a breakthrough led me to an address in Miami, which as fate would have it was home to another debt relief company targeting businesses with merchant cash advances. The website is similar. They are “Trusted”, “Approved” and seen on TV. They can also improve cash flow by up to 80%. What a coincidence. The owner of this one also has a colorful background with the law. Although I was not able to fully confirm that this company is the alter-ego of the other, I learn that this second company was just sued in April for allegedly absconding with a merchant’s funds it claimed was being used to pay off MCAs. In another instance the debt relief company is suing a merchant for the recovery of over $400,000, the sum of which it claims was its fee for trying to reduce a merchant’s MCA payments. It would seem that such work is not so free after all.

As my phone continues to ring and ring with offers to reduce my MCA payments, I decide to disengage.

“Sean, how many loans do you have?” Mark resumes. “Sean we will reduce your payments by at least 50%, let’s discuss.”

I ignore him. When he tries me again, he tells me he can reduce the payments by 80%. Then again later by 50%. He never tells me why it changes. His last message more than several months later is a return to the same script.

“Sean, Do you have MCAs hurting your cash flow?”

I’m pretty sure that he can’t be trusted. If your sales drop, you should call your funding company to discuss and stay away from shady pitches like this.