Articles by deBanked Staff

OnDeck Repurchased 3.2M Shares, Reports $8.7M Q3 Profit

October 24, 2019 OnDeck announced this morning that it has repurchased 3.2M of its own shares for $11M since making its buyback announcement on July 29th. The company intends to repurchase another $39M worth.

OnDeck announced this morning that it has repurchased 3.2M of its own shares for $11M since making its buyback announcement on July 29th. The company intends to repurchase another $39M worth.

OnDeck was profitable in Q3, reporting a net income of $8.7M on originations of $629M. Although that was an increase over the previous quarter, the year-over-year decline was said to be a reflection of “tightening underwriting criteria and market dynamics.”

The average term loan was for $56,000 with an average maturity of 13 months. The company’s line of credit program is growing and now accounts for 21% of the company’s total loans and finance receivables at quarter-end, up 15% from last year.

“OnDeck expects the current operating environment to extend into 2020 with increased profitability,” their quarterly report said.

LendIt China 2019 is Canceled

October 23, 2019 LendIt Fintech has officially announced that there will be no conference in China this year after 3 long years in the country. A blog post written by LendIt Fintech co-founder Peter Renton explained that calamitous events engulfing the peer-to-peer lending industry there, namely the abundance of fraud, and the government’s waning tolerance, has led them to believe that no lending companies will be interested in speaking, sponsoring or even attending this year.

LendIt Fintech has officially announced that there will be no conference in China this year after 3 long years in the country. A blog post written by LendIt Fintech co-founder Peter Renton explained that calamitous events engulfing the peer-to-peer lending industry there, namely the abundance of fraud, and the government’s waning tolerance, has led them to believe that no lending companies will be interested in speaking, sponsoring or even attending this year.

“We will regroup in 2020 and hopefully will be able to bring our unique event back to China,” Renton wrote.

The decision only applies to their Lang Di Fintech China event. Their US event is scheduled to take place in New York this year on May 13-14 at the Javits Center. That event will be immediately followed by deBanked’s Broker Fair 2020 at the brand new Convene at Brookfield Place on 225 Liberty Street in New York on May 17-18.

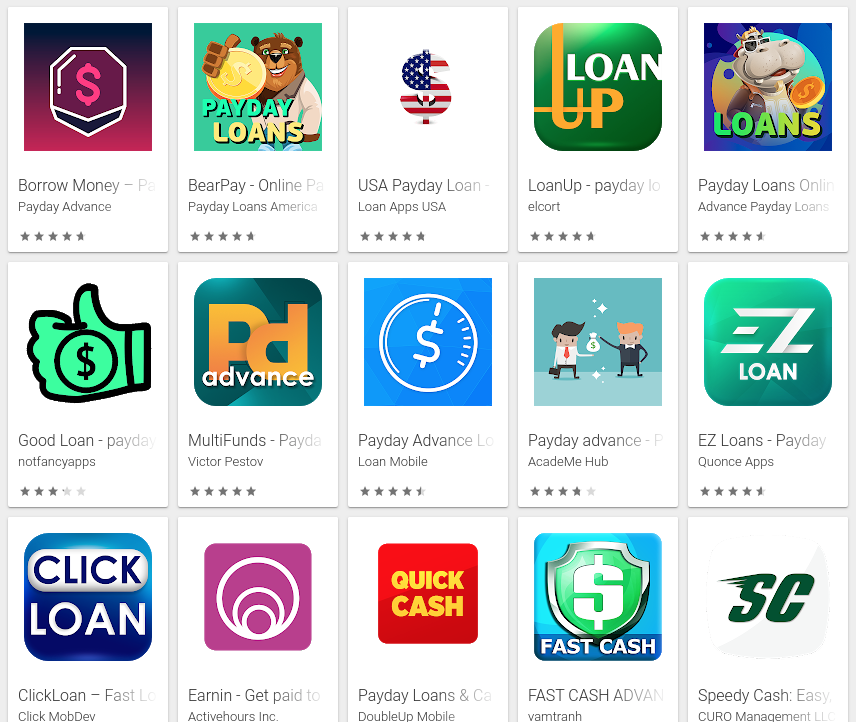

Google Bans Loan Apps From App Store If Personal Loan Offers Exceed 36% APR

October 12, 2019

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

Google is implementing new rules for consumer lenders who have apps in the Google Play app store. And they’re pretty strict. If a lender offers loans that exceed 36% APR, their app will be banned. If the repayment period of the loan is 60-days or less, the app will be banned.

It doesn’t matter what lenders call these loans, at least according to Google’s updated policy. “Peer-to-peer loans” were used as just one example of a loan category subject to the new rules.

Despite the new rules and a WSJ story announcing that payday loans had been shut out of the platform, deBanked determined that hundreds of payday loan apps are still available for download. This includes Nas-backed Earnin which is under investigation by regulators in multiple states.

Google banned payday loan ads from its search result pages in 2016. The move was viewed in some circles as hypocritical since Google’s VC arm, Google Ventures, had just invested in a payday lender (LendUp) that offered loans in excess of 400% APR. However, LendUp was also affected by the ban, a move that LendUp’s then-CEO Sasha Orloff embraced. Orloff blogged about the irony, writing, “If effectively enforced, Google’s ban will push the payday loan marketing competition away from ads and toward natural search, where safer alternatives with quality content can shine.”

Perhaps Google aims to achieve a similar objective with its app store.

The full text of Google’s new personal loan rule for its app store is below:

We define personal loans as lending money from one individual, organization, or entity to an individual consumer on a nonrecurring basis, not for the purpose of financing purchase of a fixed asset or education. Personal loan consumers require information about the quality, features, fees, risks, and benefits of loan products in order to make informed decisions about whether to undertake the loan.

- Examples: Personal loans, payday loans, peer-to-peer loans, title loans

- Not included: Mortgages, car loans, student loans, revolving lines of credit (such as credit cards, personal lines of credit)

Apps for personal loans must disclose the following information in the app metadata:

- Minimum and maximum period for repayment

- Maximum Annual Percentage Rate (APR), which generally includes interest rate plus fees and other costs for a year, or similar other rate calculated consistently with local law

- A representative example of the total cost of the loan, including all applicable fees

We do not allow apps that promote personal loans which require repayment in full in 60 days or less from the date the loan is issued (we refer to these as “short-term personal loans”). This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.

High APR personal loans

In the United States, we do not allow apps for personal loans where the Annual Percentage Rate (APR) is 36% or higher. Apps for personal loans in the United States must display their maximum APR, calculated consistently with the Truth in Lending Act (TILA).

This policy applies to apps which offer loans directly, lead generators, and those who connect consumers with third-party lenders.

New York Attorney General Secures Judgment Against Cardis Enterprises International

October 11, 2019 New York Attorney General Letitia James announced today that she had secured default judgments against numerous entities and individuals involved in a $30 million fraud.

New York Attorney General Letitia James announced today that she had secured default judgments against numerous entities and individuals involved in a $30 million fraud.

In December 2018, the New York Attorney General’s Office filed suit against Cardis and company personnel Aaron Fischman, Stephen Brown, Steven Hoffman, and Seth Rosenblatt for participating in the fraudulent marketing of Cardis to investors. The complaint further alleged that, while Cardis was raising significant investor funds, Fischman was fraudulently diverting much of the proceeds to enrich himself, family members, and his favored charities.

Default judgments were entered against Cardis Enterprises International N.V., Cardis Enterprises International (U.S.A.) Inc., Cardis Enterprises International B.V., and Chosen Israel LLC, along with several individuals related to Aaron Fischman as relief defendants.

“The case remains ongoing with several motions pending,” the AG wrote in a public statement, “including a motion for leave to amend the complaint to re-plead claims against Stephen Brown (who was previously dismissed from the case) and the remaining defendants.”

Coinbase Begins Paying Interest Rewards On Crypto Holdings

October 2, 2019

Bitcoin’s price might not be all that right now, but Coinbase, a US-based digital currency wallet, wants to pay its customers a reward for holding on to its stablecoin. Unlike Tether, a popular stablecoin that was purportedly fully backed by US dollars but then revealed it wasn’t, Coinbase’s stablecoin is fully backed by dollars on deposit in a bank.

Bitcoin’s price might not be all that right now, but Coinbase, a US-based digital currency wallet, wants to pay its customers a reward for holding on to its stablecoin. Unlike Tether, a popular stablecoin that was purportedly fully backed by US dollars but then revealed it wasn’t, Coinbase’s stablecoin is fully backed by dollars on deposit in a bank.

The advantage of a stablecoin, in theory, is the stability and safety of the US dollar combined with the fluidity of cryptocurrency. Coinbase’s stablecoin is called USDC and as of Wednesday, the company will begin paying holders of the coin an annualized reward of 1.25% APY. That’s a little bit less than a high yield savings account. It’s interest but it’s technically not. Unlike a bank, Coinbase won’t be using your funds to facilitate loans to generate income so that it can pay out interest to depositors. Instead, the company claims, “You simply earn while storing your crypto safely on Coinbase.”

Coinbase disclaims the offer by reminding users that their funds are not FDIC insured and that the digital wallet is not a deposit account or savings account.

$176 million of USDC exchanged hands in the last 24 hours as of this post being written.

The crypto faithful, users whose optimism in cryptocurrency has been unwavering, have quietly been looking for an alternative stablecoin to Tether. Tether has been locked in a battle with the New York Attorney General and recently revealed in court documents that its stablecoin was not as well backed as the company had claimed.

deBanked Around The World

September 28, 2019 Members of the deBanked editorial team returned from Ireland this week. The Republic of Ireland will be the latest in our international series on nonbank finance. Stay tuned for our stories on that.

Members of the deBanked editorial team returned from Ireland this week. The Republic of Ireland will be the latest in our international series on nonbank finance. Stay tuned for our stories on that.

In the meantime, be sure to check out our international coverage of:

Canada

- Canada story series

- Magazine Feature: Canada’s Alternative Financing Market Is Taking Off

- Canadian Funder Directory

Australia

- Australia story series

- Magazine Feature: Snapshot on Australia: Growth in the making

- Australia Funder Directory

Hong Kong

Mexico

Head of MyPayrollHR Charged in Massive Nine-Year Bank Fraud

September 23, 2019 When MyPayrollHR left thousands of companies and their employees high and dry without their paychecks earlier this month, suspicion grew that the company’s rather mysterious owner, Michael Mann, may have been involved in some unsavory business. New information has emerged that around that time, Mann voluntarily checked in to the US Attorney’s office in Albany and admitted to a fraud he’d been running for 9 long years.

When MyPayrollHR left thousands of companies and their employees high and dry without their paychecks earlier this month, suspicion grew that the company’s rather mysterious owner, Michael Mann, may have been involved in some unsavory business. New information has emerged that around that time, Mann voluntarily checked in to the US Attorney’s office in Albany and admitted to a fraud he’d been running for 9 long years.

Since then, according to the Department of Justice, “Mann fraudulently obtained at least $70 million in loans from banks and other financial institutions. He created companies that had no purpose other than to be used in the fraud; fraudulently represented to banks and financing companies that his fake businesses had certain receivables that they did not have; and obtained loans and lines of credit by borrowing against these non-existent receivables.”

He has not paid them back. By the end, Mann resorted to kiting checks, the DOJ claims, in that he wrote checks back and forth to himself at different backs to inflate the balance of one or more accounts.

His largest creditor, Pioneer Bank, is owed tens of millions. Earlier this month, Mann attempted to route funds meant for his customers’ payrolls to an account at Pioneer Bank. Pioneer Bank responded by freezing all of the funds, causing all of MyPayrollHR’s clients to get caught in the crossfire.

Mann is charged with Bank fraud. If convicted, he faces up to 30 years in prison and a maximum $1 million fine.

Last Call To Book Rooms & Sponsor deBanked CONNECT San Diego

September 21, 2019deBanked CONNECT San Diego, which kicks off on October 24th at the Hard Rock Hotel, is fast approaching. Discounted hotel rooms through deBanked’s special link will only remain available until Monday at 5pm. Even if you were planning to book later and pay full price, the hotel has informed us that they are almost entirely sold out of rooms.

Monday is also the last day to become a sponsor of the event. Don’t miss out on this incredible west coast opportunity and call 917-722-0808 or email events@debanked.com to register.

Tickets to the event can be purchased HERE. Commercial finance brokers benefit from a reduced entry fee.

class=”aligncenter size-large wp-image-182322″ />

class=”aligncenter size-large wp-image-182322″ />