Articles by deBanked Staff

Bitty Continuing to Perform Well in Q2 2025

August 11, 2025“Our investment in Bitty continued to perform well in the 2025,” said Todd Schwartz, CEO of OppFi, during the Q2 earnings call. “The business continues to add accretive profitability and cash flow to OppFi. Bitty is doing a great job utilizing technology to improve operations and the customer experience, identifying additional growth opportunities in new credit segments and capitalizing on the continued supply/demand imbalance in the small business lending space.”

OppFi holds a 35% stake in Bitty. Their pro-rata share of Bitty’s first half 2025 earnings was significant to their bottom-line.

NerdWallet: ‘AI Answers Are Taking Organic Search Clicks Away’

August 11, 2025NerdWallet, which operates one of the largest online small business lending marketplaces in the US, is experiencing the competitive pressures of AI in real-time. For example, the company has long depended on organic search traffic to generate customers, but Google’s search results now serve more than just links.

“I’d say the story hasn’t changed much since last quarter. Organic search is still pretty challenged,” said NerdWallet CEO Tim Chen during the Q2 earnings call. “What’s happened incrementally is we’ve seen AI-overviews roll out to a much broader swath of queries in recent months, which is resulting in more people getting answers without ever clicking through to websites.”

The company revealed that SMB products revenue of $25 million was down 4% year-over-year, “primarily due to pressures in organic search traffic.”

NerdWallet, however, has also noticed early signs that LLMs are generating referrals for them.

“What’s probably less obvious is that people who click through from LLMs have materially higher intent to transact than people who click through from search engines,” Chen said. “So, while encouraging in terms of that being a new growth channel, it’s still pretty small.”

Square Loans Originates $1.64B in Small Business Loans in Q2

August 8, 2025Block’s merchant financing division, Square Loans, continues to lead the competition. The company originated $1.64B in small business loans in Q2, up slightly from $1.59B in Q1. That puts them on pace for $6.5B for the year and allow them to maintain their top position among small business finance companies that deBanked tracks. Square Loans’ advantage is that its customers repay their loans automatically through their daily Square POS transactions.

Overall, Block CEO Jack Dorsey announced that the entire company is “Back on offense.”

“We had a strong second quarter,” wrote Dorsey in his shareholder letter. “Square GPV grew 10% year over year and Cash App gross profit grew 16% year over year, accelerating as we exited Q2.”

Shopify Capital: Business Loan & MCA Originations Grow, Loss Rates Consistent

August 6, 2025Shopify Capital purchased $1B worth of business loans and MCAs in Q2, bringing the total to $1.8B for the first half of 2025.

“Our capital business continues to grow, supported by recent product innovations that enhanced our suite of credit offerings and expanded our geographic reach, including launching Capital in Germany and the Netherlands,” said Shopify CFO Jeff J. Hoffmeister. “We’ve introduced new tools that give merchants more choice in how they manage and select loan options, providing greater flexibility to meet their financing needs. Note that loss rates have remained consistent with prior quarters. This is about the successful, thoughtful expansion of capital.”

The company is on pace to outperform last year’s estimated originations of $3B. The company held ~$1.6B in business loans and MCAs on its balance sheet as of June 30.

Certain loans and merchant cash advances are facilitated by Shopify and originated by a bank partner, from whom Shopify then purchases the loans and merchant cash advances obtaining all rights, title and interest or discount. deBanked is able to estimate originations from these figures.

LightSpeed Capital Has Over $100M in MCAs on Balance Sheet

August 5, 2025LightSpeed Capital, the MCA division of LightSpeed Commerce, has over $100M in merchant cash advances on its balance sheet, according to the company’s latest quarterly earnings report. The POS company reported that LightSpeed Capital’s revenue grew 34% year-over-year.

The company’s balance-sheet-driven approach has made them relatively conservative and cautious with originations growth. For example, in the preceding quarter, Lightspeed CFO Asha Bakshani said “There is a lot of opportunity. We can move faster if we wanted to. When we look at our peers, for example, they are giving out 1% of their [Gross Transaction Volume] in merchant cash advance. Lightspeed is well below that. 1% of our GTV would be almost $1 billion in merchant cash advance. So when we think about the opportunity, it’s there. It’s just that in this macro, we want to move carefully on a product like Capital. Like I mentioned earlier, our default rates are in the very low single digits, and we want to keep it there.”

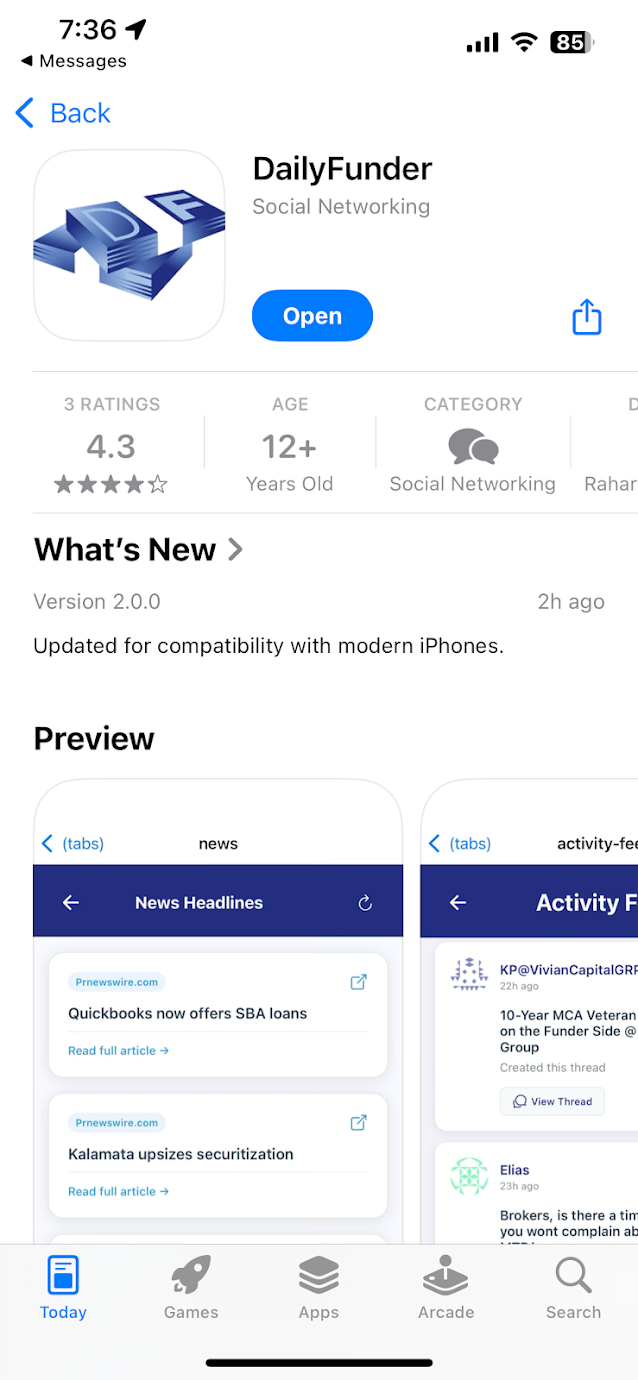

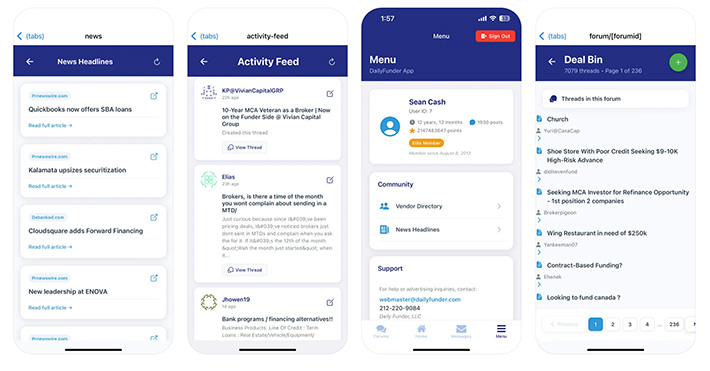

DailyFunder’s Mobile App Returns to iOS

August 4, 2025 DailyFunder’s iOS app is back. DailyFunder 2.0 is now available in the Apple App Store.

DailyFunder’s iOS app is back. DailyFunder 2.0 is now available in the Apple App Store.

The app is a completely new rebuild from the versions that were published in the App Store in 2013 & 2014. Apple’s technical standards forced those versions out of distribution by 2017 and there had been no replacement since. That is until now since DailyFunder recently decided to do a reboot using in-house developers instead of a third party. Given that it’s the first new iteration, consider it a Beta.

DailyFunder 2.0 features:

- The main forum categories

- The Activity Feed

- Make new threads and replies

- PM other users

- Industry news headlines & links

- Advertiser/Vendor directory

- Advertising

What’s not available yet:

- The app for Android (on the list to do)

- The reputation feature

- In-app registration (must do that on the web-based version)

- Perfection (there will be bugs. Please bear with it)

- Ability to edit one’s profile in-app (on the list to do)

DailyFunder has more than 17,000 approved members, making it the largest and most active online small business finance community in the US. The site launched as a forum in 2012. DailyFunder is great for networking, placing a deal, or industry gossip. For questions related to the site or the mobile app, email webmaster@dailyfunder.com.

LendingTree: ‘Small Business Loan Originations Up 40% On Our Platform’

August 1, 2025LendingTree’s small business loan origination volume is up 40% YoY, according to the company’s latest quarterly earnings report.

“In small business, we made a strategic investment to grow our sales force and it has paid off in more business and more efficiency,” said LendingTree CEO Doug Lebda. “I think that small business can be a real growth driver for us.”

Lebda added that profitability had been consistently growing each quarter and that the company was “on a roll.” And part of that is being attributed to staying on top of AI.

“Eighteen months ago, I told our board and our company that we’re going to be an AI first company,” Lebda said. “And today, effectively, all of our employees are using AI in their day jobs, including having enterprise GPT for everyone.”

How SoFi is Approaching AI and Blockchain

July 30, 2025“We’re implementing and testing AI applications across our business from enhancing back office processes like dispute resolution and filing suspicious activity reports to improving how we interact with our members to help them get their money right, and we brought on teams of engineers to drive these efforts forward,” said SoFi CEO Anthony Noto during the Q2 earnings call.

While the company is using other innovative technologies like blockchain to allow customers to move money over crypto rails or to invest in the underlying cryptocurrencies themselves, they also see a role for it to effectively reintroduce peer-to-peer lending/investing.

“As we look further down the road, we see the potential to tokenize SoFi loans to make them more widely available in liquid markets in increments of dollars rather than tens of thousands of dollars such that anyone can invest in loans just like they do equities,” Noto said. “Crypto is a key area of focus for our management team and when we have brought on board significant expertise, including substantial engineering talent to advance these new initiatives.”