|

Phone: 844-200-1944 Email: info@rok.biz Learn More |

Since: February 2021 Since: February 2021 | |

Registered sales-based financing provider in VA Registered sales-based financing provider in VA |

|

Related Headlines

| 12/09/2022 | ROK Financial announces new CEO |

| 05/13/2021 | Video: deBanked went to ROK Financial |

Related Videos

Tony Cimino of ROK Financial | On The Scene At ROK Financial |

Sidebar Chat With James Webster - ROK Financial | |

Stories

ROK Financial Announces Cannabis Banking Partnership with BNB Bank

January 14, 2021Great River, NY: ROK Financial, a leader in the alternative and commercial lending space is excited to announce their newest partnership with BNB Bank’s Cannabis division. This new partnership allows for ROK Financial to offer direct checking and savings to Cannabis businesses through BNB Bank.

“This new partnership is truly filling a void within the Cannabis industry” says James Webster, CEO of ROK Financial “Federal regulations make it near to impossible for Cannabis related businesses to utilize traditional banking methods. We’re proud to partner with a financial institution that sees the value and need within the industry.”

BNB Bank, headquartered in Bridgehampton, NY has 39 locations from Manhattan to Montauk. BNB Bank provides the resources of a strong financial institution, exceptional customer service, and access to a suite of leading-edge money management tools. They are publicly traded on Nasdaq (BDGE) and have a 5-star rating (Bauer Financial). Peter Su, Vice President – Private Banking BNB says: “This new relationship with ROK Financial allows us to service a wider variety of clientele. We’re excited to work with ROK Financials existing Cannabis clients as well as attracting new relationships through this partnership.”

A large majority of traditional institutions tend to shy away to offering traditional banking to the industry as a whole due to the lack of regulations and financial risk they may face. Banks also risk losing their master account with the Federal Reserve due to the ‘risk’ of the industry. “BNB Bank has a board approved Cannabis Banking Policy that we strictly abide to, and have established a compliance monitoring program providing seed to sale regulatory support to ensure we all are in compliance” says Su “We are happy to help provide needed resources to these thriving businesses.”

About ROK Financial

ROK Financial’s team committed to establishing ROK solid relationships with our clients, lenders, and partners. By providing the best financing solutions available to business owners while creating a positive association with business financing. Through our streamlined process, revolutionary technology and educated team of experts, we support business owner’s ability to create new opportunities. ROK Financial is proud to empower the heartbeat of our country, our small businesses.

Megan Capobianco

3500 Sunrise Highway

Building 100, Suite 201

Great River, NY 11739

833-337-6534

press@rok.biz

www.rok.biz

ROK Financial Announces Direct SBA Loan Access

November 23, 2020![]() Over the past several months the state of the economy has been by no doubt uncertain. With unemployment hitting record highs and Coronavirus cases still on the rise, business owners all across the country have been faced with many difficult decisions regarding their livelihood.

Over the past several months the state of the economy has been by no doubt uncertain. With unemployment hitting record highs and Coronavirus cases still on the rise, business owners all across the country have been faced with many difficult decisions regarding their livelihood.

Finding business financing options during these uncertain times can be challenging and risky to not only business owners, but the banks and lenders they choose to work with.

ROK Financial truly understands the uncertainty a business owner feels during these current times. Having derived themselves from a company split back in August, the team is helping other business owners just like them navigate these unchartered waters.

“We have been working tirelessly with our lenders and partners over the past several months discussing different ways we can continue to better service our clients.” Says CRO, Patrick Manning of ROK Financial “The relationships we have built over the years allows us to become quite versatile with our product offering, in turn allowing us to better serve our business owners. That is why we are extremely excited to announce our exclusive partnership with Doug Hood, SBA Loan Consultant LLC. This unique partnership opens up direct SBA access to clients for SBA products $350,000 and above.”

Doug Hood has been facilitating SBA Loans for more than 35 years, resulting in more than $20 million in SBA Loans distributed to business owners annually. Hood said he connected with ROK via LinkedIn, “I’m on Linkedin way more than I should be, we connected at 10 or 11 o’clock at night, and we hit it off.” Says Hood. Excited at the fact that ROK offers short term financing that Doug himself would now be able to leverage in addition to his SBA Loan offerings for his clients was a win-win.

Doug now sits as the official SBA Loan Consultant under the ROK Financial umbrella for deals $350,000 and above. This unique relationship provides greater opportunities for business owners from purchasing existing businesses, refinancing existing debt, starting a business and much more.

“The worlds of Fintech and SBA have collided for the greater good” says Manning, “streamlining and modernizing a once antiquated process, which eliminates the frustration that comes along with long-term lending.”

—————

Megan Capobianco

press@rokfi.com www.rokfi.com

3500 Sunrise Highway

Building 100, Suite 201

Great River, NY 11739

833-337-6534

Britecap Financial Welcomes Jim Noel as Vice President of Strategic Partnerships

October 2, 2024BriteCap Financial LLC (“BriteCap”), a leading non-bank lender providing small businesses with fast, convenient financing alternatives such as working capital loans, announced today the appointment of James Noel as Vice President of Strategic Partnerships. Jim brings over 20 years of experience in the business lending industry to BriteCap, where he will play a pivotal role in expanding the company’s network of strategic funding partners.

“Jim and I have built a strong working relationship over the years, and I’m thrilled to bring his expertise to BriteCap,” said Richard Henderson, CEO of BriteCap Financial. “His addition will help us expand our exclusive network of elite funding partners while delivering the white-glove service they’ve come to expect. Jim’s depth of experience in business lending will elevate the personalized care we provide as we continue to expand our reach.”

In his new role, Noel will be responsible for identifying and cultivating strategic partnerships with brokers, alternative lenders, and other financial services providers. He will also work closely with BriteCap’s existing partners to enhance collaboration and drive mutual growth.

“I am thrilled to join the BriteCap team,” said Noel. “I look forward to working with an exceptional team to help the company expand our strategic partner network while continuing to deliver a high level of service.”

Noel’s appointment comes at an exciting time for BriteCap Financial, as the company continues to grow and expand its offerings to small businesses across the country.

About BriteCap Financial

BriteCap Financial is a leading provider of working capital for America’s small business owners. Since 2003, BriteCap combines technology, non-traditional credit algorithms to provide fast, convenient and affordable working capital direct to businesses or through their broker network. For more information about becoming a partner, visit britecap.com/become-a-partner.

Media Contacts:

For BriteCap:

David Schneider

Vice President of Marketing

BriteCap Financial, www.BriteCap.com

david.schneider@britecap.com

BriteCap Financial Announces New CEO

September 16, 2024BriteCap Financial LLC (“BriteCap”), a leading non-bank lender providing small businesses with fast, convenient financing alternatives such as working capital loans, announced today the appointment of Richard Henderson as the company’s new CEO.

“I’m proud to see Rick take the helm at a time when BriteCap is poised to bring financial solutions to the market at scale,” said outgoing CEO Sri Kaza. “His experience and relationships across the industry will open the door for many more small businesses.”

BriteCap became a member of the growing family of companies under the North Mill Equipment Finance (NMEF) umbrella in 2023. “We are thrilled to have Rick join as the leader of BriteCap,” reported David C. Lee, Chairman and CEO, NMEF. “His two plus decades of success in equipment finance and working capital lending dovetail well with our strategy to offer comprehensive capital solutions for small and medium sized businesses. In particular, we look forward to developing unique solutions and programs for our key referral partners in partnership with BriteCap.”

“I’m excited to join BriteCap and lead such a respected, values-driven company,” said Rick Henderson, CEO, BriteCap Financial. “BriteCap has built an exceptional, tech-enabled funding platform that blends the speed and convenience of self-service with the expertise of a supportive team, making it easier and faster for small and medium-sized businesses to access the capital they need to grow. I look forward to collaborating with the BriteCap team and our strategic referral partners to build on this legacy, developing innovative solutions that empower America’s business owners and the finance brokers who support them.”

BriteCap operates from offices in North Hollywood, CA and Las Vegas, NV.

About BriteCap Financial

BriteCap Financial is a leading provider of working capital for America’s small business owners. Since 2003, BriteCap combines technology, non-traditional credit algorithms to provide fast, convenient and affordable working capital direct to businesses or through their broker network. For more information about becoming a partner, visit britecap.com/become-a-partner.

About North Mill Equipment Finance

NMEF originates and services small to mid-ticket equipment leases and loans, ranging from $15,000 to $2,500,000 in value. A broker-centric private lender, the company accepts A – C credit qualities and finances transactions for many asset categories including construction, transportation, vocational, medical, manufacturing, printing, franchise, renovation, janitorial and material handling equipment. NMEF is majority owned by an affiliate of InterVest Capital Partners. The company’s headquarters are in Norwalk, CT, with regional offices in Irvine, CA, and Voorhees NJ.

Media Contacts:

For BriteCap:

David Schneider

Vice President of Marketing

BriteCap Financial, www.BriteCap.com

david.schneider@britecap.com

954-494-1606

For NMEF:

Don Cosenza

Chief Marketing Officer

NMEF, www.nmef.com

dcosenza@nmef.com

203-354-1710

Capify Announces New Appointment to Lead Broker Division

March 7, 2024Leading online SME lender, Capify, has appointed Mike Morris to lead its broker business in the UK.

Mike joins Capify after five years with Funding Circle, most recently as Head of Business Development, where he was responsible for leading the lender’s broker network.

With nearly 20 years experience in the finance industry, including time at Close Brothers retail finance, Mike will focus on the growth and expansion of Capify’s introducer relationships and its marketplace offering.

“I’m hugely excited to join Capify to build out its broker programme and exponentially grow this channel for one of the first online SME lenders in the UK market,” said Mike.

“Capify occupies a vital place in the funding landscape – offering much-needed fast, flexible and responsible solutions for businesses. We’re focused on ensuring that introducers understand our offering and how we can help their clients. Our growth will then be realised by launching new products that go up and down the credit spectrum, providing the best possible service to enable the brokers, and ultimately the clients they represent, to get the funds they need to thrive in the current climate. Our goal is to have an offering for all types of businesses so we can be a one-stop shop for brokers and their clients. I look forward to Capify announcing these new offerings in the near future.”

Capify was launched in the UK in 2008, against the backdrop of the global financial crisis, when many small and medium-sized businesses were struggling to access funding from banks. Last year it was named the UK Credit Awards SME Lender of the Year (up to £1m). The company was founded initially in the United States in 2002 making it one of the world’s first online alternative financing companies for SMEs globally.

John Rozenbroek, COO/CFO at Capify, said: “We’re absolutely delighted to welcome Mike to the Capify team. Brokers play an integral role in helping businesses understand the complex funding landscape and the types of finance that are best suited to their needs. His appointment underlines our commitment to introducers and marks an exciting new stage in Capify’s continued growth.”

ABOUT CAPIFY

Capify is an online lender that provides flexible financing solutions to SMEs seeking working capital to sustain or grow their business. Alongside its sister company, Capify Australia, the fintech businesses have been serving their respective markets for over 15 years. In that time, it has provided finance to thousands of businesses, ensuring the UK’s vibrant and vital SME community can meet the challenges of today and the opportunities of tomorrow.

For more details about Capify, visit: http://www.capify.co.uk

Capify Contact:

Ash Yazdani, Marketing Director

ayazdani@capify.co.uk

Media enquiries

Sam Gallagher, Director

sam.gallagher@1473media.com

Broker Battle Finds a Champion

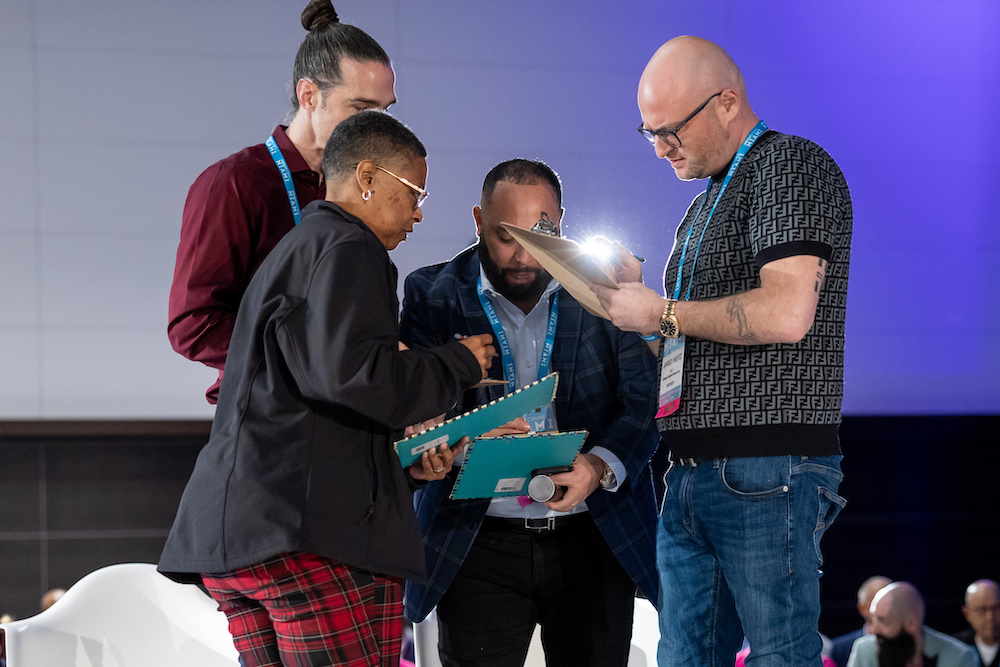

January 14, 2024At the Miami Beach Convention Center in Miami Beach, Florida, thousands of viewers packed a hall to witness the first ever Broker Battle™ at deBanked CONNECT. After the rules of the competition were explained, six broker contestants waited eagerly for their turn to face four judges and with that a chance to win a grand prize of $5,000. Their goal? Choose from one of three pre-defined sales scenarios and show off their knowledge and abilities to the judges. Here’s what happened:

The Broker Battle was introduced

Broker Battle judge Daniel Dames (Bitty Advance) held up a Title belt

Irving Betesh (Advance Funds Network) had the distinction of going first. He came prepared!

The contestants continued one by one alphabetically by last name

The conversational role playing on the stage covered the gamut, ranging from explaining APRs and contract terminology to diagnosing customer needs or trying to earn a customer’s business. Below, judges Jared Weitz (United Capital Source) and Cheryl Tibbs (Equipment LeaseCo Inc) listen in to a contestant’s pitch.

Mike Brooks (Best Connect Capital) came in with his own style

Corey Digi (Lexington Capital Group) put up a strong showing

Stanley Mitchell (CLM Financial) goes to work

Danielle Rivelli (United Capital Source) showed off her experience

Anthony Truglia (CapFront) made it known the competition wasn’t over yet

The judges had to add up their scores for each contestant to find out which TWO would make it into the final championship battle

Second from the right is judge Leo Vargas (Triton Recovery Group).

Anthony Truglia and Danielle Rivelli are declared the two finalists after racking up the highest scores

The final sales scenario is revealed!

Both contestants have to compete on stage at the same time! Oh my!

The contestants are sent offstage so the judges can deliberate

And the winner is…

Anthony Truglia!

All photos from the Broker Battle here

All photos from the rest of deBanked CONNECT MIAMI here

deBanked would like to thank all of the amazing broker contestants for participating in something bold and brand new. Thank you to Anthony Truglia, Danielle Rivelli, Corey Digi, Irving Betesh, Stanley Mitchell, and Mike Brooks. Gratitude is also directed towards the judges for their efforts, Cheryl Tibbs, Daniel Dames, Jared Weitz, and Leo Vargas.

deBanked hopes that this competition inspires all brokers to become better, to further master their knowledge of available products, legal compliance, style, and confidence. A video highlight reel of the competition is in post-production.

Interested in more from deBanked? Contact us at info@debanked.com or call 212-220-9084.

NMEF Offers to Purchase IOU Financial

July 25, 2023JULY 25, 2023, NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”), a leading independent commercial equipment lender located in Norwalk, Connecticut, announced today that the following letter was sent yesterday to the Special Committee of the Board of Directors of IOU Financial Inc. (“IOU”). NMEF’s proposed acquisition is at a 27% premium to the price per share agreed to by IOU and a group of inside shareholders representing 46.1% of the issued and outstanding shares of IOU announced on July 14, 2023. “We are offering to all IOU shareholders a far superior price to the value of the Company presented by the inside shareholders that was accepted by the Special Committee in a sweetheart deal for those insiders,” said David C. Lee, Chairman and CEO of NMEF. “Our offer is not subject to any financing contingency nor access to confidential information.”

About NMEF

NMEF originates and services small to mid-ticket equipment leases and loans, ranging from $15,000 to $2,000,000 in value. A broker-centric private lender, the company accepts A – C credit qualities and finances transactions for many asset categories including construction, transportation, vocational, medical, manufacturing, printing, franchise, renovation, janitorial and material handling equipment. NMEF is majority owned by an affiliate of InterVest Capital Partners. The company’s headquarters is in Norwalk, CT, with regional offices in Irvine, CA, Dover, NH, Voorhees NJ, and Murray, UT. For more information, visit www.nmef.com. One of NMEF’s controlled affiliates, BriteCap Financial LLC, is a leading non- bank lender providing small businesses with fast, convenient financing alternatives such as working capital loans since 2003 from offices in North Hollywood, CA and Las Vegas, NV. For more information, visit www.britecap.com.

Welcome to Broker Fair 2023

May 8, 2023 Broker Fair check-in and breakfast start at 8am at the Hilton Midtown in NYC.

Broker Fair check-in and breakfast start at 8am at the Hilton Midtown in NYC.

If you’re here today, here’s some quick helpful info:

WIFI PW: ROKFinancial

Contact info: events@debanked.com

We hope you enjoy the day!

Loan Broker-Remote Sales... rok financial is looking for sales representatives nationwide to join our team. work remotely as an independent contractor, aggressive commission stru... |

Rok Financial is a new site sponsor... please welcome rok financial as a new site sponsor. to learn more, visit: :cool::):cool:... |