Archive for 2017

Upstart Raises $32.5M

March 6, 2017It’s been three years since we launched the Upstart lending platform, and today we’re pleased to announce we’ve raised $32.5M to take our business to the next level. The funding round was lead by Rakuten, a global leader in internet services and global innovation headquartered in Japan, and by a large US based asset manager. Existing investors Third Point Ventures, Khosla Ventures, and First Round Capital also participated. We’re particularly excited to have Oskar Mielczarek de la Miel, Oskar Miel, Managing Partner of the Rakuten FinTech Fund join Upstart’s Board of Directors.

With more than 50,000 loans originated, Upstart has the highest consumer ratings in the industry, has Net Promoter Scores (NPS) in excess of 80, and has delivered industry-leading returns to loan investors.

Leaders in Technology and Data Science for Lending

Upstart was the first platform to leverage modern data science and technology to power credit decisions, automate verification, and deliver a superior borrower experience. In 2014, we were first to launch next-day funding. In the last year, we virtually eliminated loan stacking on the Upstart platform, a central cause of credit issues in online lending. Today, more than 20% of our loans are fully automated, helping us attract the best quality borrowers with a superior experience.

As a result of our efforts, we’ve seen unparalleled credit performance, with 2016 cohorts our strongest yet. Upstart loans are funded in four distinct ways: 1) whole loan sales to institutions, 2) retention by Upstart’s originating bank partner, 3) sales to Upstart itself, and 4) via individuals in our fractional market. Furthermore, we expect our first loan securitization transaction within a few months.

2017 and Beyond!

We’ve focused considerable effort on our credit quality and loan economics, and the results speak for themselves. We aim to originate more than $1B in loans in 2017, and expect to reach cash flow profitability this year.

But that’s not all. We’re also thrilled to announce that Sanjay Datta has joined Upstart as CFO. Sanjay was formerly VP of Global Advertising Finance at Google, having spent a decade to help build and internationally expand Google’s $80B core economic engine.

Those that know my history at Google will understand why I’m excited to tell you about “Powered by Upstart”, a Software-as-a Service offering derived from Upstart’s top-rated consumer lending platform. From rate requests through servicing and collections, this new service brings modern technology and data science to the entire lending lifecycle.

Our beginnings

Anna, Paul, and I founded Upstart to bring the best of Google to consumer lending. Upstart was the first platform to leverage modern data science and technology to power credit decisions, automate verification, and deliver a superior borrower experience. In 2014, we were first to launch next-day funding. As of today, more than 20% of our loans are fully automated and we expect this percentage to increase significantly through 2017. With more than 50,000 Upstart loans originated, we have the highest consumer ratings in the industry and have delivered industry-leading returns to loan investors. With Net Promoter Scores (NPS) in excess of 80, we’re excited about the impact we’re having.

Technology partner

FinTech is disrupting all areas of financial services. As a leading tech platform in marketplace lending, Upstart aims to partner with financial institutions rather than compete with them. Given the pace of change in lending, technology partnerships will be critical in the years to come, and Upstart aims to be a partner the industry can rely on.

But “Powered by Upstart” is not just software – it’s a turnkey solution that provides all necessary document review, verification phone calls, fraud analysis, and (optionally) customer service, loan servicing and collections.

Software-as-a-Service in lending

SaaS has grown exponentially in the last decade because of its obvious virtues: rather than buying, installing, configuring, hosting, and supporting software yourself, the software is delivered over the cloud. It’s more reliable and always up to date. Delivering cloud software can be challenging in any industry. Usability, reliability, and performance are the minimum to play, and effective change management is critical to success. As the team that delivered Google’s SaaS platform before it was called “cloud”, we understand these challenges.

Of course, the regulatory environment in lending raises the bar even higher. We’ve long demonstrated our commitment to trustful and compliant lending, and we’re likewise committed to delivering robust and compliant lending software.

Patch of Land Hires Chief Investment Product Officer, Matthew Zall, Recognized Capital Markets Expert and Innovator of Lending Products for the Single-Family Home Rental Market

March 5, 2017LOS ANGELES- March 6, 2017 – Patch of Land, a leading online real estate marketplace lender and crowdfunding platform, announces the addition of Matthew Zall as Chief Investment Product Officer as the firm prepares to expand into the single-family rental market with longer term, permanent financing products. The number of non-owner occupied single-family properties in the U.S. including townhomes, condos, and 2-4 unit properties grew to almost 24 million units valued at over $6 trillion in 2016, according to ATTOM Data Solutions.

Zall brings to Patch of Land more than 12 years of real estate and mortgage experience, as well as expertise in financing and product development. He pioneered three of the industry’s first-ever multi-borrower single-family rental securitizations, helping to build Blackstone Group subsidiary, B2R Finance, (now known as Finance of America Holdings, LLC) from start up to a multibillion dollar lender in only a few years. Prior to joining B2R, Matt was a Commercial Real Estate (CRE) trader at J.P. Morgan and Bear Stearns. At Patch of Land, Zall will execute strategies to enable the expansion of the firm’s position as a marketplace lender by offering both accredited and institutional investors additional opportunities to invest in this asset class.

“Patch of Land’s marketplace is designed to meet the lending needs of real estate investors. The addition of Matt enables us to continue the expansion of our marketplace to fully serve the lending needs of more than 10 million Americans who directly invest in single-family residential properties and need consistent, reliable access to capital to fuel their businesses,” said Paul Deitch, Patch of Land’s Chief Executive Officer. “We are excited about adding Matt to our executive team as he is passionate about our mission to leverage technology to improve the borrowing experience for the real estate entrepreneur and at the same time offer investors from both Main Street and Wall Street the opportunity to participate in this attractive asset class.”

About Patch of Land

Since issuing its first real estate loan in October 2013, Patch of Land has been recognized in the financial technology space as a leader in online real estate lending. The company employs its proprietary technology to efficiently fill a void in the real estate finance industry by providing borrowers access to capital for residential and commercial real estate projects. The platform also establishes a marketplace through which qualified individual and institutional investors can participate in private real estate projects with low minimum investments, predictable returns and first-lien secured loans.

More information is available at www.PatchofLand.com or by calling 888-959-1465.

Media Contact: Glen Orr

glenlorr@gmail.com

469.441.3203

Innovative Lending Platform Association and Coalition for Responsible Business Finance Join Forces

March 5, 2017NEW YORK, Early Release — The Innovative Lending Platform Association (ILPA) and the Coalition for Responsible Business Finance (CRBF) today announced they are joining forces and will now operate as the ILPA – the leading trade organization representing a diverse group of online lending and service companies serving small businesses. Joining ILPA’s existing members, OnDeck® (NYSE: ONDK), Kabbage® and CAN Capital, are CRBF member companies Breakout Capital, Enova International’s (NYSE: ENVA) The Business Backer™, PayNet and Orion First Financial. United by a shared commitment to the health and success of small businesses in America, the newly expanded ILPA is dedicated to advancing best practices and standards that support responsible innovation and access to capital for small businesses.

In addition, leading national small business organizations that formerly served as the CRBF Advisory Board will now represent small business customers as formal advisors to the ILPA. The Advisory Board includes individuals from the National Federation of Independent Business (NFIB), the National Small Business Association (NSBA), the Small Business & Entrepreneurship Council (SBE Council), the U.S. Chamber of Commerce, and new representatives from the Association for Enterprise Opportunity (AEO). These small business organizations have provided key input into the collective group’s best practices and standards initiatives over the past year, ensuring that the needs of their small business constituents are addressed.

The expanded ILPA remains committed to advancing online small business lending education, advocacy and best practices. In October, the ILPA introduced the SMART Box™ (Straightforward Metrics Around Rate and Total cost), a first-of-its-kind model pricing disclosure and comparison tool launched in partnership with the AEO. The SMART Box is focused on empowering small businesses to better assess and compare finance options and is now available for broader adoption by lending platforms. More details can be found at: http://innovativelending.org/smart-box/

As a leading voice for responsible business funding, CRBF launched in January 2016 with the mission to create a concrete code of ethics for the industry and to educate policymakers on the value of non-bank small business financing. The organization outlined responsible and transparent business practices for both providers as well as customers, and the expanded ILPA has leveraged that work to formulate an updated industry Code of Ethics that will guide the ILPA moving forward.

The expansion of the ILPA follows a period of broad stakeholder engagement and a demonstrated shared commitment to serving small businesses. With this unification, the cross-industry effort to bring innovative and responsible solutions to improve access to capital for Main Street small businesses continues to gain momentum.

“Fostering responsible innovation and empowering small businesses to better assess and compare finance options are priorities for the ILPA. We are delighted to join forces with the CRBF as we work together to advance small business online lending education, advocacy and best practices,” said Noah Breslow, Chief Executive Officer, OnDeck. “We are proud to be part of this growing cross-sector effort to help improve capital access on behalf of small businesses across the United States.”

“The combination of these leading organizations represents a landmark moment in the industry, signifying how major players in the small business lending space are increasingly aligned on values and best practices that benefit small businesses,” said Carl Fairbank, founder and chief executive officer, Breakout Capital. “Founded on the fundamental principles of responsible lending, education and transparency, Breakout Capital is thrilled to partner with other premier players in the industry who share our vision and believe that a unified industry voice can promote small business success more effectively. “As a founding member company of CRBF, The Business Backer is thrilled with the merger between the CRBF and the ILPA,” said Jim Salters, president of The Business Backer and CRBF Advisory Board member. “The move creates an even larger platform of industry leaders with a common voice to help ensure small businesses have access to honest and transparent funding sources.”

“The ILPA was launched as a self-regulatory exercise and is focused on empowering small businesses with clear and transparent ways to compare financing options,” said Rob Frohwein, co-founder and chief executive officer of Kabbage. “Kabbage and the ILPA are excited to join with the CRBF in order to advance ubiquitous industry standards. Together, we are eager to continue working with regulators and policymakers to expand small businesses’ ability to easily access technology-driven financing products.”

“Access to capital is a high priority for America’s small businesses. As our economy grows, small business owners need diverse sources of capital to hire new employees and expand their businesses. The U.S. Chamber of Commerce applauds the innovative capital providers in the ILPA for their dedication to fueling growth on Main Street,” said Tom Sullivan, vice president, small business, U.S. Chamber of Commerce.

“CAN Capital has been a supporter of transparency throughout our 19 year history, and we are excited to see the ILPA expand as it continues to support small business owners,” said Parris Sanz, chief executive officer of CAN Capital.

“Small business lending continues to be stubbornly elusive for many small firms and what we need is not just more lending, but better lending options,” said Todd McCracken, National Small Business Association president and chief executive officer. “This merger will expand on efforts to connect small business with a variety of fair and responsible lending resources.”

“We are excited to be part of an organization whose purpose is to create a vibrant, healthy, small business lending marketplace that serves the engine of the U.S. economy – small businesses,” said David Schaefer, chief executive officer of Orion First Financial. “As a loan servicer to small business lenders, we are particularly enthusiastic that the ILPA is embracing a diverse membership and participation from small business associations through its Advisory Board.”

“SBE Council looks forward to partnering with the expanded ILPA to continue advocating for the innovative and responsible sources of funding to which entrepreneurs and small businesses need access,” said Karen Kerrigan, president and chief executive officer of the Small Business & Entrepreneurship Council.

“It is critical that these and other responsible lenders come together to advance initiatives like SMART Box,” said Connie Evans, president/chief executive officer of the Association for Enterprise Opportunity. “The time is ripe for united voices and action to give more people the opportunity and the tools to realize a brighter future for their businesses.”

Together, the members of the expanded ILPA have provided access to more than $14 billion dollars in capital to small businesses to help drive growth and hiring.

With Clock Ticking, Members of the Commercial Finance Coalition Journeyed to the New York State Capitol

March 5, 2017 With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

With less than a month to go until New York State’s budget deadline, members of the Commercial Finance Coalition (CFC) traveled to Albany, NY last week to address a vague and confusing licensure proposal put forth by Governor Cuomo. According to the CFC, nobody from the New York Department of Financial Services, the governor’s office or the state legislature had contacted any of their members prior to putting the language in the budget that they suspect could lead to catastrophic consequences. So on very short notice, they packed their bags and went up to Albany to tell their story to as many legislators as they could.

“It could destroy the industry if the worst comes to fruition,” declared Robert Cook, a partner at Hudson Cook LLP, who was speaking in reference to the proposal. The industry not only employs thousands of people in New York State but also provides much-needed capital to small businesses there. The CFC says that their members injected more than $50 million into New York businesses just last year alone.

Several law firms who have written about the proposal have used words like could, may and likely to explain what will happen, in part because it seems as though no one’s really sure. CFC members worry that the proper research hasn’t been done, especially when there hasn’t been any engagement with them. “They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director.

As the clock ticked down, the CFC’s two-day effort in the capitol building played out like a scene from a movie.

Are you aware of Part EE of the TED Bill?

This is what we do…

No, nobody from the Department of Financial Services has even talked to us

No, we’re not kidding

And on it went…

Gans says the CFC is looking for additional companies in the small business financing industry to support their efforts. He’ll be at the LendIt Conference. “I would be happy to meet with anyone interested in joining the CFC and helping us fight this misguided policy that is also attending,” he said. He can be contacted at dgans@polariswdc.com.

The budget deadline in New York State is March 31st.

Letter From the Editor – Jan/Feb 2017

March 4, 2017When deBanked first launched online in 2010, I thought it was too late, that perhaps all the exciting changes in alternative finance had already taken place and that aside from a few obsessed geeks, there wasn’t that big of an audience to write for. It certainly felt a bit out-of-style, especially since I had been working in the industry for more than four years by that point. The only publication that was dedicated to the scene at the time had already come in to the public eye and vanished. Many alternative financial companies had met the same fate, thanks to the financial crisis.

In a way, deBanked started off as a post-apocalyptic diary, an accounting of the industry’s survivors and their roles in the new world order. Primitive, my reporting may have been then, but interest quickly grew. By mid-2011, I was already forced to change web hosts to keep the website from slowing down. In my day job as a commercial finance broker, I continued to talk to small business owners all the over the country about a common theme, that banks just weren’t lending. And maybe they never would again, some predicted anyway. Or maybe the way loans were made in general would just never be the same.

Looking back among my old 2011 stories, I discovered that I had written a personalized review of Square’s payment technology and had given it high marks. Back then however, I saw Square as a payments toy. It was innovative and sexy, but unrelated to lending. Fast-forward to 2016 and Square’s capabilities have expanded. I should know, they funded my business exactly five years after my review. In this issue, I’ll walk you through what it was like to play the role of borrower, and put marketplace lending up to the ultimate test. Thanks to Square Capital, my journey has come full circle or more appropriately, full square.

This issue is the first of 2017. For alternative finance, it fortuitously feels like the beginning, not the end. If our descendants far in the future stumble upon these stories, I pray they will enjoy our accounts of the transformation, when entrepreneurs dared to look at the world in front of them and boldly decided to change it. It was the early 21st century, historians will say, when mankind dared to de-bank and change everything we knew about finance. In the here and now, you are a part of it all…

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced deBanked’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, deBanked is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

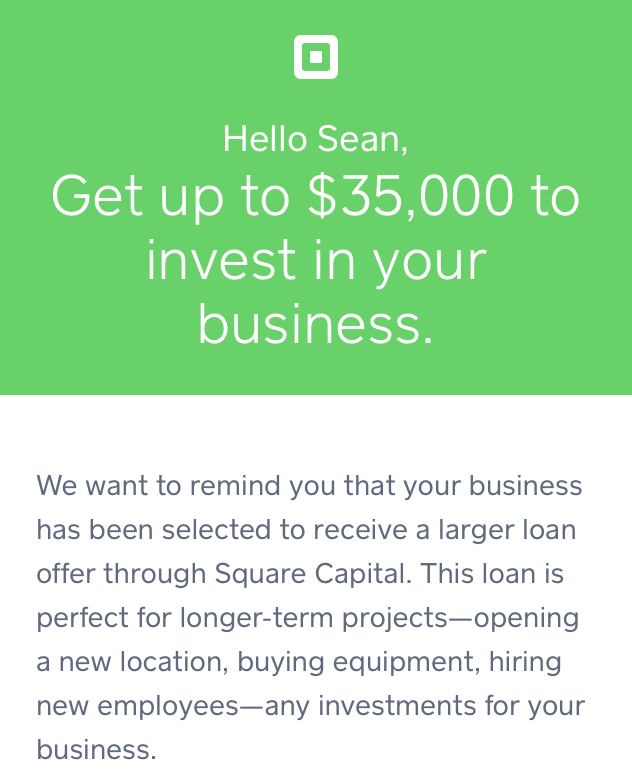

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

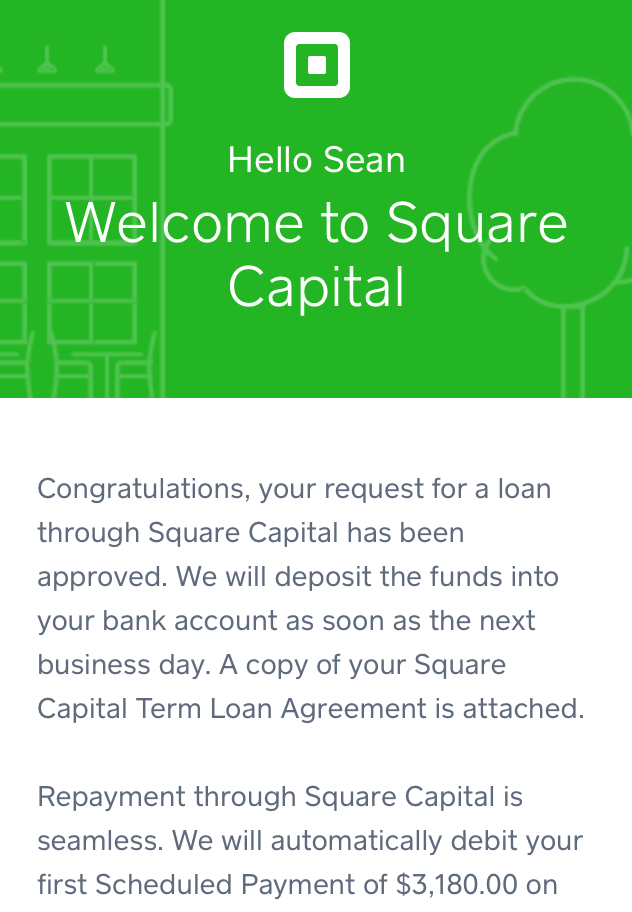

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

See You At LendIt

March 3, 2017Monday kicks off the LendIt conference at the Javits Center in NYC. Given that it’s the biggest event of the year for the industry, I certainly hope to meet as much of you there as possible.

If you still haven’t registered, make sure you at least take advantage of a 15% discount by using promo code: Debanked17USA. My schedule is pretty booked up, fueled in part by the excellent session topics this year which I want to catch a bunch of. That being the case, I am potentially available to get together even on Sunday or Wednesday (since I live in Manhattan) or any other day outside of the conference.

I hope you enjoy LendIt. You should check out their story of how they came to be HERE.

Letter From The Editor – Mar/Apr 2017

March 1, 2017Out of the many lenders and marketplaces that reported their 2016 earnings in the last month, several didn’t look so good. If algorithms and branchless-finance was supposed to make lending so much more efficient, why is it that so many online lenders are struggling to make a pro t?

As it would turn out, banks were not as doomed or as outdated as the technologists characterized them to be. Their cost of capital and brand name recognition (for most of them anyway) is proving very tough to compete with. In this issue we explore the latest trend, the drift back towards banking. That doesn’t mean that we are returning to a purely bank-dominated lending universe, however. On the contrary, it’s mainly the prime borrower market that banks are working to service better. There’s an entire segment out there for which bank financing is not the answer, at least not yet, and there’s plenty of exciting events taking place.

For small business owners, some still want a relationship with the person helping them obtain capital, they just want it in a different way. In the last few months, we spoke with several professionals who attest to having a text-based relationship with their clients, as in they communicate back and forth through their phones over text.

When I first heard about this, I assumed it had to be a one-off. “Wait, your applicants text you for updates with the underwriting process?” I asked a sales representative who seemed stunned that I would think that was odd. After a quick poll of other salespeople at a conference, the truth became clear to me. If you don’t attempt to have a text relationship with your clients, you might be at a disadvantage. In this issue, we explore why that might be.

And on that note, RU ready 4 this issue? Cuz I g2g so ttyl. Thx. ![]()

–Sean Murray