Moody’s Position on Marketplace Lending

You can’t slap a FICO score on to an entire industry but you can still assess its short term and long term risks. That’s precisely what ratings agency Moody’s has done in a report they published last month titled, 2016 Outlook – Marketplace Lending Platforms Will Continue to Evolve, Expand Loan Types.

In their report, Moody’s defines “marketplace lending” as “the growing industry of Internet-based, alternative lending platforms for consumers and small businesses.” And there’s good news, they predict it will further expand globally in 2016. The US is not even the biggest game in town, according to Moody’s, China is. “China will remain by far the largest market for marketplace lending and similar online lending platforms,” they wrote.

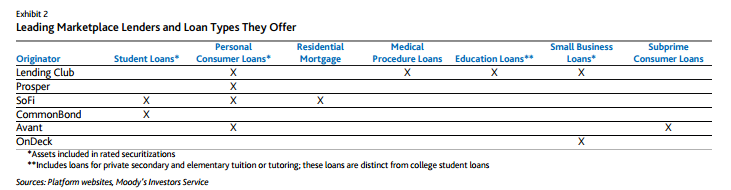

OnDeck was labeled as the leading player in the small business loan market, SoFi and CommonBond for student loans, and Lending Club, Prosper, SoFi, and Avant for personal consumer loans.

Listed among the industry’s risks is the Madden v. Midland decision. Ironically, merchant cash advance companies who gave up doing purchases of future receivables in exchange for becoming a “true lender” have found themselves wondering if merchant cash advance was perhaps the safer model all along. “Questions remain about the viability of the loan origination model many marketplace lenders currently use, in which a partner bank originates the loans, then promptly sells them to the marketplace lender,” the Moody’s report states. “This model allows marketplace lenders to take advantage of federal “rate exportation” laws and offer loans with interest rates that exceed the maximum rate otherwise allowed.”

Below are some of the other highlights:

- An increase in interest rates will not have an impact on performance but defaults will rise moderately

- Defaults on student loans will continue to be low

- Unemployment is not expected to rise in the near term

Most people probably can’t name more than 5 peer-to-peer lending platforms in the US. Meanwhile in China, there are so many that 800 of them have already failed or were recently facing major liquidity issues. There are more than 2,600 platforms there nationwide.

You can read the full 14 page report HERE

Last modified: February 19, 2016Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.