Industry News

Franklin Capital Group Has Been Acquired

October 23, 2020 This month, Franklin Capital Group was acquired by Wing Lake Capital Partners with the help of Rocky Mountain Bank. Franklin Capital will change its name and add funding capability- but the entire team will stay on. CEO Shaya Baum was happy to announce the deal, explaining that the firm would use acquisition funds to create more deals and continue to grow.

This month, Franklin Capital Group was acquired by Wing Lake Capital Partners with the help of Rocky Mountain Bank. Franklin Capital will change its name and add funding capability- but the entire team will stay on. CEO Shaya Baum was happy to announce the deal, explaining that the firm would use acquisition funds to create more deals and continue to grow.

“It gives us the ability to fund many deals that are outside of our box previously,” Baum said. “We’re going to be launching a couple of sister funds alongside what we currently have and scale the business.”

Franklin Capital was founded in 2012 as an equity fund for companies in financial trouble during, before, or post-bankruptcy. The firm discovered a market for refinancing MCA advances, finding companies that should have never obtained cash advances in the first place. Franklin Capital began offering a product to refinance cash advances through traditional loans.

“We buy out the cash advance deals,” Baum said. “In fact, most if not all of our deals come from brokers in the cash advance industry saying ‘Hey can you get us out of these deals?'”

Baum said that his firm had seen a continually growing demand for capital this year.

“I know the cash advance companies have gotten killed, but we’ve actually had the opposite problem,” Baum said. “We don’t do one-off restaurant [advances.] We’re dealing with companies that are larger, more established: they’ve all pivoted into industries that have grown during this period of time.”

DailyFunder Still #1 Small Business Finance Community

October 14, 2020 DailyFunder, the small business finance forum founded by Sean Murray in 2012, continues to be the leading online community for the industry, according to a recent announcement. The forum recently surpassed 10,000 registered members, in addition to logging more than 2 million page views just in 2020 so far.

DailyFunder, the small business finance forum founded by Sean Murray in 2012, continues to be the leading online community for the industry, according to a recent announcement. The forum recently surpassed 10,000 registered members, in addition to logging more than 2 million page views just in 2020 so far.

“The forum has attracted well over a million visitors since inception and users have historically spent longer than 10 minutes on the site in any given session on average,” Murray said.

deBanked’s parent company fully acquired DailyFunder earlier this year. The announcement was featured prominently in deBanked’s January/February 2020 magazine issue. In it, Murray renewed the website’s objective:

“The mission will be to create a great forum for those involved in day-to-day dealmaking,” he said in a Q&A. “How can we provide a platform that enables those in the industry to make more money? That’s the way I look at it. I think if we can provide that type of value, success will follow.”

The Roosevelt Hotel is Closing Permanently Due to Pandemic Losses

October 13, 2020 After nearly a century of quintessential Manhatten hospitality, the Roosevelt Hotel is closing by the end of the month, sources say. A relic of classic New York that survived the Great Depression, WWII, and Broker Fair 2019, the hotel is officially shutting down for good after suffering pandemic related losses, a spokesperson said.

After nearly a century of quintessential Manhatten hospitality, the Roosevelt Hotel is closing by the end of the month, sources say. A relic of classic New York that survived the Great Depression, WWII, and Broker Fair 2019, the hotel is officially shutting down for good after suffering pandemic related losses, a spokesperson said.

“Due to the current, unprecedented environment and the continued uncertain impact from COVID-19, the owners of The Roosevelt Hotel have made the difficult decision to close the hotel, and the associates were notified this week,” the Spokesperson told CNN reporters Friday. “The iconic hotel, along with most of New York City, has experienced very low demand, and as a result, the hotel will cease operations before the end of the year. There are currently no plans for the building beyond the scheduled closing.”

The hotel will be added to the growing list of staple New York City businesses that have closed as a result of COVID. The Roosevelt was named and built to honor the United States’ 26th president and it opened its doors on September 22, 1924. Constructed during Prohibition, the building began the modern trend of featuring designer store windows on the street front.

Appearing as a backdrop for dozens of Hollywood blockbusters like Boiler Room, Malcolm X, and The Irishman, the hotel was iconic. The New Year’s Eve tradition of singing “Auld Lang Syne” was born at the Roosevelt in 1929 when Guy Lombardo and his orchestra broadcast the song live over the radio.

Appearing as a backdrop for dozens of Hollywood blockbusters like Boiler Room, Malcolm X, and The Irishman, the hotel was iconic. The New Year’s Eve tradition of singing “Auld Lang Syne” was born at the Roosevelt in 1929 when Guy Lombardo and his orchestra broadcast the song live over the radio.

The building was purchased by the limited investment branch of Pakistan International Airlines (PIA) in 1999.

In July, government officials and PIA executives debated the hotel’s future, some hoping rumors that President Trump would purchase the property were true. The initial plan was to sell or renovate the city block to create office space, thought to be far more lucrative than the hotel business in 2019. Work-from-home orders threw a wrench into the cogs, and the hotel kept losing money: no one wanted the traditional New York experience during a pandemic.

Posting a loss during this year has become expected of the hospitality industry. According to the Bureau of Labor Statistics, hospitality lost 7.5 million jobs due to shutdowns and travel restrictions in April. CNN reported that only half as many jobs had been added back. In September, NYC hotels were below 40% occupancy.

Posting a loss during this year has become expected of the hospitality industry. According to the Bureau of Labor Statistics, hospitality lost 7.5 million jobs due to shutdowns and travel restrictions in April. CNN reported that only half as many jobs had been added back. In September, NYC hotels were below 40% occupancy.

The decision to ultimately close The Roosevelt might also come from trouble in PIA’s airline business. After the crash of PIA flight 8303 that killed 97 people in Havelian, Pakistan, European and US regulators banned flights from PIA for six months. After the crash, nearly one-third of airplane licenses in Pakistan were found to be fraudulent or forged, further straining the organization’s ability to recover.

Though this may have contributed to The Roosevelt’s closure, the pandemic sealed the deal. According to a study by the American Hotel & Lodging Association, New York has 2,336 hotels statewide that have lost 43,014 jobs this year.

Without further congressional aid, 1,565 hotels might close: the AHLA found that 74% of overall US hotels say more layoffs are coming if the industry doesn’t get additional federal assistance. But successful talks for more aid in the House and Senate are increasingly unlikely due to this election year’s heightened partisanship.

Without further congressional aid, 1,565 hotels might close: the AHLA found that 74% of overall US hotels say more layoffs are coming if the industry doesn’t get additional federal assistance. But successful talks for more aid in the House and Senate are increasingly unlikely due to this election year’s heightened partisanship.

NYC is losing yet another historical business, as the way of life and all things we have come to expect from the big apple struggle to survive. As a destination venue, The Roosevelt was also dear to deBanked. It was the home of Broker Fair 2019, where Sean Murray spoke in the same ballroom that Michel Douglas (as Gorden Gekko) made the famous “Greed is Good” speech as part of the 1987 film Wall Street. Murray made a similar speech but rewrote it to fit the industry that had gathered. “Funding small business, for lack of a better phrase, is good,” he said on stage to an audience of 700 people.

Unfortunately, it was The Roosevelt that ultimately needed funding and didn’t get it.

OnDeck / Enova Merger Overwhelmingly Approved by Shareholders

October 8, 2020The drama surrounding what OnDeck allegedly did or did not disclose to shareholders about the Enova merger presumably came to an end on Wednesday. 38 million voting shares approved the deal while less than half a million voted against it.

However, shareholders sent a message by voting against “the compensation that may be paid or become payable to the Company’s named executive officers that is based on or otherwise relates to the merger.”

OnDeck has said that the merger is expected to be completed in the fourth quarter of 2020.

Following Nine Lawsuits, OnDeck Discloses Supplementary Details Behind Planned Enova Merger

September 28, 2020

After OnDeck announced its planned merger with Enova, it was sued nine different times (See here and here) by shareholders that accused the company’s Board of Directors that they had failed to disclose material information about the deal.

OnDeck formally responded on Monday, September 28th, wherein they disclosed that plaintiffs in all of those actions had agreed to dismiss their claims in light of the release of this supplemental information:

The Company and Enova believe that the claims asserted in the Actions are without merit and that no supplemental disclosures are required under applicable law. However, in an effort to put the claims that were or could have been asserted to rest, to avoid nuisance, minimize costs and avoid potential transaction delays, and without admitting any liability or wrongdoing, the Company has determined to voluntarily supplement the Proxy Statement/Prospectus as described in this Current Report on Form 8-K to address claims asserted in the Actions, and the plaintiffs in the Actions have agreed to voluntarily dismiss the Actions in light of, among other things, this supplemental disclosure. Nothing in this Current Report on Form 8-K shall be deemed an admission of the legal necessity or materiality of any of the disclosures set forth herein. To the contrary, the Company and the other defendants specifically deny all allegations in the Actions that any additional disclosure was or is required and expressly maintain that, to the extent applicable, they have complied with their respective legal obligations.

OnDeck first re-explained its background situation leading up to the Enova deal:

Starting in April 2020, OnDeck management commenced a review of potential financing options to secure additional liquidity and potentially replace the Corporate Line Facility and began contacting potential sources of alternative financing, including mezzanine debt. OnDeck contacted, or was contacted by, more than ten potential sources of mezzanine or alternative financing, and received pricing indications from four sources. The interest rates offered by those alternative financing sources ranged from 1-month LIBOR plus 900 basis points to 1,700 basis points (in addition to an upfront fee) and all but one required a significantly dilutive equity component. The one proposal that did not include an equity component was at an interest rate of 1-month LIBOR plus 1,400 basis points to 1,700 basis points. Based on the initial term sheets proposed, OnDeck engaged in negotiations with each of the four potential sources of alternative financing. As these negotiations progressed and COVID-19’s impact on the macro economy and OnDeck’s loan portfolio intensified, two of the four potential sources of alternative financing ceased to actively participate in negotiations. Discussions with the final two potential sources of alternative financing remained ongoing through the time that OnDeck and Enova entered into the merger agreement. Throughout the Process, OnDeck management reported the status of such negotiations on a frequent and ongoing basis to the OnDeck Board for its deliberation in the context of OnDeck’s standalone plan, and the OnDeck Board considered the significant uncertainty of being able to reach agreement on alternative financing in its decision to enter into the merger agreement.

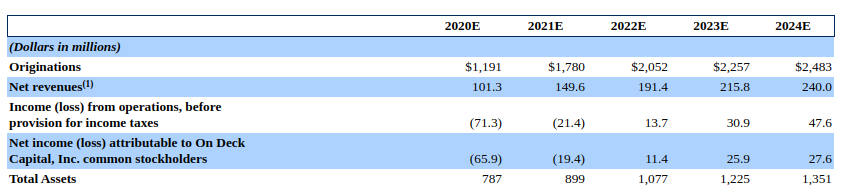

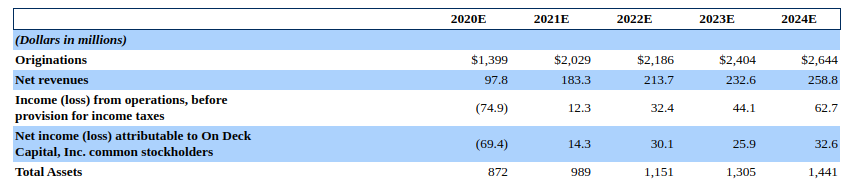

Of particular contention in the deal were OnDeck’s financial projections, prepared to estimate OnDeck’s trajectory as an independent entity. Shareholders complained that there were two sets of books and that they only got to see one. The other set, dubbed Scenario 1, had been used to shop OnDeck around to other suitors. OnDeck published both sets in their supplemental materials on Monday.

The difference is stark. Originally disclosed to shareholders was a projected cumulative net loss of $20.4 million through the end of 2024. The other set of projections, Scenario 1, state a cumulative net income of $33.5 million over the same time period, a difference of over $50 million.

The original predicted a 2021 net loss of $19.4 million while Scenario 1 predicted a net income of $14.3 million.

One reason offered for selecting the less optimistic of the two is that OnDeck’s management determined that loan originations were trending below both sets of projections as of July 12th. OnDeck announced the Enova deal about two weeks later.

Shareholders will cast their votes on the merger on October 7th. OnDeck’s Board “unanimously recommends” that they vote in favor of the proposed merger with Enova.

United Capital Source CEO Jared Weitz Discusses The State of Small Business Finance

September 24, 2020Jared Weitz, the CEO of United Capital Source, recently sat down (virtually) for an interview with me to discuss the state of small business finance. During it, Weitz makes an alarming prediction, that pandemic related events will lead to 50% of all restaurants permanently closing. You can watch our full talk below:

Additional Lawsuits Filed Against OnDeck Directors Over Enova Deal

September 14, 2020At least three federal lawsuits have been filed against the directors of OnDeck relating to the announcement that the company is being acquired by Enova. These suits allege securities act violations with regards to how the technical aspects of the deal were disclosed while the initially reported action in the Delaware Court of Chancery alleged a breach of fiduciary duty.

The federal securities lawsuits are:

Daniel Senteno v. On Deck Capital, Inc. et al – Case 1:20-cv-01179-MN

Eric Sabatini (on behalf of a class) v On Deck Capital, Inc et al – Case 1:20-cv-01166-MN

Mohamed Aboubih v On Deck Capital, Inc. et al – Case 1:20-cv-07319-Vm

LendingPoint Partners with eBay to Fund Online Sellers

August 6, 2020 LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

LendingPoint announced this week that it is partnering with the online marketplace eBay to provide funding to sellers on its platform. Titled eBay Seller Capital, the program will offer terms of up to 48 months, with no origination or early payback fees, and which will be capped at $25,000 during its pilot program.

“We’re committed to empowering entrepreneurs to make their dreams a reality, and we are continuing to partner with our sellers to provide them with the tools they need to thrive, eBay’s VP of Global Payments Alyssa Cutright said in a statement. “We’re excited to make flexible financing options available that are integrated with our new payments experience. The program with LendingPoint will enable critical funding opportunities for eBay sellers, especially during this time of economic uncertainty.”

In its early stages now, eBay Seller Capital will only be available for selected sellers, with the plan being for it to be made available to all eligible sellers in the US later this year. Beyond the program, LendingPoint has made clear in its statement that it aims to “expand their offering to provide eBay sellers with more tools to help run their businesses,” however, when asked, CEO and Co-Founder Tom Burnside did not give details of these future plans.

“I don’t want to leave the proverbial cat out of the bag yet with that,” Burnside commented in a call, “but what I will tell you is that I think when we are done eBay will be able to offer best-of-class seller financing.”