Business Lending

BriteCap Financial Ramps Up Team, Ready For Growth

December 20, 2024 The stream of announcements coming out of BriteCap Financial garnered notice. It started with news of a $150M credit facility back in August, followed by announcements of a new CEO, CFO, CCO, VPs, and more. The new CEO, Richard Henderson, whose CV includes previous roles at CAN Capital, Marlin Capital Solutions, and Direct Capital, told deBanked that the company wanted to have the right team in place to carefully grow the business. BriteCap, which is part of the North Mill family of companies, offers attractive term loans to small businesses.

The stream of announcements coming out of BriteCap Financial garnered notice. It started with news of a $150M credit facility back in August, followed by announcements of a new CEO, CFO, CCO, VPs, and more. The new CEO, Richard Henderson, whose CV includes previous roles at CAN Capital, Marlin Capital Solutions, and Direct Capital, told deBanked that the company wanted to have the right team in place to carefully grow the business. BriteCap, which is part of the North Mill family of companies, offers attractive term loans to small businesses.

As part of the plan, the company is looking to add not just new brokers but the right brokers, especially given the upstream programs they offer to merchants. “We’re being very selective on who we onboard,” said Henderson. “We’re trying to make sure that we’ll use that to get to scale, but also to build powerful relationships with those brokers where it’s a true partnership.”

BriteCap has developed an online checkout system to streamline the funding process. It can be configured to work with however the broker is used to working. They’ve focused a lot on the mobile experience so that a merchant need not even be in front of a computer to go through it.

One notable advantage to BriteCap is precisely that affiliation with the North Mill family because it opens up the possibility of not just working capital as a solution but also equipment finance. According to Henderson, the potential crossover between the products works well especially when the deals have been originated in the right context. That context includes the best practices and professionalism that equipment finance brokers typically operate within.

Among the C-suite executives to recently join BriteCap are Pushkar Choudhuri as Chief Financial Officer and David Lafferty as Chief Credit Officer. The timing of everything aligns with the firm’s economic sentiments. Henderson said that he believes optimism is higher now and growing.

“…generally speaking, we’ve seen demand picking up and we have a pretty bullish view on the economy moving forward,” he said. “I think we’re entering into a very good time in our space.”

SBA Names Members to its Small Business Lending Advisory Council

December 11, 2024The results are finally in. After a six-month review period, the SBA finally announced the applicants that have been approved to serve on its inaugural small business lending advisory council.

They are:

- Paul Brown, Managing Partner, Michigan eLab Investment Co.

- Sheryl Cameron, Executive Director SBA Solutions, JPMorgan Chase

- Kevin Carey, Interim President and CEO, American Hotel and Lodging Association

- Ellis Carr, President and CEO, CDC Small Business Finance

- Jill Castilla, President and CEO, Citizens Bank of Edmond

- Tammy deClercq, COO Head of Operations SBA, Lendistry SBLC

- Jeff Dick, Chairman and CEO, MainStreet Bank (VA)

- Nicole Dilts, VP of Commercial Solutions, Michigan State University Federal Credit Union

- Maggie Ference, SVP Small Business and SBA Director, Huntington National Bank

- Jeff Hansel, 1st VP, Rockland Trust Company

- Amy Hereford, President and CEO, LiftFund Inc.

- Ernest Hunter, CEO, Frenchy’s

- Duane Lewis, Interim Co-CEO, Black Business Investment Fund Inc.

- Deborah Partin, SVP of Lending, Rural Enterprises of Oklahoma, Inc.

- Amy Patel, EVP Head of Commercial Distribution, TD Bank

- Giovanna Piovanetti, Executive President, Corporacion para el Financiamiento Empresarial del Comercio y De Las Comunidades

- Lane Rhodes, VP Senior Loan Officer, Live Oak Bank

- Mark Robertson, President and CEO, PCR Small Business Development Corporation

- April Schneider, Head of Small and Business Banking, Wells Fargo

The published list is about six members short of the planned 25 so it is likely a few more will be added. To be eligible, applicants had to have “experience and technical expertise in such areas as commercial lending, small business finance, government-guaranteed lending, small business advocacy or advisement, and expertise needed to provide advice on SBA’s loan programs.”

LiftFund and Lendistry are arguably the only two from the fintech space.

Are You The Top Broker?!

November 21, 2024

Broker Battle returns on February 20, 2025 at deBanked CONNECT MIAMI. The competition, now the 2nd ever after last year’s very successful launch, is back with an improved format that allows for almost any qualified broker the opportunity to be tested LIVE in person. Broker Battle TWO will also have 3 separate broker categories versus last year’s catch-all. Those categories are Revenue Based Finance, SBA Lending, and Equipment Financing.

All competing brokers will be vetted, tested, and scored through very short judging rounds on the showcase floor. The two top scores from each category will actually compete on stage for the championship.

That means that as opposed to last year’s 6 total contestants and 7 separate battles on stage, this year’s competition could feasibly manage up to 100 contestants for which there will only be 3 total battles on stage (each being a championship). The format allows for more brokers to prove themselves in person while reducing total stage time for the final grand performance.

Each broker will win a cash prize and the distinction of being Top Broker (in their category). To be eligible for entry, you must be an active broker with good ethics and a positive reputation. You must also be registered to attend deBanked CONNECT MIAMI where it will take place and enter yourself in the battle itself here.

Broker Battle intends to foster best practices.

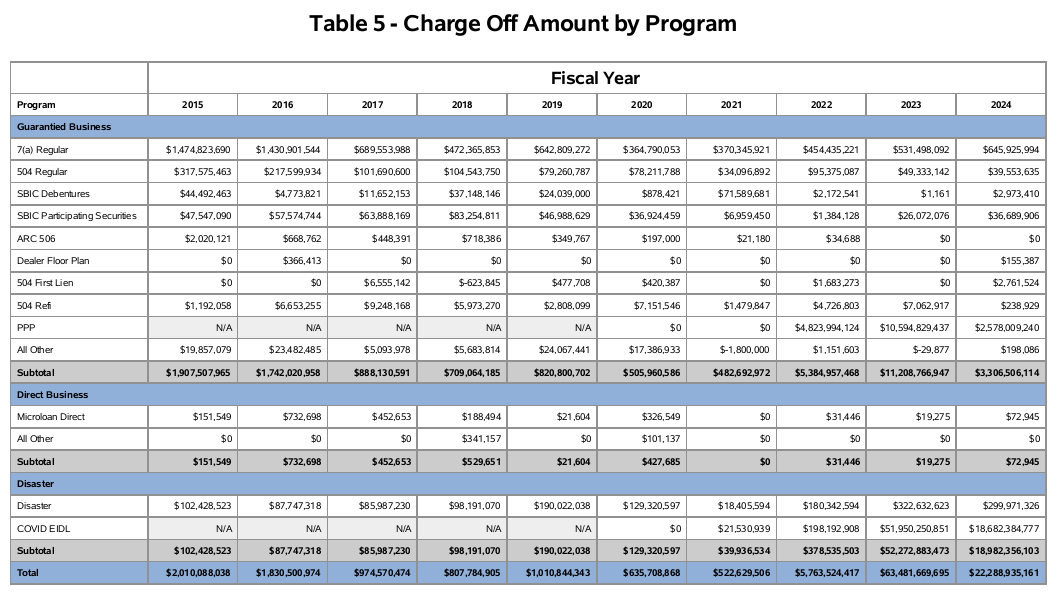

Cumulative Covid EIDL Chargeoffs Now Exceed $70 Billion

November 19, 2024The latest data from the SBA is in. It charged off $18.7B in Covid EIDL loans in FY 2024. That was down from $52B charged-off in FY 2023. The program still has an unpaid principal balance of $277B.

PPP loans were still being written off in FY 2024 as well, coming in $2.5B charged-off vs $10.6B charged-off in FY 2023 and $4.8B charged-off in FY 2022.

The EIDL program suffered astonishingly high losses during covid. Regular 7(a) loans, for example, only experienced $646M in charge-offs in FY 2024.

Shopify Capital Originates $837M in Business Loans & MCAs in Q3

November 15, 2024Shopify Capital originated $837 million in business loans and merchant cash advances in Q3, putting the grand total at $2.1B for the first 3 quarters. During the earnings call, Shopify said that loss ratios remained within the consistent range.

Compared to some of their competitors in the online space, Shopify Capital ranks third:

Q3 originations:

Square Loans: $1.38B

Enova: $1B

Shopify Capital: $837M

Ready Capital Grows as Leading Non-Bank Small Business Lender

November 10, 2024 “Ready Capital has become a leading national non-bank lender to small businesses providing a full suite of loan options from $10,000 unsecured working capital loans to $25 million plus real estate-backed USDA loans,” said Ready Capital CEO Thomas Capasse during the company’s Q3 earnings call.

“Ready Capital has become a leading national non-bank lender to small businesses providing a full suite of loan options from $10,000 unsecured working capital loans to $25 million plus real estate-backed USDA loans,” said Ready Capital CEO Thomas Capasse during the company’s Q3 earnings call.

Ready, in some ways, has flown under the radar in recognition. On the one hand the company is the top non-bank SBA lender in the country and fourth overall SBA lender in the country. On the other hand, the company has previously acquired Knight Capital, iBusiness Funding, Madison One Capital, select non-SBA assets of Fountainhead, and Funding Circle USA. The result is that the overall organization is a powerhouse with a current public market cap of $1.25B.

iBusiness Funding, once the technology arm of Knight Capital, has played an integral role for the company. For example, when Ready acquired Funding Circle USA, it did it through the iBusiness Funding brand.

“[In 2019, iBusiness Funding was] a leader in unsecured small business lending,” Capasse said on the call. “And then they adopted their tech to the PPP which was very accretive. And since then there’s been the initiative within the SBA to emphasize small loans below $350,000, which many times are minority women-owned businesses, and so that’s been a significant initiative by the SBA& and so what we’ve done is iBusiness has developed a tech stack, which is now being marketed as a third-party underwriting model for banks. Banks just do not focus on that at all. Even if they do SBA loans, it’s mostly for larger loans again above the $350,000 to the $5 million. So the idea with iBusiness is to grow the revenue stream from this software-based business.”

On Funding Circle, Capasse said that the newly acquired subsidiary would be “accretive to earnings once fully ramped.” The numbers offered so far was that $6.6 million growth in Q3 origination income came from small business working capital loans through the Funding Circle platform.

Nerdwallet: Continued “Pressure in SMB Loan Originations”, Search Engine Traffic Flux

October 30, 2024 “We continue to see pressure in SMB loan originations, with rates remaining elevated and underwriting remaining tight,” said Lauren StClair, CFO of NerdWallet on the Q3 earnings call, “However, this was more than offset by growth in our renewals portfolio, which showcases the benefit of our vertical integration strategy and the reoccurring nature of the vertical when we pursue a higher touch experience.”

“We continue to see pressure in SMB loan originations, with rates remaining elevated and underwriting remaining tight,” said Lauren StClair, CFO of NerdWallet on the Q3 earnings call, “However, this was more than offset by growth in our renewals portfolio, which showcases the benefit of our vertical integration strategy and the reoccurring nature of the vertical when we pursue a higher touch experience.”

NerdWallet CEO Tim Chen further said that it was a “tough macro environment in SMB loans.”

Their SMB business overall, which includes several products, not just loan referrals, did well however in Q3, generating double digit YoY growth for a total of $27.8M in revenue.

Of additional note is NerdWallet’s commentary on search engine traffic and its impact to its business.

“After a stronger start of the quarter, we saw some additional deterioration in our search visibility in mid-Q3,” said Chen. “While traffic to our monetizing shopping-oriented content started to rebound as we exited the quarter, traffic to our non-monetizing learning-oriented content did not. As a result, Monthly Unique Users were down 7% year-over-year in Q3.”

deBanked drew attention to their search engine observations this past August after hearing Chen muse that the current state of organic search result rankings were not actually helping business owners get business loans. Chen dived into this subject yet again on the Q3 call, the full quote of which is worth including:

“So, during our Q2 call, our search visibility was broadly stabilizing and actually starting to rebound a little bit. And then soon after our Q2 call, things took a turn for the worse. So with our shopping traffic, things got worse in August and September. But then going into October, rebounded back to a level that was a bit better even than where we were when we did the Q2 call. We think we did some things on our end to clean up the user experience that were net positive. Now, there were some exceptions, so for example, parts of credit cards and personal loans are still lagging. But, overall, we got a pretty good place – we got to a pretty good place on shopping pages and feel like we’ve figured out what to improve.

Conversely, for that far bigger bucket of education-oriented traffic that is less commercial in nature, things got progressively worse throughout the quarter and recently stabilized at a lower level. So, what’s happening there is a renewed push by search engines to incorporate their own answers directly into the search results, like you mentioned AI overviews as an example. So, for those of you who have been following search over the years, this isn’t really anything new. So, for example, at one point when you search for the weather, it didn’t show up directly in the results, and eventually a module was inserted there. That trend towards the simpler stuff being pulled into search results is inevitable, and we’ve always been more insulated from that, but historically it happens in waves, and sometimes haircuts are MUUs.

So, we’ve generally seen a re-baselining after any major changes, and then eventual growth from there as you lap the impact. Oftentimes, those changes are rolled back. And so, over the last 10 years, I’d say these changes come in waves, and we’re in the middle of a big wave, and as long as we focus on delivering consumer value, we’re steering in the right direction, and things tend to sort themselves out. So, this headwind is driving our outlook for further MUU deceleration in Q4, because of the full quarter impact of some of the stuff that happened with those headwinds.

Now, in the long run, I do think an improving search experience is a win for the overall ecosystem and keeps it healthy and growing. And, really, I’d say the silver lining here is that Q3 was pretty brutal as far as some of the headwinds we faced in organic search, especially in highly commercial areas, and being able to hit like a 12% NGOI margin in Q3 in spite of that headwind is really a testament to some of the progress we’ve made in building a brand and a direct relationship with our users and our increasing competitiveness in other channels.”

PayPal is Back to Growing its Merchant Lending Program

October 29, 2024 After taking drastic action over the last year to rein in surging SMB lending charge-offs, PayPal believes it has corrected the issue.

After taking drastic action over the last year to rein in surging SMB lending charge-offs, PayPal believes it has corrected the issue.

“We have now fully lapped the actions taken last year to tighten credit underwriting and reduce on balance sheet risk,” said PayPal CFO Jamie Miller on the Q3 earnings call. “We’re seeing better performance across the portfolio, and have now started to modestly grow merchant originations. We’ll continue to prudently manage the portfolio’s exposure with the goal of sustaining our balance sheet-business model, while providing our customers with more ways to manage their cash flow, spending and borrowing needs.”

The reduction in originations since the pullback had been severe, down by as much as 50% by deBanked’s prior estimates.