AI

NerdWallet: “We are in the middle of an AI transition that is changing how people get their answers to their money questions”

August 7, 2026NerdWallet users have traditionally turned to Google to begin their financial journeys. A question entered into the search bar would surface a NerdWallet article, sending users to the company’s site. Now, that behavior is changing.

“We are in the middle of an AI transition that is changing how people get their answers to their money questions,” said NerdWallet CEO Tim Chen during the Q2 earnings call.

As the company has noted in previous quarters, some traffic is now coming from LLMs. While it remains a small share of overall traffic, those visitors tend to convert at a high rate.

“I think intent is extremely high when someone is coming through an LLM in terms of wanting to transact in a marketplace,” said Chen. “It continues to be a pretty small part of our business today, but it’s definitely an area of investment and growth for us.”

Analysts have continued to press the company on the subject. And while Chen has said that “the story is still being written,” he believes enough change has already taken place to provide a clearer picture of where things are headed.

“We’ve already entered a phase where you’ve got billions of weekly active users across major LLMs,” Chen said. “Mass adoption is already taking place, right? I think a lot of the impact that we’ve already seen in terms of our educational content being affected the last three years, has played out. I think we’re starting to see what the future looks like.”

Chen also emphasized that having a trusted brand will be critical to succeeding in this new era.

“The importance of that trusted brand when you’re talking about offering marketplaces and high stakes financial guidance is really front and center,” he said. “I just think we’re really well-positioned there.”

LendingTree: “Using AI as a Communications Tool With the Consumer is Very Exciting.”

August 3, 2026“I think using AI as a communication tool with the consumer is very exciting,” said LendingTree CEO Scott Peyree during the Q2 earnings call. “For example, we develop a lead. Instead of sending that lead out five times and having five different brokers call the consumer a bunch, it’s like first have that—whether it’s voice or text or email—have that AI agent engage and communicate with the consumer a little bit first to get a little further detail on it.”

The substance of that conversation would be to clarify what type of factors are the most important, and then directing them to one or two companies that are best suited for that rather than to five.

“That’s a dramatically better consumer experience, and it’s a really useful way to use AI from a consumer-facing perspective,” said Peyree.

The Fatal Flaw in Upstart CEO’s Vision for AI Underwriting in MCA: A response to Upstart’s view of AI in underwriting

June 12, 2026David Roitblat is the founder and CEO of AI My Advance and Better Accounting Solutions, a leading authority in specialized accounting for merchant cash advance companies alongside our new innovative CRM designed to solve the critical gaps holding the industry back. To connect or schedule a call about working with AI My Advance or Better Accounting Solutions, email David@betteraccountingsolutions.com

As deBanked reported (March 23, 2026), Paul Gu, CEO of Upstart, said something on his company’s Q4 earnings call that has been quoted approvingly in a few corners of the credit world. It deserves a careful read because some important points are incorrect when it comes to the MCA industry.

Gu’s argument, as reported, runs roughly like this. Humans have never been very good at precisely underwriting loans and projecting cash flows. That problem has always been a math problem, not a language problem. The recent wave of AI, the LLMs from Anthropic, OpenAI, and Google, is good at the things humans are naturally good at: reading documents, navigating messy paperwork, perfecting liens, and checking property records. Therefore, in Gu’s framing, LLMs are well-suited to the operational layer around lending but not to the underwriting decision itself. He puts it bluntly: “No matter how many humans you have, you don’t want that army of humans underwriting loans for you.”

The deBanked piece does a real service by reporting it. But the framing carries a serious blind spot. It implies that AI underwriting is essentially a solved problem, owned by structured-data shops like Upstart, and that the broader conversation about AI in lending is mostly noise. For consumer credit, that may be true. For the MCA industry, it is not, and treating it as if it were misses the actual point.

Begin with the parts of his argument that hold up. Underwriting, at its core, is a probability problem. Given a set of inputs, what is the likelihood of repayment, and what is the distribution of outcomes if it fails? That has always been the question, and Gu’s phrasing is exactly right: “That’s something that has always been solved as a big math problem.”

He is also correct in saying that LLMs, in their current form, are not the natural tool for that math problem. They are extraordinary at reading, summarizing, classifying, extracting, and reasoning over language. They are not, on their own, the right architecture for portfolio-level probability estimation. The deBanked piece links to Upstart’s own track record, 91% of their loans now fully automated, and that result was not built on top of GPT-class models. It was built on years of structured-data modeling. Gu is entitled to point that out.

He is also right that the most obvious near-term wins from LLMs in lending are operational: HELOC processing, lien perfection, document review, title work. Anywhere a human currently spends hours reading and routing paper, an LLM can do meaningful work. His framing of those as “the perfect problem to throw sort of LLM-style AI against” is well put.

The problem is the conclusion the framing pushes the reader toward: that because the underwriting decision is a math problem, and because the new wave of AI is mostly a language problem, the conversation about AI in underwriting is largely settled. That conclusion translates poorly from Upstart’s world to ours, and it does so in a way that matters.

Upstart underwrites consumer installment loans. The data is clean, the durations are predictable, the borrowers are individuals with credit files, and the question being asked is essentially: will this person make 36 or 60 fixed monthly payments on time. That is, as Gu says, a big math problem with a long history of structured inputs.

MCA underwriting is not that problem. It is a different problem with a different shape, and the difference is not cosmetic.

An MCA underwriter is not pricing a fixed-term installment loan to an individual with a credit file. They are pricing a daily or weekly remittance against a small business’s future receivables, over a horizon measured in months, where the inputs are messy by nature: bank statements with idiosyncratic categorization, industry-specific seasonality, owner behavior that does not show up in a FICO score, stacking risk, processor changes, lease events, partner disputes, and dozens of other signals that live in unstructured form. The decision is not made once and then monitored passively. It is revisited continuously as the merchant’s behavior evolves over the life of the advance.

That is a different beast, and the math that solves consumer credit does not, on its own, solve it. The part of AI that Gu sets aside, the language part, the unstructured-data part, the continuously-observing part, is precisely the part that matters for the underwriting decision itself in MCA, not just the paperwork around it. Setting it aside is not a clean theoretical move. It is a category error when applied to this industry.

In modern MCA operations, the most important thing AI is doing is not the initial decision. It is what happens after the capital goes out.

Underwriting does not end at approval. Our new and up-and-coming platform continues to ingest merchant behavior after funding. It links directly to merchant bank accounts, monitors post-funding activity, tracks changes in deposit patterns and remittance behavior, and detects patterns across defaulted deals. It does not simply record that a deal failed. It identifies what those failed deals had in common. That information does not sit in a static report. It feeds directly back into how new deals are evaluated.

That is underwriting, too. It is just underwriting, not the single-moment, single-file decision the term usually evokes. It is a feedback system: the decision at funding is the first input, the merchant’s subsequent behavior is the second, and the model that prices the next deal is the third.

Gu’s framing treats underwriting as the moment of decision. In MCA, the moment of decision is a single frame in a longer film. The frames that matter most are often the ones after funding, where a human underwriter cannot realistically hold the pattern in mind across hundreds or thousands of merchants, while a system can. Any framework that ignores those frames does not describe MCA underwriting. It describes something else and calls it by the same name.

This is also where the LLM-versus-structured-model dichotomy starts to fall apart. Reading a bank statement well is partly a math problem and partly a language problem. Categorizing a $4,200 ACH out as a vendor payment versus a stacked advance from another funder is not pure math. It requires reading the counterparty name, recognizing the funder, knowing the industry conventions. That work sits exactly at the seam between what Gu calls “solved as a big math problem” and what he calls “the perfect problem to throw sort of LLM-style AI against.” In MCA, those two are not separable layers. They are the same workflow, and pretending otherwise produces a model of the industry that does not match how the industry actually runs.

The deeper point is that the AI conversation in lending is not one conversation. Upstart’s answer is the right answer for Upstart’s problem. It does not automatically transfer, and the confidence with which it has been quoted in the credit world suggests the transfer is being assumed rather than examined.

Consumer credit, where Upstart operates, has had decades of structured-data infrastructure built around it: bureaus, scores, standardized loan documents, regulated disclosures, and well-defined repayment behavior. A math-heavy, low-LLM approach makes sense there because the inputs were already structured by the time the modeling started.

MCA grew up differently. The data is unstructured by default. The borrowers do not have meaningful credit files in the consumer sense. The product is non-recourse against a fluctuating revenue stream. The lifecycle is short and active. The signal that matters often lives in places, bank statement memos, merchant behavior, processor data, partner disputes, that look like language problems and behavior problems before they look like math problems.

That is why the LLM-style AI Gu is comfortable assigning “around the edges” work, which, in MCA, frequently involves core underwriting. Parsing the statement is part of underwriting. Reading the memo line is part of underwriting. Recognizing the third stacked funder is part of underwriting. Watching how a merchant’s deposit pattern shifts in week three of an advance is part of underwriting. Those are not auxiliary tasks bolted onto a clean math problem. They are the problem.

The disagreement with Gu, then, is not that AI cannot underwrite. He is not really arguing that. His actual position is closer to this: LLMs are not the right tool for the underwriting math, and you should not let the hype around LLMs convince you otherwise. On that, we agree.

The disagreement is this. In MCA, the underwriting problem is a math problem wrapped in a language problem wrapped in a continuous-monitoring problem. The math is necessary but not sufficient. The language and behavioral layers are where modern AI, LLM-style and otherwise, is genuinely changing how deals are priced, monitored, and learned from. With our new and up-and-coming platform, AI My Advance, this is exactly what we do: we parse the unstructured inputs, track merchant behavior after funding, and feed what we learn from defaulted deals back into how the next deal gets priced. Treating that work as merely “operational” is not a small mistake. It is the kind of mistake that produces a confident answer to the wrong question.

Upstart has earned the right to its view. The 91% automation figure is real, and the underlying modeling is serious. But that view was built on a problem whose inputs were already structured. The MCA industry is solving a different problem in real time, and the tools that work for it are not the same tools, in the same proportions, as those that work in consumer credit. The sooner that distinction is named clearly, the better the conversation about AI in lending becomes.

How LendingClub (Happen Bank) Plans to Handle Customers Using AI Agents To Seek Out a Loan vs. Search Engines Like Google

April 28, 2026During LendingClub’s Q1 earnings call, stock analyst David Scharf asked LendingClub CEO Scott Sanborn how they’re approaching investments in AI-type search vs. traditional. Scharf used this example for context:

Scharf:

…specifically, I was just typing in how do I get a $10,000 personal loan and it just gives you the typical Google paid search listing of whoever shows up, then I said what’s the best $10,000 loan for me and it did the typical NERDWallet shows up. But going forward, when somebody types in, a year from now, what’s the best $15,000 personal loan for me into either Chat or Claude, can you talk us through either some of the risks or opportunities you see in terms of these AI engines making more qualitative assessments and not just traditional search assessments?

Sanborn’s excerpted response:

So it’s a great question. And while it is a buzzword, it is also — that does not take away from the fact that the changes underway are very real, and we are pursuing them, as I mentioned in the prepared remarks, across really all departments and all aspects of the company.

[…]

So inertia is really the thing we’re trying to overcome. So if the agents evolve not only to replace Google search, but potentially to act on behalf of consumers, we think we’re a net beneficiary. But you’re right, it is as a percentage of web traffic right now, it is quite small. That said, it is high intent. And so as that percentage grows, we need to be there for it.

All of the protocols are not established exactly what the — as I’m sure you know, there are many, many, many firms that are engineering themselves around how to optimize for Google’s ever-changing algorithm that same thing will be true for agentic search, and we are going to be going after that the same way we will sort of core organic search and think we’re set to benefit. Right now, that means likely increasing the amount of content we produce to get out there. We’re already in the site. We’re obviously in the places you mentioned. We’re in NerdWallet Best Of, I think, on both sides of our balance sheet. So we’re already there.

But we need to be getting some of our content out on our own to help with that. So we’re pushing behind that throughout this year. That’s definitely on our plan.

LendingClub previously announced that it is rebranding to Happen Bank.

Lending Tree: LLM Referrals Are Very “High-Intent Consumers”

March 3, 2026 During Lending Tree’s Q4 earnings call, CEO Scott Peyree echoed the same conclusion on LLMs that was uttered by rival NerdWallet, that LLM referrals convert better than normal search referrals.

During Lending Tree’s Q4 earnings call, CEO Scott Peyree echoed the same conclusion on LLMs that was uttered by rival NerdWallet, that LLM referrals convert better than normal search referrals.

“There are a number of fronts we are working on there,” said Peyree. “There is obviously the SEO front where you are getting referenced by the LLMs, driving consumers to our site. We continue to focus on that and it continues to grow. It is very high-intent consumers, as I have mentioned on previous calls. I would say, materially, it is still a pretty small percentage of our overall consumer base, but it is continuing to grow.”

Lending Tree hinted that there was an opportunity to capture more LLM traffic through paid LLM advertising going forward but that they couldn’t say to what extent yet for 2026.

“Some of the LLMs, ChatGPT being an example, are looking to start testing some advertising, which we are excited about participating in,” Peyree said.

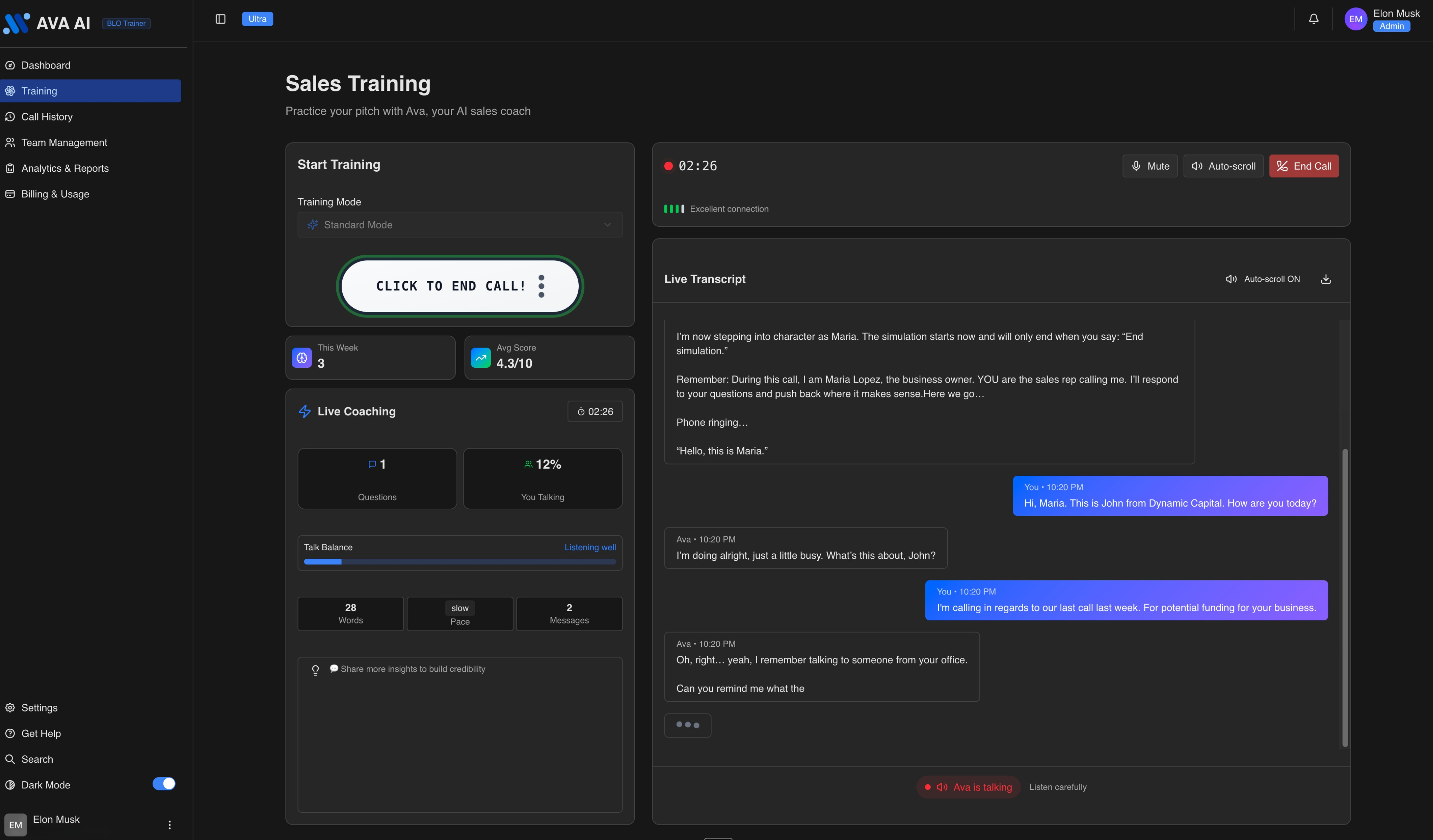

Getting Your Reps to Perform at the Ultimate Level? This ISO is Using AI to Train Them

February 2, 2026“I‘m unable to get 80, 90 guys to work in the area that I am in so I have to actually max out the team that I have,” says Steven Edisis, CEO of Dynamic Capital. “So my whole thing is onboarding guys and getting them to perform at the ultimate level.”

Edisis says that training small business finance sales reps takes extreme discipline, hours and hours of manual training. Training in the morning. Training in the afternoon. Training at night. Training and then some more training. Some of that training involves roleplaying. Other times it’s live calls. In either case, he’s found there are weaknesses in those systems. For instance, in a roleplay, the trainer has to contend with maintaining rapport with the individual they’re training. Persistent unfavorable feedback, even if warranted, could actually be demoralizing and create tension in the relationship.

“When you’re roleplaying with your buddy, your buddy’s a human,” Edisis says. “After two or three or four times of them getting it wrong, do you just stop correcting it? And you let it go.”

The end result is that they’re not actually in top shape and ready for calls, but they could be deceived into thinking that they are. Meanwhile, live-call training presents another dilemma. If you give the trainee good leads and they mess up, are the good leads wasted? And if you give them really cheap leads and they don’t get anywhere with them, how are they supposed to be judged or learn from it?

For Dynamic Capital, the solution to all of the above has been AI. About a year ago, Edisis began using an AI agent called Ava, a product by Reech AI that’s led by CEO Liran Weissenberg. Ava does for Dynamic Capital what Edisis did for a long time, trains, but on steroids. Trainees, experienced reps, and even veteran pros at the game can roleplay with Ava, a voice AI, in any setup of circumstances they choose. It can be a straight-up cold call, a warm lead, or a follow-up, for example. It can be tuned to easy mode, regular mode, hard mode, or even impossible mode. The best part is that Ava knows how to play the role of a merchant, speaks in real time, and speaks with human-believable tones and emotions. Voice AI technology, once considered clunky or plagued by latency in years past, has finally become virtually indiscernible from a real person.

In a live demo performed for deBanked to show it in action, the AI answered the phone and Edisis went right into the normal flow of business.

“This is Steven with Dynamic Capital. Last week you went online, requested some information for some working capital for your business, how are you today?”

“I’m ok, just a little busy right now,” Ava responded somewhat suspiciously. “yeah, I remember poking around online. I put in my info but I never really got a clear idea what you guys actually do.”

From there, Edisis played it out to a conclusion. When it was over, Ava rated him on his performance, gave him a score, and shared what he did well, as well as things he could have done better. It seemed to understand the relevance of open balances a merchant might have with loans or MCAs, which is key to making it impactful. Ava’s an AI, so a trainee would not be able to attribute the constructive criticism it offered to being singled out or picked on. For instance, if the AI said the trainee needed to work on tone and pacing of speech, there’s no way for the trainee to attribute that to personal bias from a trainer.

“The cool thing is that we can model the AI to behave in very specific scenarios and to have very specific analysis,” said Weissenberg of Reech AI, who created Ava.

Meanwhile, no real leads were wasted in the process. This is especially valuable since Edisis says that he teaches a specific technique—or rather, an art—called the interruption, a very delicate tactic used to keep a call on track. But it only works if delivered correctly, because it involves literally interrupting the prospect while they’re speaking. Learning how to interrupt in the circumstances that call for it is a massive gamble that could not only lead to lost sales revenue but also negative customer feedback if executed poorly. This is a perfect example of where AI training comes into play.

“It’s really nice to [practice it] on Ava versus blowing up and getting negative reviews from a live person,” Edisis said. “So that’s a really cool way that I can train people.”

Weissenberg said that when Ava is being used across a whole sales floor, a sales manager can view transcripts of all the calls, along with feedback and analytics. One could literally have a full-on simulated call center where all the prospects are AI agents being used to train reps.

“The coolest thing about the app is the analytics,” Weissenberg said. “It’s only going to get better too because AI is getting smarter and it’s getting more human.”

“On top of [new trainees], my other guys over the years—some have been here up to ten years—every once in a while they get a little rusty, revert back to bad habits, etc.,” Edisis said. “This allows me to keep them honest. And when some new person comes to me and tells me my leads are bad, I say, “let’s go to Ava… you tell me your pitch, I’ll do the same pitch.”

If Edisis significantly outscores them, it becomes evident that lead quality isn’t the issue, but rather all the other factors that go into having a successful call.

“It keeps some honesty between the program and reality,” he said.

People Are Using AI as a Replacement for Search

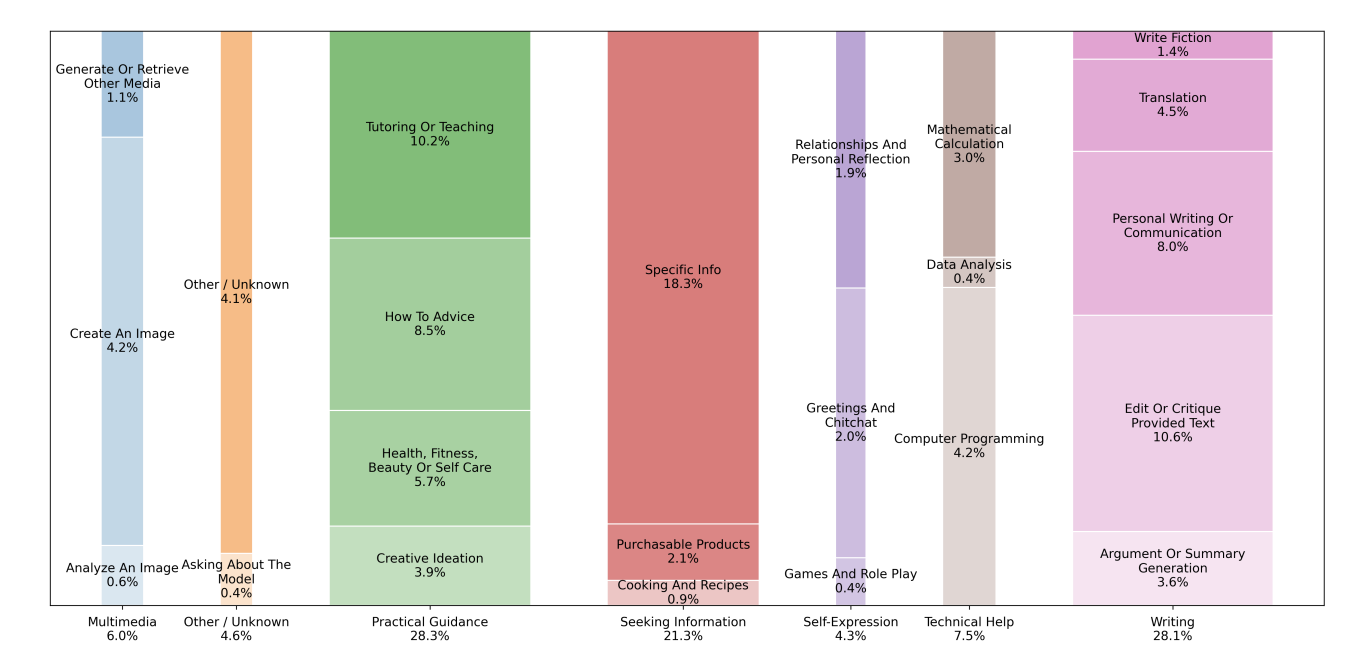

October 6, 2025It used to always be Google when it came to search, but a recent study shared by OpenAI shows that people are using LLMs in a manner that is very similar to how they used Google.

21.3% of ChatGPT interactions, for example, are about seeking information, 28.3% are about practical guidance, and 7.5% are about technical help.

The data was based on 1.1 million sampled conversations between May 15, 2024 and June 26, 2025.

“While users can seek information and advice from traditional web search engines as well as from ChatGPT, the ability to produce writing, software code, spreadsheets, and other digital products distinguishes generative AI from existing technologies,” the report says. “ChatGPT is also more flexible than web search even for traditional applications like Seeking Information and Practical Guidance, because users receive customized responses (e.g., tailored workout plans, new product ideas, ideas for fantasy football team names) that represent newly generated content or novel modification of user-provided content and follow-up requests.”

ChatGPT’s crossover as a search engine is already going one step further. Last week the company announced that it was partnering with Stripe on in-chat checkout.

“The flow is simple: a ChatGPT user asks for product recommendations in the chat,” Stripe said of it. “When they are ready to buy, they are presented with a Stripe-powered checkout inline in the chat.”

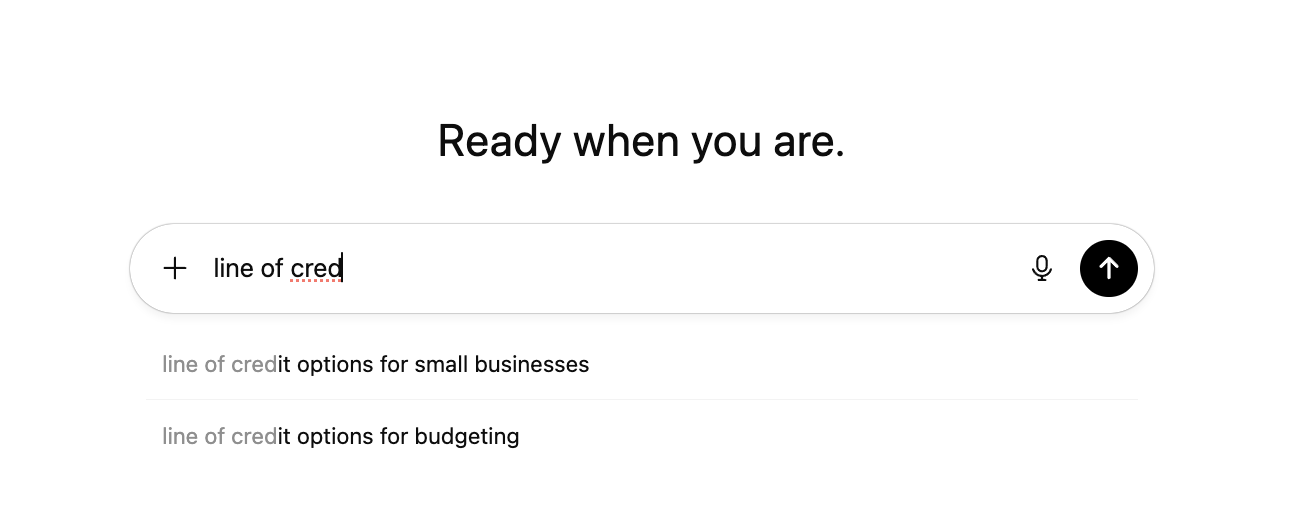

And just as recently, ChatGPT is now also leaning into auto-complete queries, similar to what Google already does.

Typing “line of cred” into a query box, for example, shows “line of credit options for small businesses” as a potential query for the user to choose from.

LendingTree: ‘Small Business Loan Originations Up 40% On Our Platform’

August 1, 2025LendingTree’s small business loan origination volume is up 40% YoY, according to the company’s latest quarterly earnings report.

“In small business, we made a strategic investment to grow our sales force and it has paid off in more business and more efficiency,” said LendingTree CEO Doug Lebda. “I think that small business can be a real growth driver for us.”

Lebda added that profitability had been consistently growing each quarter and that the company was “on a roll.” And part of that is being attributed to staying on top of AI.

“Eighteen months ago, I told our board and our company that we’re going to be an AI first company,” Lebda said. “And today, effectively, all of our employees are using AI in their day jobs, including having enterprise GPT for everyone.”