Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

MoneyThumb Acquired, Ryan Campbell Takes Over as CEO, and What to Expect

August 29, 2024Ryan Campbell will take over as CEO of MoneyThumb as part of the deal announced earlier today. MoneyThumb is being acquired by an investment group led by Iron Creek Partners LLC that includes Main Street Capital Corporation (NYSE: MAIN). Campbell was for a long time MoneyThumb’s EVP of Sales & Marketing. Ralph Mayer, MoneyThumb’s founder, will move on to an advisory role and retain his board seat.

MoneyThumb is widely known in the small business finance industry for two signature products it offers, PDF Insights, which reads and analyzes financial documents, and Thumbprint, which assesses whether documents have been manipulated and could be fraudulent.

The idea for the company, which originated over a decade ago, came to Ralph Mayer when someone had asked him a basic question, could he convert the data in a PDF file?

“I had been in software my entire career. I was an angel investor and I was looking to get into something a little bit different,” Mayer said of the time when the idea for MoneyThumb came to him. “Originally we got started selling software to accountants.”

MoneyThumb soon encountered a field that seemed to handle an unlimited number of PDFs and was ripe for the product they were building. It was the MCA & revenue based financing industry. MoneyThumb has made a name for itself in it ever since.

Ryan Campbell told deBanked that it’s actually quite common for funding companies to be on the receiving end of manipulated bank statements and that about 6% of the documents they analyze on average end up meeting or surpassing the scoring threshold they’ve built to indicate manipulation.

“It happens a whole lot more than what you would think,” Campbell said.

One major trend they’ve noticed is that before covid 90% of fraudulently submitted bank statements did not even have financial columns that reconciled numerically whereas now most fraudulent ones today do. Today’s fraud, because of how good scammers have gotten, may not even be noticeable to the naked eye which is why their technology has become even more important.

Campbell said that as part of the acquisition it will be business as usual with their clients. The company is keeping its name and Iron Creek is going to continue letting them do what they do best. MoneyThumb is used by both funders and ISOs and Campbell is regularly seen on the industry trade show circuit.

“This acquisition underscores MoneyThumb’s proven technology and strong industry demand, and supports our long-term growth objectives,” Campbell said in an official statement. “This partnership marks an exciting milestone for our company and with the support of Iron Creek, we are well-poised to accelerate our growth, continue to deliver exceptional software solutions for our customers and help lenders manage risk and deliver more capital faster to small businesses.”

Media and Trade Associations With Representation at B2B Finance Expo

August 21, 2024Coming to B2B Finance Expo on September 23-24 in Las Vegas? Here are some of the news publishers and trade associations that will have representatives there! (SEE AGENDA HERE)

Small Business Finance Association

National Private Lenders Association

Innovative Lending Platform Association

Registration is still open at: b2bfinexpo.com

A Broker Diversifies With Suite of Value-Adds

August 8, 2024 Like many broker shops these days, Connecticut-based Sharpe Capital is offering more than just a revenue-based financing product. Owned by CEO Brendan Lynch who has been funding deals and boarding credit card processing accounts for more than 15 years, the company is now looking much deeper into business owners’ needs through a whole new set of diagnostic questions like whether or not they have a written will, access to a lawyer, possession of a firearm, or ownership in real estate.

Like many broker shops these days, Connecticut-based Sharpe Capital is offering more than just a revenue-based financing product. Owned by CEO Brendan Lynch who has been funding deals and boarding credit card processing accounts for more than 15 years, the company is now looking much deeper into business owners’ needs through a whole new set of diagnostic questions like whether or not they have a written will, access to a lawyer, possession of a firearm, or ownership in real estate.

The latter on that list, real estate, is becoming more familiar in the small business finance community. Sharpe Capital, for example, added mortgages to its product set about 18 months ago.

“When we talk to anybody on the phone and they start asking questions, ‘oh, what kind of programs do you have? What are the rates?’ now we’ll always say, ‘well, the cheapest way and the most affordable way to get money is, even though rates are higher on mortgages and that stuff right now than they were in the past few years, it’s still the cheapest way.'” Lynch said. “And then what we’ll try to do is explain that it’s going to take a while. ‘How much do you need to get through the next two months while we work this up for you,’ right? Try to get the long term funding going for them and the short term solution all in one.”

More recently, however, the company has added a bundle of services that include things like identity theft protection, legal consultations, will writing, and more. In one example, Lynch said that a merchant disclosed that an IRS audit had slowed down their ability to continue the application process with them and he realized they actually had a solution for that.

“One of the things [this partnered service] covers here is audit services,” Lynch said. “They’ll give you up to 25 hours and walk you through an audit from the IRS. So it was easy. I was like, ‘hey, yeah, let me help you out right now. We signed him up right away.'”

Lynch says that for now, since it’s all still new for them, these value-adds are typically being proposed after the customer onboards for funding but that he’s open to switching it around.

“We’re definitely trying to figure out a way to approach it as the frontend as well,” he said. “The way these leads are being bought and sold so fast and rapidly, you’re fighting with 50-60 different brokers on every deal, you know? … So, we’re really just trying to find something that separates us.”

Lynch argued that in a market where a lot of brokers are essentially offering the same thing, just being personally remembered later on when it comes time for funding again can make all the difference and that being the guy who helped them draft a will for sixty bucks will probably stay fresh in their mind.

“It definitely stands out,” Lynch said. “It definitely opens up conversations where you’re going to get a little more personal with them and build a closer relationship because you’re going to start asking, ‘Are you married?’ Yeah, I know maybe that’s part of people’s sales pitch, but a lot of times we’re just so focused on getting you an offer fast and getting you funded fast, you kind of don’t have time to get into all that, so that afterwards getting to really build the relationship seems to really be working.”

WTF, From Credit Card Processing to Funding Deals

August 6, 2024“My first name is William, my son’s name is Torre and he’s my partner, and our last name is Failla, so WTF was the name of the acronym that we came up with.”

WTF Merchant Services, a real name and double entendre that makes it instantly unforgettable to any client that hears it, has an unusual story. Its CEO Will Failla is a veteran professional poker player that has won more than $6.6 million from tournaments over the course of his career according to a site that tracks players. It’s through friends he made at the card tables that he began to learn about a unique business that some of them were involved in, funding merchants based on their credit card processing sales. After a lot of encouragement and advice over the years, Failla was intrigued enough to look into doing it himself.

WTF Merchant Services, a real name and double entendre that makes it instantly unforgettable to any client that hears it, has an unusual story. Its CEO Will Failla is a veteran professional poker player that has won more than $6.6 million from tournaments over the course of his career according to a site that tracks players. It’s through friends he made at the card tables that he began to learn about a unique business that some of them were involved in, funding merchants based on their credit card processing sales. After a lot of encouragement and advice over the years, Failla was intrigued enough to look into doing it himself.

“I approached my son who was a business major and a finance major out of Hofstra and I said to him, ‘you’re graduating any day now so why don’t we do some diligence, look into this business and see what you think.'”

His son, Torre, who is now the company’s CFO, signaled his approval so long as they paced themselves and mastered the most fundamental component of it first, the credit card processing side of the business. Thus 2021 kickstarted WTF Merchant Services as a shop on Long Island that focused entirely on boarding merchant accounts. They started by approaching their friends, family, and contacts and then expanded it to where they had a referral incentive program and continued to acquire more and more accounts.

The most attractive part of the business to them is the residual revenue component to it. “That’s the greatest. That’s what made us get into it because now we get paid every month. As long as you keep that customer, you get paid every month,” Failla explained.

And keeping those clients means providing great customer service, which he said they’ve placed a strong emphasis on. They’ve also gotten a firsthand look at the financial trends of the various businesses they’ve worked with, something they figured would come in handy for when they were ready to take the next step.

“We didn’t do an MCA deal until the beginning of this year,” Failla said. “We really wanted to learn the business in and out, and then we were just an ISO.”

The evolution from credit card processing to funding is straight out of the old MCA playbook of the mid-2000s, but with a notable difference here, they haven’t abandoned their roots. Unlike many modern funding ISOs who focus entirely on commissions paid out on funding, WTF is requiring their funding clients to switch their merchant accounts to them, assuming it’s a business that processes cards. And if they can do the funding deal on a split of the processing, all the better.

The evolution from credit card processing to funding is straight out of the old MCA playbook of the mid-2000s, but with a notable difference here, they haven’t abandoned their roots. Unlike many modern funding ISOs who focus entirely on commissions paid out on funding, WTF is requiring their funding clients to switch their merchant accounts to them, assuming it’s a business that processes cards. And if they can do the funding deal on a split of the processing, all the better.

“When you do the split, it’s so much easier because you take, let’s say 15 or 20% or whatever the merchant can handle at the time,” Failla said. “It’s just so much better of a direction to get paid because it doesn’t hit their bank, it doesn’t hurt them as much. When they see it coming out daily like that, it’s a little different. When it comes out of the credit cards it’s just early and it helps a lot. Mindset changes.”

The company’s traditional approach has already attracted the attention of some of their peers in the industry who like the idea of residual income but don’t have the time or the patience to worry about merchant accouts.

“We have different MCA offices that we actually do this with already,” Failla said. “We do all their credit card processing. We handle all the back-end. We handle all the front-end. All they do is give us the referral and they become what we call a referral partner, and they get paid every single month as long as we keep the account.”

Will was sure to give credit to those that have helped shorten his learning curve along the way. He has since discovered that others in the poker scene are also in the same business as he and it’s created a valuable community. WTF even has a poker table in its office as a sort of tribute to his background which he has not actually retired from. The Hendon Mob poker tracker states that Will recently placed 259th out of 10,112 players in the World Series of Poker in Las Vegas earlier this month. Meanwhile, the company name itself, a bold strategy, seems to be working out so far.

“If you look under our logo, it says our names right underneath it. William, Torre Failla, and listen there’s going to be some pushback, but the amount of pushback we’ve had is so minimal that I think it’s worth it, and we’re going to stick with it as long as we can.”

More About OppFi’s Big Equity Investment in Bitty

August 1, 2024 Publicly-traded OppFi announced it has acquired a 35% stake in Bitty Advance for a cash payment of $15.25M and stock valued at $2.7M. OppFi says this was a 6x valuation multiple based on Bitty’s $8.5M of adjusted net income for the trailing 12 months ending March 31, 2024. Bitty originated approximately $165M in revenue based financing deals in 2023.

Publicly-traded OppFi announced it has acquired a 35% stake in Bitty Advance for a cash payment of $15.25M and stock valued at $2.7M. OppFi says this was a 6x valuation multiple based on Bitty’s $8.5M of adjusted net income for the trailing 12 months ending March 31, 2024. Bitty originated approximately $165M in revenue based financing deals in 2023.

The transaction enables OppFi, already well known in consumer lending, to enter the small business financing market. OppFi cited Bitty’s operating metrics being bolstered by an industry experienced CEO (Craig Hecker) and an established team. Bitty has funded $420M to 29,000+ merchants since inception. Bitty will remain majority controlled by Hecker. OppFi has the option to acquire a majority stake in the company in 2027. OppFi has a current market cap of $389M and more than 400 employees.

“We’re excited by this acquisition, as we believe Bitty provides the foundation for OppFi’s new vertical in small business financing,” said Todd Schwartz, Chief Executive Officer and Executive Chairman of OppFi. “Bitty facilitates credit access to small businesses that are not served by traditional banks, aligning with our mission to facilitate credit access to everyday Americans. Small business financing is increasingly being originated online, and we believe Bitty’s digital platform is well-positioned to capture this growth. We look forward to working with Craig and his team to further scale Bitty with OppFi’s data analytics, automation, and marketing expertise.”

Bitty is well-known to deBanked. Hecker’s investment in Bitty Advance (which led to an eventual takeover) was first covered in early 2020. Hecker has been known to the Editor through the industry for even longer than that, since before deBanked’s inception in 2010. Hecker sat for an on-camera interview in January and has been a signature sponsor of both Broker Fair, deBanked CONNECT, and the upcoming B2B Finance Expo.

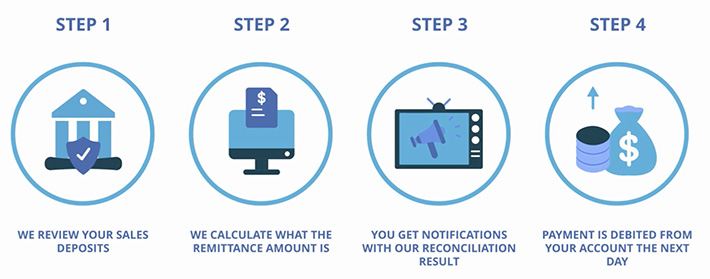

Real-time Reconciliations on Revenue Based Finance Deals?

June 25, 2024In the finance world, taking a percentage of a merchant’s sales at the time a sale is consummated is called a split. It’s how revenue based financing often works when the purchased future receivables are card-based. When it’s all revenue, funding providers often rely on a combination of ACH debits and reconciliations, the frequency of which are governed by the contract. On some big e-commerce platforms, like Walmart Marketplace, for example, sales data is monitored in real-time and the appropriate split is debited out from the merchant’s bank account the next day. Some refer to this as a real-time reconciliation.

Real-time reconciliations have been attempted outside of e-commerce ever since Merchant Cash and Capital aka BizFi (RIP) pioneered this 15 years ago, but it was a manual process riddled with challenges that would hardly hold up in today’s technological world. In 2021, revenue based financing provider FundKite introduced its own system, one that was documented by deBanked at the time.

Back then, FundKite CEO Alex Shvarts said, “This product [where debits vary daily based upon true sales] works better for merchants, it works better for portfolios, if you’re actually reconciling and pulling what you’re supposed to, and not what you’re anticipating.”

Three years later, Shvarts still feels the same way and told deBanked that his daily reconciliation method has been a success and is now a leading driver of its business.

“In order to reconcile we must have access to the merchant bank accounts,” Shvarts said. “We use priority technology to do the reconciliation after we have the data. We use a combination of live Logins, Plaid, Decision logic and another piece of code we wrote. Merchants are automatically notified of the reconciliation and adjustment to the payments before we debit the accounts.”

The company touts this system as its edge on its homepage.

“Payments are based on sales, offering protection during slower periods or when no sales occur,” the site says.

“Something’s Happened” – How a funding platform weathered a shocking crisis and is flourishing

June 21, 2024 “[The CEO] called me just before seven in the morning…but [he] would never call me at that hour, so I picked up the phone and he goes ‘Paul, something’s happened, it’s very serious.’ and I’ll never forget, he says ‘you need to take care of our company.'”

“[The CEO] called me just before seven in the morning…but [he] would never call me at that hour, so I picked up the phone and he goes ‘Paul, something’s happened, it’s very serious.’ and I’ll never forget, he says ‘you need to take care of our company.'”

That’s how Paul Vega, Senior Operations Manager at Funders App, retold the story of a phone call he received in June 2021 that would shake up everything about the small business finance company he was working at. At the time, the business was known as 24 Capital, Funders App was a platform they were developing internally, and Mark Allayev who was the CEO, was riding high from having weathered all the uncertainties of startup life and the Covid era. With Vega having played a key role in that success and the business running smoothly, Allayev felt he had earned a much needed vacation and traveled to Europe with some friends.

“And it was just five days,” Allayev said. “But one of our friends had an event in New York and we just had to come back, and the only flight to New York was with a layover in Germany, in Frankfurt. So we got to flying and it was supposed to be a two hour layover in Germany, but came out to be an eight month layover in Germany.”

That’s when the fun and life as he knew it came to a grinding halt. The German authorities never let him get on a plane to the United States. Instead, he was placed under arrest when his name registered as a match with Interpol. Despite his insistence that it was all some misunderstanding, he was directed to a local jail and told he’d soon be extradited to the country that wanted him, Russia. Allayev, then 31 years old, who had been born in Soviet-era Tajikistan and at the time enjoyed dual American and Russian citizenship, had not been to Russia at all since he moved to the United States in 2015. He had, however, previously worked at a family business in Russia as a youngster that found itself ensnared in the unique political environment. Allayev said that his family’s business had been the victim of fabricated allegations and they had left as a result. As an American citizen he had enjoyed international travel for years without issue, and he had almost forgotten about it all. That is until this moment in June 2021 that would change his whole world view and send his family scrambling to save him. While those efforts would eventually enlist help from Democratic Reps. Debbie Wasserman Schultz of Florida and Greg Meeks of New York, Allayev was swiftly cut off from being able to manage his business and was no longer able to contact Paul Vega directly.

“I was aware of what had happened years ago with him and his family because he was transparent with me from the first day we met,” Vega said. That fateful phone call he received that morning lasted all of 3 minutes. “I was like, Okay, I guess this is what’s happening,” Vega recalled.

For Vega, the realization hit that the company had nearly two dozen employees at the time, all of whom depended on it for their livelihood, and all of whom were probably going to question the circumstances their boss was in. Nevertheless, crisis management is how Vega had been introduced to the business from the beginning. Vega started at 24 Capital in January 2020 with about six years of industry experience under his belt, with the objective of completely revamping the underwriting process.

“I think it was actually perfect timing, I think it was meant to happen that way,” Vega said. For instance, family members living across the globe had tipped him off that Covid was going to be much worse than the oblivious American media was making it out to be. Vega was also operating out of an office in New York City where a potential doomsday scenario was a lot easier to imagine than where Allayev sat in South Florida.

“When I first expressed this idea [to Allayev] of the possibility of the universe being shut down, I know that Mark was questioning whether he had made the right decision in bringing me on because here I am brand new to the company and I’m telling him that, ‘hey, the US is going to shut down,'” Vega said. Despite having come across as alarmist, Vega felt that it was better to act on his conviction and plan for the impossible.

“Behind Mark’s back I started to research the idea of remote work, and nobody knew what remote work was back then,” he said. Vega proceeded to set up staff with home computers and began testing out software they had never used before.

“By the time they shut down the city, we were well situated to just literally flip a switch and be able to process and run the business from home,” he said.

And ready they were because not only did the company never stop funding but it also never let anyone from the company go during that time. Through it all Vega and Allayev formed a really trusting relationship with each other, the kind that would only make survival of the company possible once Allayev was detained in Germany the following year.

As days turned into weeks and weeks into months, Allayev’s extradition to Russia seemed inevitable despite a growing lobbying effort to free him. Then Russia invaded Ukraine. Once that happened, the politics in Europe changed, and Allayev was suddenly freed in March 2022 and put on a plane back to the United States. The emotional journey and the circumstances that enabled his return became a big news story in the newspapers, one of many about people whose fortunes changed for better or worse as a result of the war.

Once he was reunited with family and had the opportunity to acclimate back into life, he looked toward his business, which he now had a newfound perspective on. “Before, all I cared about was just working and just living my own life,” Allayev said. “So I think what changed is me understanding that probably your family’s the most important part and you need to focus and spend more time with your parents, your siblings, all your loved ones. I think that’s the thing that really changed my mindset.”

Of course, it wasn’t as if this perspective was shaped by losing his business in the process, because it had somehow managed to continue running like normal during the eight months he was away, thanks to Vega. Even the employees stayed on, as everybody stood in supportive solidarity with Allayev.

“So one thing that I learned that was funny when I came back is that the company could be run without me,” Allayev said. “And I think that Paul and all the other team members did an amazing job, keeping everything in place and keeping the funding amounts pretty decent.”

Today, the brand Allayev and Vega are under is known as Symplifi Capital. The company’s internal infrastructure platform has also blossomed into its own publicly licenseable service known as Funders App for companies that want to be their own funders. Allayev says that Funders App provides technology, underwriting services, collections, accounting, servicing, distribution of funds, contracts, white label services, and more. It can be customized to provide just what one needs. A sizable number of companies are already using it, to the point where last year Funders App announced it had collectively originated $500M in funding to small businesses since inception.

“I think there’s so many talented kids and young people that have the vision to create their own companies but they just have absolutely no help and no backup,” Allayev said, “and this is what we want to create with funders. We want to help those people, we want to get them in, train them, help them, and provide them with the right tools, the infrastructure, and even with leverage, even the money because you need capital to become a funder.”

Allayev drew some of this inspiration from how he started in the business in late 2016, when he talked to numerous companies about what they could provide to help him launch his business and felt like nobody could provide all the pieces. As for the trajectory forward, their eyes are on efficiencies and growth.

“As you know speed is kind of the name of the game here,” Vega said. “If the typical lending house is taking three to four hours to put out an offer, make a decision, ask for additional information, our goal is to have a file from submission to funding in that three-to-four hour timeline where most people are just getting an answer back to the ISO. So we’re hoping to have the merchant funded in that timeline. And that’s going to create just a huge competitive advantage for us.”

That’s the kind of thing they’re working on today. The backdrop with what happened to Allayev is now just part of the company’s founding story. For Vega, there was never any question that it wouldn’t work out. Referencing the early months of Covid when companies were doing mass layoffs, he expected that Allayev would ultimately, through no fault of his own, do the same.

“[Allayev’s] the only person that I know in the whole industry that actually said, ‘I’m not doing that, I’m keeping everybody’ and kept his word,” Vega said. “That day he sold me. That’s a big portion of the reason why I have so much trust in him, because he’s a man of his word.”

SellersFi Surpasses $1B in Loans Since Inception, Experiences Success Through E-Commerce Funding

June 14, 2024The timing of it all was fortuitous for SellersFi. When the company announced in January that it had secured a partnership with Amazon to provide eligible Amazon sellers with access to credit lines, it was clear that its fresh equity raise and credit facility of up to $300 million were going to be put to use. SellersFi wasn’t the only partner, however, and Amazon still did most of the lending to its own sellers directly, a business it had been in for more than a decade, but it was still a big relationship to have. But then it got better. In March, Amazon announced that it would end its direct lending program and rely entirely on its partners instead. For SellersFi that meant it would have the opportunity to service even more sellers on the platform than before. Since then, SellersFi has quietly surpassed $1 billion in loans since inception.

“What we are seeing now is less competition,” said Ricardo Pero, CEO of SellersFi, in a call with deBanked. He partially attributed that to the current interest rate environment which has impacted those with small margins. SellersFi, however, has experienced a lot of success. The company knows the e-commerce space particularly well, the only space it operates in, since its the only US lending platform also approved as a payment service provider member for Amazon. They started their relationship with Amazon as a service provider 3 years ago. While Pero said they have seen “nothing that points to a recession,” their experience suggests that even if one were to happen in the future, consumers would react by seeking out bargains on e-commerce platforms, reinforcing their position as the niche to be in. As readers may recall, a flight to e-commerce is also what happened during the pandemic.

E-commerce, however, is a broad umbrella, and Amazon is not alone in the universe. Millions of businesses rely on various platforms for e-commerce from basic templates with API connections to Shopify and more. Even big box brick and mortar retailers are waking up and rapidly inching their way into e-commerce. Walmart is just one example, which not only accommodates individual sellers on its platform but also offers merchant cash advances to them.

“The competitive landscape is changing for our clients,” Pero said. Pero added that they know what’s going on because they talk to these clients all the time and that even in the e-commerce business there are person-to-person relationships. “Customers mention their account managers by name,” Pero said. “We have a reputation as a partner to these merchants.”

One trend they’ve noticed over the last year or so is their strategy towards borrowing. While merchants have always typically used funds for things like advertising or inventory, the previous low rate environment enabled behavior where merchants could borrow first and then figure out how to spend the funds second whereas now that rates are higher there is a lot more of a deliberative approach to precisely how much they should get and what it will be used for in advance. It’s something they see all the time now and agree with. “You need to plan,” Pero said.