Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

A Glimpse at Simply Funding

January 14, 2025 In around 2018 Jacob Kleinberger began calling merchants for a well known small business finance brokerage—a job he not only enjoyed but one that sparked his curiosity. “I always wanted to understand what my funders were doing,” Kleinberger says. He frequently asked questions to learn how decisions were being made across the board.

In around 2018 Jacob Kleinberger began calling merchants for a well known small business finance brokerage—a job he not only enjoyed but one that sparked his curiosity. “I always wanted to understand what my funders were doing,” Kleinberger says. He frequently asked questions to learn how decisions were being made across the board.

Though he worked closely with funders, being on the sales side didn’t give him the full picture. That changed in 2021 when an opportunity arose to join Simply Funding, a direct funder, as a partner. Today, he serves as Head of Operations.Transitioning from broker to funder was an eye-opener, leading Kleinberger to half-jokingly call the funders he used to work with to apologize for the challenges he had unwittingly created. Despite the learning curve, Kleinberger hit the ground running. Simply Funding, founded in 2017 by Bernard Mittelman, was a relatively small operation when he joined, but his mission was to help it grow. “We more than doubled the following year in funding and more than doubled the year after that,” Kleinberger says, reflecting the impact he’s been able to have with the team, which he’s said has been crucial to the success.

“We’re all a team, all here to show off each other’s strong points,” he says. For instance, the company already had a really good core foundation and underwriter in place when he got there.

The company describes itself as an A/B paper shop, with the majority of its revenue-based financing deals involving weekly payments, though they do daily payments as well. They also offer merchant processing splits.

Now a 28-person company, Simply Funding was originally located in Manhattan’s financial district but has since relocated to Jersey City. Kleinberger recalls the transition vividly, flying straight from the deBanked CONNECT Miami conference in 2023 to the new office to assemble all the furniture—an ordeal that lasted nearly 24 hours straight. One benefit of the move, he says, is access to a large talent pool in the area. But of course, it had to be accessible for the current team.

“A very big part [of the decision] was I had really good staff, and how would my staff come to work?” he says, since they make the whole operation hum. As a New York native from north of the city, Kleinberger is a commuter himself. The office now is just across the street from the PATH train station on the Hudson River. One can see the Simply team in person in the corporate high-rise there if they drop by.

“A very big part [of the decision] was I had really good staff, and how would my staff come to work?” he says, since they make the whole operation hum. As a New York native from north of the city, Kleinberger is a commuter himself. The office now is just across the street from the PATH train station on the Hudson River. One can see the Simply team in person in the corporate high-rise there if they drop by.

When asked about the importance of security at Simply, Kleinberger is unequivocal: “It’s the most important.” The company takes no chances with data access, even to the extent that Kleinberger himself refuses to store work-related information on a laptop. He also emphasizes the need for clear, unambiguous rules in business operations to ensure everyone understands expectations and outcomes.

The company has no inside sales force, so Kleinberger gets a thrill when an ISO seeks his help with merchant communication—it reminds him of his early days. However, he remains acutely aware that, since it’s the company’s funds on the line, transparency and directness with customers are non-negotiable. From his perspective, some brokers in the industry walk a fine ethical line, and he and the Simply crew are determined to ensure things are done the right way.

“I do feel like there needs to be something to help make brokers accountable,” he says. Despite the challenges, Kleinberger remains optimistic about the future and is excited about what lies ahead as Simply Funding continues to grow.

“I think 2025 is going to be a sick year,” he says.

Recent Developments at Mulligan Funding

January 9, 2025 Last month, Mulligan Funding announced the closing of a second asset-backed securitization (ABS) totaling $120M and expandable up to $500 million. Business has been great since.

Last month, Mulligan Funding announced the closing of a second asset-backed securitization (ABS) totaling $120M and expandable up to $500 million. Business has been great since.

According to a representative of Mulligan, “December was the best month we’ve ever had as a company, capping off our best year since inception. And a large measure of that success is owed to the extraordinary community of ISO partners that we work with – and the incredible relationships we’ve been able to develop with them.”

As part of that, Mulligan Funding has made some changes to continue its success, an explanation of which is quoted here:

“We are continually looking for ways in which to improve our relationships and the level of service we’re able to offer them. And so, in order to continue to improve our level of service and improve the depth of our relationships with our partners, we decided to implement a restructure of our ISO Team and the way in which we manage our partner relationships.

We have established for the first time a regional segmentation of our ISO partners. This has allowed us to rationalize our ISO groupings, and to create smaller, more focused multi-person teams purely dedicated to the relationships in their particular region.

Each team will consist of people with different levels of seniority and very specific roles. Some will be dedicated purely to looking after the relationship at a strategic level; and others will be tasked with handling the transactional details of day-to-day operations.

This regional focus will allow these teams to develop much deeper relationships at all levels of the partner’s business, and to spend more time in front of these partners, developing a better understanding of their needs and wants – something we have historically found challenging, being on the West Coast.”

– Mulligan Funding

Top Stories of 2024 vs 2014

December 30, 2024A lot happened in 2024, but rather than just rehash it all out, let’s revisit the world of 10 years ago. In 2014, both OnDeck and LendingClub went public, Bitcoin landed in the mainstream, Square started funding, securitizations in the industry commenced, and the world was still not totally sold on the concept of MCA. Oh how things changed!

BriteCap Financial Ramps Up Team, Ready For Growth

December 20, 2024 The stream of announcements coming out of BriteCap Financial garnered notice. It started with news of a $150M credit facility back in August, followed by announcements of a new CEO, CFO, CCO, VPs, and more. The new CEO, Richard Henderson, whose CV includes previous roles at CAN Capital, Marlin Capital Solutions, and Direct Capital, told deBanked that the company wanted to have the right team in place to carefully grow the business. BriteCap, which is part of the North Mill family of companies, offers attractive term loans to small businesses.

The stream of announcements coming out of BriteCap Financial garnered notice. It started with news of a $150M credit facility back in August, followed by announcements of a new CEO, CFO, CCO, VPs, and more. The new CEO, Richard Henderson, whose CV includes previous roles at CAN Capital, Marlin Capital Solutions, and Direct Capital, told deBanked that the company wanted to have the right team in place to carefully grow the business. BriteCap, which is part of the North Mill family of companies, offers attractive term loans to small businesses.

As part of the plan, the company is looking to add not just new brokers but the right brokers, especially given the upstream programs they offer to merchants. “We’re being very selective on who we onboard,” said Henderson. “We’re trying to make sure that we’ll use that to get to scale, but also to build powerful relationships with those brokers where it’s a true partnership.”

BriteCap has developed an online checkout system to streamline the funding process. It can be configured to work with however the broker is used to working. They’ve focused a lot on the mobile experience so that a merchant need not even be in front of a computer to go through it.

One notable advantage to BriteCap is precisely that affiliation with the North Mill family because it opens up the possibility of not just working capital as a solution but also equipment finance. According to Henderson, the potential crossover between the products works well especially when the deals have been originated in the right context. That context includes the best practices and professionalism that equipment finance brokers typically operate within.

Among the C-suite executives to recently join BriteCap are Pushkar Choudhuri as Chief Financial Officer and David Lafferty as Chief Credit Officer. The timing of everything aligns with the firm’s economic sentiments. Henderson said that he believes optimism is higher now and growing.

“…generally speaking, we’ve seen demand picking up and we have a pretty bullish view on the economy moving forward,” he said. “I think we’re entering into a very good time in our space.”

Smaller Funder? How to Get Fast Tracked With Big Investors

December 4, 2024Looking for big money? As a smaller funder your simple financial reports might not cut it when it comes to big investors. In fact, it’s a complaint frequently made by investment bankers and institutional funds looking to get capital deployed in the revenue-based financing space.

“Smaller originators face three key hurdles: first, the lack of institutional-grade portfolio performance and consistency; second, limited data operations and analytics capabilities; and third, a shortage of affordable resources and expertise to close these gaps and engage effectively with capital markets,” said Tomo Matsuo, Managing Partner of AdvanceIQ.ai., “AdvanceIQ.ai was launched to address these challenges head-on through tailored solutions like our new Portfolio Pulse product.”

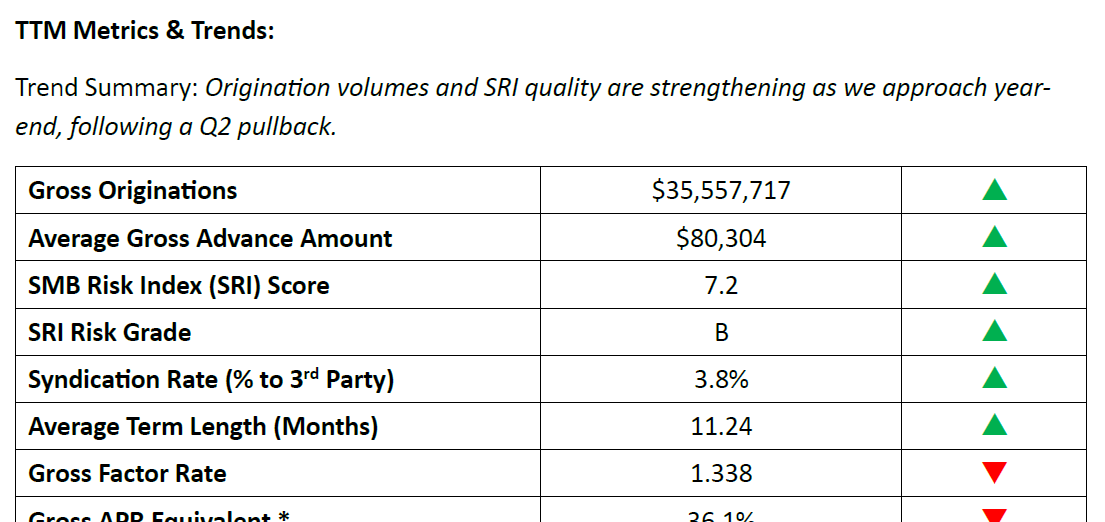

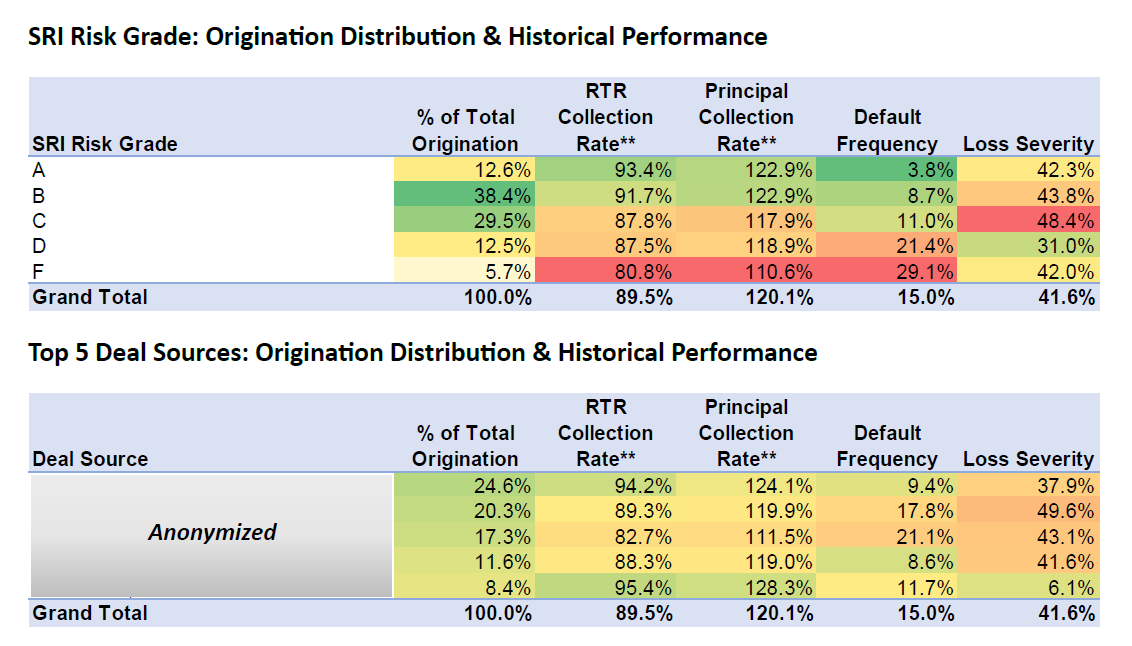

The Portfolio Pulse is a simple yet robust tear-sheet product that delivers a high-level, third-party validated snapshot of portfolio performance. Designed as a cost-effective tool, it helps funders build credibility and engage institutional investors with confidence. Seamlessly integrating with most industry CRMs, it generates investor-ready metrics tailored for early-stage conversations, enhancing transparency and trust.

But Portfolio Pulse is just one piece of AdvanceIQ.ai’s broader suite of tools. From risk scoring and intelligent lead routing to dynamic portfolio analytics, AdvanceIQ.ai equips funders with the insights and resources to scale efficiently while building investor confidence. These offerings include tools like the SMB Risk Index (SRI), a proprietary scoring system designed for the SMB AltLending sector to predict and enhance asset performance.

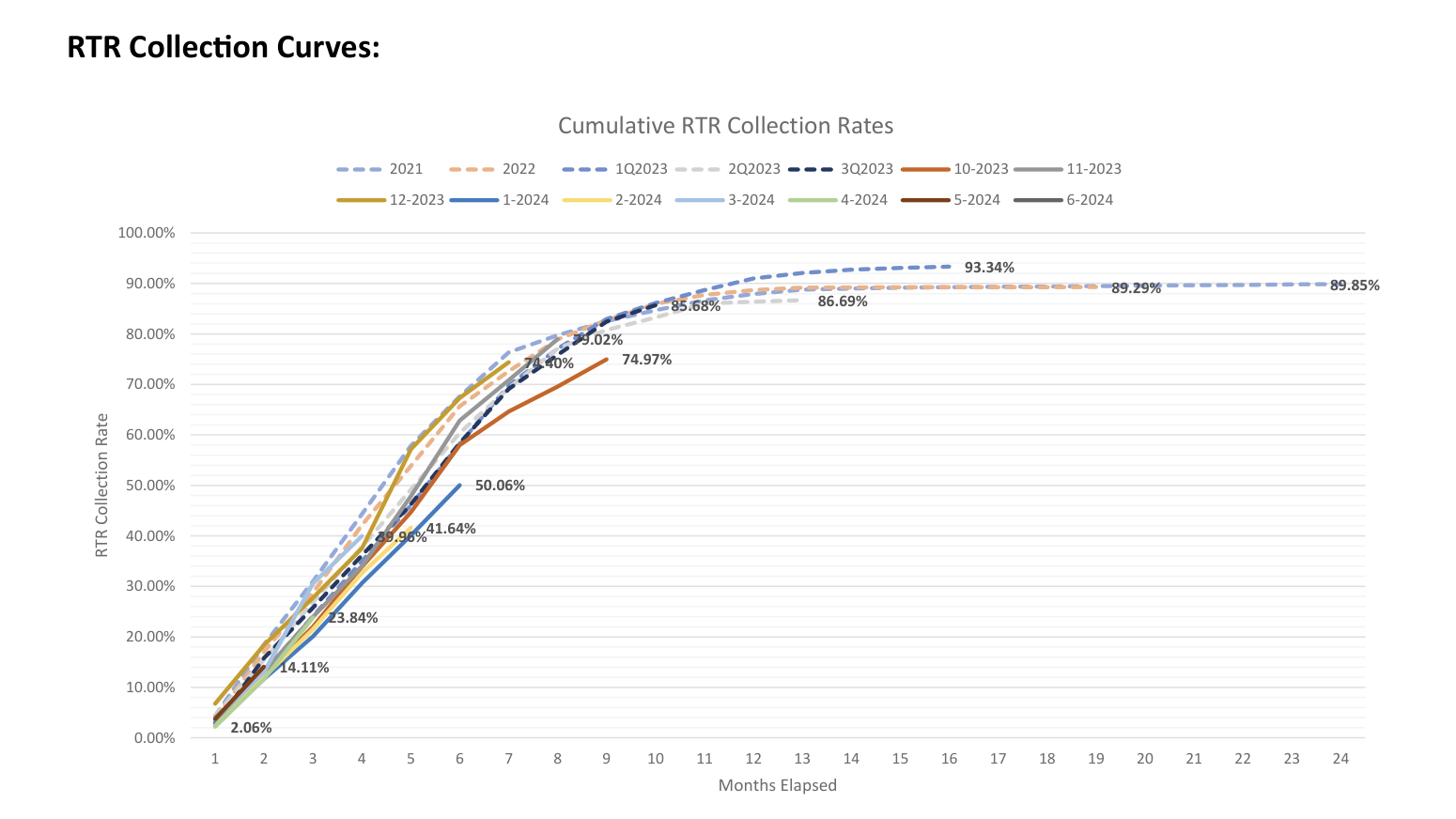

Excerpts from Portfolio Pulse:

• Trailing twelve-month (TTM) origination metrics and performance trends.

• Distribution and performance insights segmented by key attributes, including the proprietary SMB Risk Index (SRI).

• Historical repayment trends via collection curve analysis.

“High-quality reporting is an essential first step for smaller funders to break into institutional markets,” Matsuo noted. “Our goal is to provide the transparency and insights that empower them to succeed.”

With deep experience in the SMB AltLending space, Matsuo is no stranger to the challenges funders face. “Having been involved in raising and managing hundreds of millions of dollars in both debt and equity, I’ve seen how difficult it can be for smaller originators to stand out. AdvanceIQ.ai’s offerings are designed to remove those barriers and position them for growth.”

CAFE’s Fall 2024 Accelerator Cohort a Success

November 25, 2024 deBanked attended and sponsored the final demo day of CAFE’s Fall 2024 Accelerator Cohort. CAFE, as previously profiled, is the non-profit Center for Advancing Financial Equity. The six members of the Cohort were Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm.

deBanked attended and sponsored the final demo day of CAFE’s Fall 2024 Accelerator Cohort. CAFE, as previously profiled, is the non-profit Center for Advancing Financial Equity. The six members of the Cohort were Carvertise, GivingCredit, Kredit Academy, Odynn, Salus, and Prismm.

As previously stated, the bi-annual accelerator aims to identify, support and grow extraordinary financial accelerated technologies and innovations. Hundreds of companies apply but only six get selected for each cohort.

The demo day took place inside the Fintech Innovation Hub, situated on University of Delaware’s STAR campus. It was a major success.

To learn more about CAFE, visit: https://ftcafe.org/

Are You The Top Broker?!

November 21, 2024

Broker Battle returns on February 20, 2025 at deBanked CONNECT MIAMI. The competition, now the 2nd ever after last year’s very successful launch, is back with an improved format that allows for almost any qualified broker the opportunity to be tested LIVE in person. Broker Battle TWO will also have 3 separate broker categories versus last year’s catch-all. Those categories are Revenue Based Finance, SBA Lending, and Equipment Financing.

All competing brokers will be vetted, tested, and scored through very short judging rounds on the showcase floor. The two top scores from each category will actually compete on stage for the championship.

That means that as opposed to last year’s 6 total contestants and 7 separate battles on stage, this year’s competition could feasibly manage up to 100 contestants for which there will only be 3 total battles on stage (each being a championship). The format allows for more brokers to prove themselves in person while reducing total stage time for the final grand performance.

Each broker will win a cash prize and the distinction of being Top Broker (in their category). To be eligible for entry, you must be an active broker with good ethics and a positive reputation. You must also be registered to attend deBanked CONNECT MIAMI where it will take place and enter yourself in the battle itself here.

Broker Battle intends to foster best practices.

Rewarding Loyalty in Revenue Based Finance

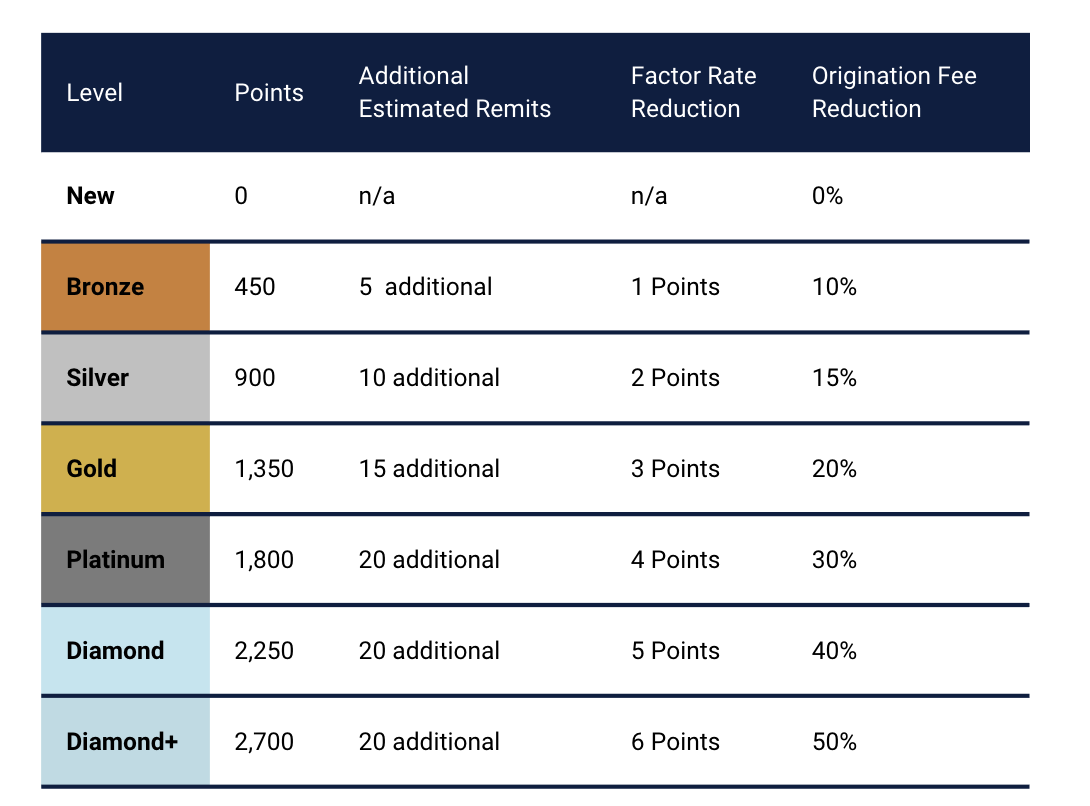

November 13, 2024 Everyone’s heard the pitch that if a deal goes well there could be better terms on the next one, but how much better are we talking about precisely? Well, after conducting an internal study, Pennsylvania-based Funding Metrics decided to actually codify incentives for success into a fully fledged loyalty rewards program that enables merchants to get a precise factor rate reduction, origination fee discount, and additional estimated remittances on subsequent advances.

Everyone’s heard the pitch that if a deal goes well there could be better terms on the next one, but how much better are we talking about precisely? Well, after conducting an internal study, Pennsylvania-based Funding Metrics decided to actually codify incentives for success into a fully fledged loyalty rewards program that enables merchants to get a precise factor rate reduction, origination fee discount, and additional estimated remittances on subsequent advances.

“Early 2023 we took a deep dive into our customer experience and how it directly correlated to merchant retention,” said Melissa Flagg, Vice President of Operations for Funding Metrics. “We listened to the pain points our ISOs shared, with customer retention always driving the conversation. Most ISOs we spoke with seemed to face similar retention challenges and were coming up short with solutions.”

The challenge is that merchants tend to shop around on subsequent deals even if they are happy with what they got the first time. The loyalty program was the eventual outcome of what they learned and it’s open to merchants funded by Lendini and Quick Fix Capital. As Flagg tells it, there are three ways for merchants to accrue points. First, points simply for opting in, which they must do in order to take advantage of it. Second, additional points for each 1% they remit toward the purchased amount, and third, points for each renewal. There are six total milestones that range from Bronze Level to Diamond+ Level. While the tiers, conditions, and corresponding discounts are published right on their website, merchants can easily track their points through the Funding Metrics mobile app.

“There’s no need for a redemption email or request,” said Flagg. “Points don’t deduct, they continually accrue as long as merchants continue to remit, and discounts automatically associated with the loyalty level apply on their next offer.”

She added that it’s quickly been recognized as a great way to incentivize a merchant not to shop around. It’s also been used to secure a renewal or win back an old customer that had left. This logically helps the ISOs involved.

Most readers are already familiar with the Lendini brand through their constant mix of on- and offline marketing. Members of their team usually show up in large numbers at major industry events, for example. Flagg said that 2024 has been a big year for the company. “In Q2, we successfully launched Instant Offers, and we’re proud to report that we’re now averaging a turnaround time of under 5 minutes for offers up to $75,000,” she said. Their new mobile app, while still in beta, allows merchants to track offers, remittances, and engage with the Resolutions Team.

“Over the past two years, we’ve prioritized elevating the customer experience by creating accessible tools that empower merchants to navigate the financing process with ease and transparency,” Flagg said. “This is only the beginning. Funding Metrics is dedicated to continuously enhancing these experiences that put merchants in greater control of their business financing and making every step from offer to origination as seamless as possible.”