Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

On Long Island? You Might See Signs

March 26, 2024

Billboards for Broker Fair 2024 have gone up across several Long Island towns this past week, including locations in Glen Cove, Syosset, Westbury, Bay Shore, and Valley Stream. The conference, built specifically around a broad range of commercial finance brokers, will take place on May 20 in New York City. Long Island is among the largest geographical employers of brokers in the United States.

Broker Fair attendees can expect to learn from industry pro Peter Ribeiro, meet a wide range of funders/lenders & vendors, pitch their deals, and find out what they need to be doing to remain compliant and become successful.

Broker Fair 2024 will take place at the Metropolitan Pavilion in New York City. Brokers pay the lowest price for entry. There is also a pre-show party the night before on May 19th at a Lounge called Somewhere Nowhere NYC (yes that’s really the name!).

If you’re a broker, Broker Fair 2024 is an event you cannot miss!

Let’s Hop on a 5 Minute Call

February 28, 2024There’s a fantastic meme account on X where “Hunter” spreads the comedic gospel of cold calling one’s way to becoming a billionaire. Hunter suggests that true sales people take freezing cold showers, tip their landlords for sub-par living arrangements as respect for creating optical conditions to grind, and to make cold calls every day, every night, during holidays, and while being seated in an ice bath at the Cheesecake Factory.

We need to teach cold calling in elementary school pic.twitter.com/fwqaaG2uA2

— Hunter (Let's hop on a quick 5 min call) (@huntercoldcalls) February 22, 2024

We all know that cold showers help you become a better cold caller

But to unlock your true potential, you need to cold shower while cold calling

Introducing, the next generation of call centers pic.twitter.com/vrTwI7b094

— Hunter (Let's hop on a quick 5 min call) (@huntercoldcalls) February 21, 2024

A national cell phone outage just destroyed my business, my life, and the entire world

Thousands of my cold calls went unanswered today because the national cell phone network wasn't working

I would have helped each and every one of those prospects improve their lives

And I…

— Hunter (Let's hop on a quick 5 min call) (@huntercoldcalls) February 22, 2024

The account, which can sometimes be found trolling celebrities by asking them to hop on a quick 5 minute call in the comments, is likely relatable to any salesperson that’s experienced the rigors of the hustle. For instance, I can recall one particular day in 2015 when I was making cold calls from a waterfront skyscraper in Jersey City when a plane flew by the window and then LANDED right there in the Hudson River. What to do? Go look? Not possible. Had to make more cold calls!

That plane, of course, was flown by Captain Sully Sullenberger, of which the feat of landing there became known as the Miracle on the Hudson. I am proud to say that because I ignored all of it and continued to make cold calls while it was happening that I am now worth $463 trillion as a result.

My Real Estate Was Turned into an NFT. I Used that NFT as Collateral for a Loan.

February 25, 2024 Ooops, I did it again. I bought an NFT that grants me ownership of real land in Arizona in the same manner that I previously bought land in California. But this time I went a step further, I used it as collateral for a loan.

Ooops, I did it again. I bought an NFT that grants me ownership of real land in Arizona in the same manner that I previously bought land in California. But this time I went a step further, I used it as collateral for a loan.

Thanks to a proptech company called Fabrica, the owner of a plot of undeveloped land in rural Sun Valley, AZ transferred the rights to a trust for which control is governed by whomever owns the corresponding NFT. Long story short I bought that NFT. The difference between this NFT and say some digital collectible flavor of the month is that the land has some actual value in the real world. It’s not dependent on the blockchain for its worth and I can go to Sun Valley and build something there if I wanted. But with ownership governed by the NFT, I can also do something that might be a little bit more difficult otherwise for this remote and somewhat illiquid property, and that’s access liquidity in a highly efficient marketplace.

Specifically, I offered this property up as collateral for a loan on NFTfi, a peer-to-peer NFT loan marketplace at a very modest LTV of 32%. My offer was filled and I was able to access the funds with a single click of a button. If I default on the loan, the NFTfi smart contract will transfer the NFT to the lender and with that the lender would become the legitimate owner of the property in Sun Valley. The stakes in this case are real.

If you’re thinking about what kind of person would ever want to make this kind of loan, consider that more than $400 million worth of NFT loans have already been conducted on NFTfi since inception. The most commonly used collateral is digital artwork like cryptopunks and Bored Ape Yacht Club, which collectively represent $164 million of that total volume alone. When borrowers use this digital artwork as collateral the lender may end up stuck with an NFT with no physical connection to the real world. For an entire niche audience of lenders, this doesn’t bother them. However, as someone with a more apprehensive view toward risk in lending, the introduction of real physical collateral, actual property in the United States no less, is a game changer.

I am not the first person to ever engage in this type of transaction. According to Fabrica, the first property-backed NFT loan was transacted in 2021. However, if I might be afforded any claim to fame it is for conducting the first ever domain name loan over Ethereum.

GoDaddy Enables Any Website Domain To Accept Payments

February 22, 2024“Hey, do you have a Zelle or Venmo or Website?”

GoDaddy, the domain name registrar and popular website hosting service, has jumped into the fray to offer website owners a new easy way to receive payments. Although the new feature is called a “crypto wallet” it can accept more than just ether. That’s because one of the most popular currencies being used on the Ethereum blockchain today is USDC, a digital dollar that is fully backed by real dollars.

GoDaddy, the domain name registrar and popular website hosting service, has jumped into the fray to offer website owners a new easy way to receive payments. Although the new feature is called a “crypto wallet” it can accept more than just ether. That’s because one of the most popular currencies being used on the Ethereum blockchain today is USDC, a digital dollar that is fully backed by real dollars.

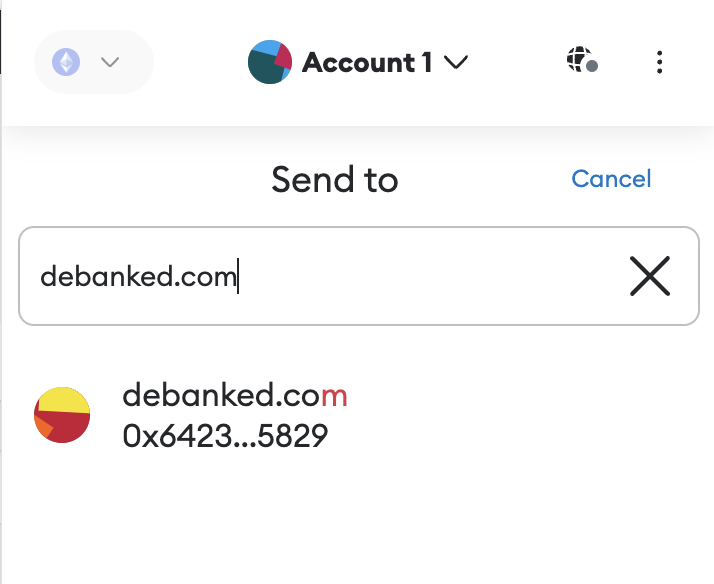

Specifically, GoDaddy is allowing any website domain owner to use their domain name as a crypto wallet address. That means instead of relying on someone’s Zelle or Venmo address, you can just send funds (ether, USDC or more) to the domain name of the website, like debanked.com for example. Again, “crypto” doesn’t necessarily mean exotic coins since the blockchain can facilitate the transfer of digital dollars as well.

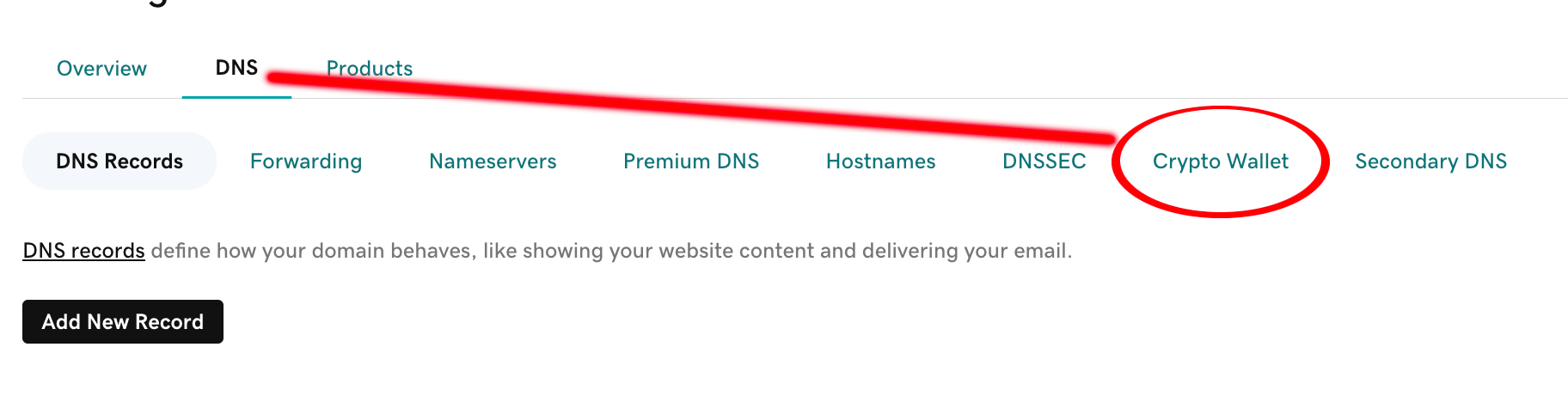

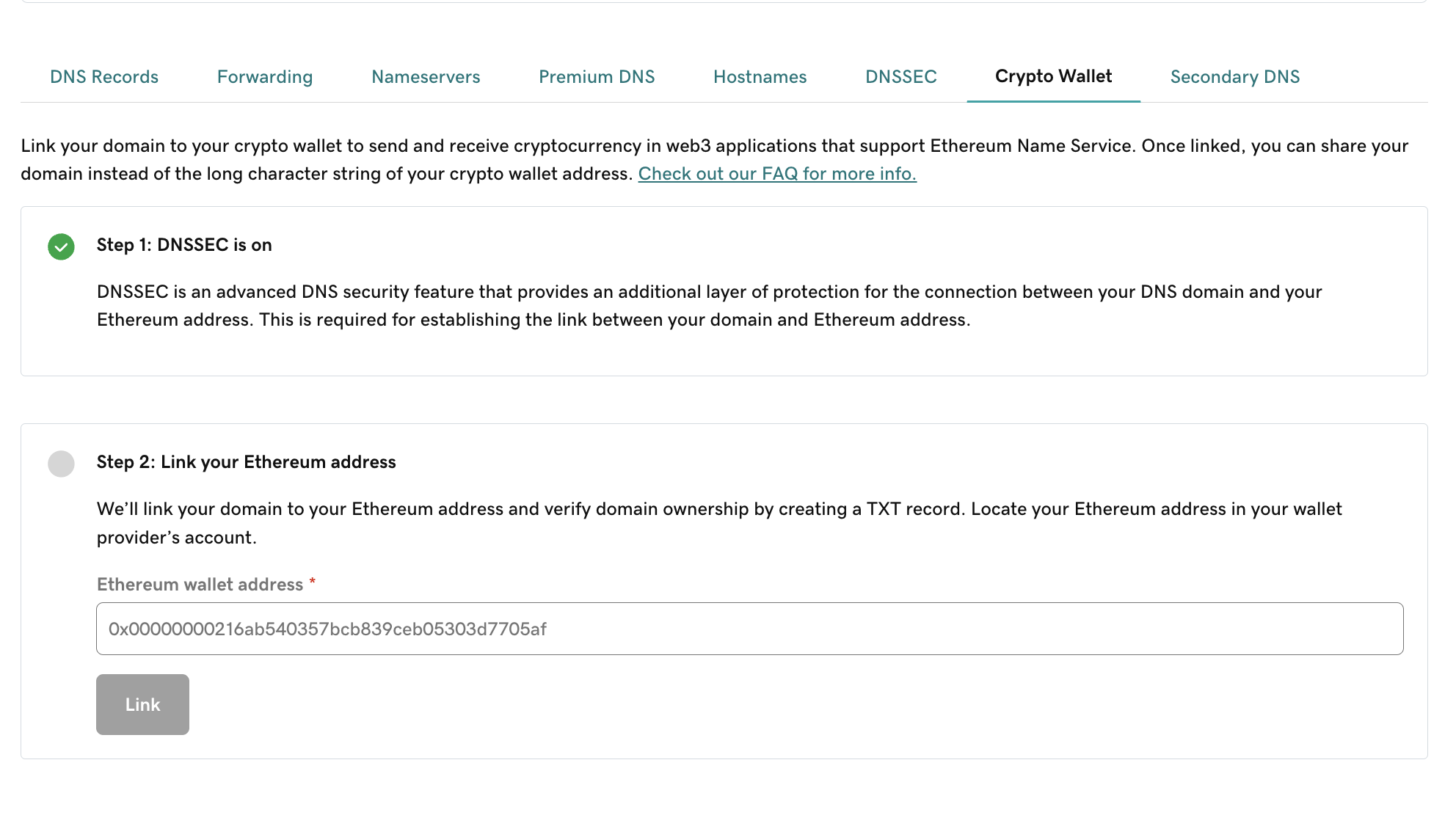

To try it, just go to the DNS settings in your GoDaddy account, click the “Crypto Wallet” tab, and then just click the “turn on” button and enter in your Ethereum address in the next field. That’s it. That’s all you have to do. Now your website domain name can accept payments over the blockchain. It assumes you have an Ethereum address already, which if you don’t well then that’s an article for another day as that all happens outside of GoDaddy. In the meantime, see the below guide:

Forget the Metaverse, I Bought Real Land

February 20, 2024 In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

In 1958, developers purchased 82,000 acres of barren land that was situated a hundred miles north of Los Angeles with a plan to build a sprawling metropolis for 400,000 future residents. As it instantly became the third largest city in California by land area, they chose an appropriately symbolic name, California City. It was a flop from the start. Although powerful marketing led to the sale of 50,000 lots by the early 1970s, the city only had a population of 1,300 people by 1969. That was bad enough that the Federal Trade Commission intervened in 1972 and forced a settlement that allowed thousands of landowners to get refunds. California City held on, however, and it’s now home to nearly 15,000 residents. It even has its own airport. But still, what it has become is still remarkably short of the original vision.

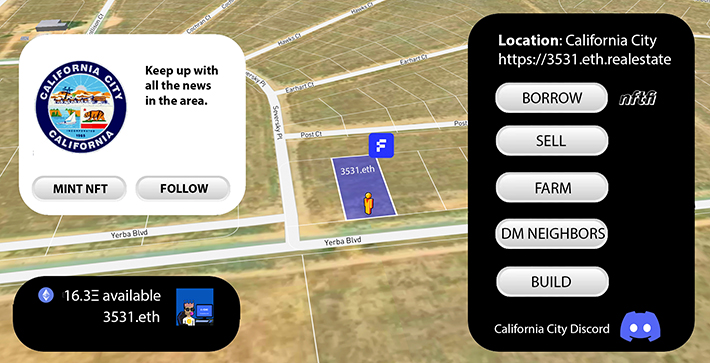

All of this history was something I breezed through right before I impulsively clicked a button on my screen asking me to confirm my purchase for a lot there. One click. That’s apparently all it took to become the newest member of a potential future neighborhood in California City, one that might not ever come to fruition. But how I found it in the first place is the real story. It appears that in the modern era this sleepy desert outpost has become a bit of an experimental laboratory for something relatively new in the real estate world, converting properties into NFTs.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Here’s how it’s done. A landowner places their property into an individual trust and ownership of that trust is governed by whomever owns the corresponding NFT on Ethereum. In effect, the owner of the trust would be defined by their ugly hex address, like this one for example: 0x64233eAa064ef0d54ff1A963933D0D2d46ab5829. It’s actually quite basic and it’s all made possible by a “proptech” company called Fabrica.

Founded in 2018 and backed by investors like Mark Cuban and Zain Jaffer, properties tokenized by Fabrica “can be traded instantly, used as collateral and are compatible with all NFT platforms,” the company states. “The product automates sales transactions, facilitating title transfer, payments and regulatory compliance.” Fabrica facilitates the on-ramping of your land into an NFT and even provides its own marketplace for buyers and sellers. That’s where I got mine. Interested parties can read up on a property’s on-chain history and even check the title. There’s also a cool little Google Earth-like animation that flies the user to their specific plot of land. The experience feels a lot like buying a plot of virtual land in a video game or the metaverse except this land is real. That means that sleek little NFT in your digital wallet comes with real responsibilities like property taxes, which Fabrica works to keep the owner informed about. It also means any and all liabilities of property ownership. The upside is that you can go and visit it in real life and even develop it. You can’t do that in a video game.

Although I’ve counted six properties in California City that are immediately identifiable as NFTs, it’s hardly the only place in the United States where this is being done. Properties available for sale as NFTs as of this writing include locations across Colorado, Arizona, New Mexico, San Bernardino-CA, and even Orange, New York. Some are very remote and speculative, while others are a part of normal civilization and priced accordingly. Buyer beware of course given the serious nature of these assets.

Perhaps one of the biggest obstacles to understanding how this is all possible is the widespread misconception of what NFTs are. Most of the American population lives under the mistaken impression that NFTs are cartoon art pictures like Bored Apes or CryptoPunks that were all the rage in 2021 and to some extent are still popular in niche circles, but almost anything can be tokenized. More recently, for example, domain names are being converted into NFTs to facilitate faster sales and quicker payouts. The same is true now here with land. Not only can land ownership change hands in the blink of an eye by transferring the NFT but one can also easily tap into the value by pledging it on a peer-to-peer NFT loan marketplace like NFTfi. Fabrica officially announced a partnership with NFTfi this past December, for example. The possibilities are endless

For the perpetual skeptics of all things blockchain that are convinced real business will only ever be done in the real world, a visualization of an NFT on a crypto wallet app might not be all that convincing, especially if the icon for it is situated right next to one of those expensive monkey pictures that kids wouldn’t shut up about years ago. The proof then is in the adventure. With a drive of less than two hours from Downtown Los Angeles, there’s a little plot of land on a quiet street known as Yerba Boulevard. It’s covered in weeds and reddish soil. Empty plains make up most of the backdrop but the suburbs are very slowly creeping their way there. In fact, I’ve since learned who my neighbor is across the street. It’s a 26,000 square foot cannabis facility that was just built in 2022. I bet the owners would be into NFTs (😂). Since that facility is up for sale, numerous 3D surrounding views exist of my plot. Turns out I can even walk to the airport. It’s not much but it’s home to me and all I could afford for the purpose of this story and learning what it was all about. Maybe those 400,000 planned residents will eventually want my land and it’ll make me a millionaire. Ah the allure of California City.

BROKER FAIR RETURNS TO NYC – MAY 20

February 15, 2024

| Broker Fair is BACK! The annual conference for small business finance brokers returns to New York City on May 20, 2024. The venue is the Metropolitan Pavilion on 18th Street in Manhattan. This will be the 6th Broker Fair in NYC since it first launched in 2018.

For questions or inquiries, please email events@debanked.com or call 917-722-0808. You can watch what’s been said at previous Broker Fairs on our new Broker Bites video page. |

Top Industry Execs Attend Small Business Finance Leaders Summit in Washington DC

January 29, 2024 Fifty top C-level executives attended the Small Business Finance Leaders Summit in Washington DC last week to discuss the economy, small business finance, policy issues, regulatory impacts, and industry best practices. Co-hosted by two major trade organizations, the Small Business Finance Association (SBFA) and the Innovative Lending Platform Association (ILPA), it was invite-only and open to members of both.

Fifty top C-level executives attended the Small Business Finance Leaders Summit in Washington DC last week to discuss the economy, small business finance, policy issues, regulatory impacts, and industry best practices. Co-hosted by two major trade organizations, the Small Business Finance Association (SBFA) and the Innovative Lending Platform Association (ILPA), it was invite-only and open to members of both.

Speakers included US Senator Roger Marshall, Tom Sullivan from the US Chamber of Commerce, Holly Wade from the National Federation of Independent Business, Aaron Klein from Brookings, Will Tumulty from Rapid Finance, Justin Bakes from Forward Financing, Kirk Chartier from OnDeck, and Steve Allocca from Funding Circle, among others.

“As our industry matures, it’s important to provide industry leaders with an opportunity to connect and engage with high-level thought leaders,” said Steve Denis, Executive Director of the SBFA. “We believe our C-level Summit complements the Broker Fair and other industry conferences like Money 20/20 or Nexus. We hope to expand our Summit in June to bring in some new industry voices and will continue to focus on high-end content that is meaningful and strategic for our members and other top industry leaders.”

The organizations are planning another Summit in early June to build upon the success.

The Story Behind the Broker Battle Champion

January 26, 2024 “I think I’m the best because I understand my clients very, very well,” said Anthony Truglia, an Account Manager at CapFront. “I listen to them, I ask the right questions, and I really try to dive very deeply into what it is the problem that they’re facing, and I try to find a solution to it to the best of my abilities.”

“I think I’m the best because I understand my clients very, very well,” said Anthony Truglia, an Account Manager at CapFront. “I listen to them, I ask the right questions, and I really try to dive very deeply into what it is the problem that they’re facing, and I try to find a solution to it to the best of my abilities.”

Truglia uttered these lines in a calm baritone voice on the red carpet at deBanked CONNECT MIAMI just hours before the inaugural Broker Battle in which he had been accepted as a contestant. The contest was designed to showcase the top brokers taking real but hypothetical questions and applying their knowledge live on stage.

At the time, Truglia had no idea how it was going to be conducted, not to mention that the other highly qualified contestants had also projected equally similar confidence in the likelihoods that they were going to win. It was anyone’s game at that point and the suspense was palpable. There had never been anything like it.

“I’m definitely going to be watching that,” said Manny Yosipov of Advanced Recovery Group during a show floor interview before it took place. “I’ve never seen a broker battle, never heard of a broker battle.”

“Broker Battle is huge because it shows the level that you can reach of talking to these clients, dealing with objections, and just selling in general,” said Joshua Hillian, Creative Director at Advance Funds Network. “I think a lot of people have the wrong idea of sales–but at the end of the day it’s question-based, customer focused, and that’s what it’s about.”

Hillian’s colleague Irving Betesh was slated to go first in the Battle later that evening. Betesh, like others, said that they had been preparing for this day well in advance. There was an overwhelming desire from all of them to showcase not only their technical knowledge but also their friendly diagnostic qualities. This was an educational opportunity for everyone.

When it finally kicked off, Truglia and Betesh squared off against fellow contestants Corey Digi, Stanley Mitchell, Danielle Rivelli, and Mike Brooks.

When it finally kicked off, Truglia and Betesh squared off against fellow contestants Corey Digi, Stanley Mitchell, Danielle Rivelli, and Mike Brooks.

By the time Truglia went on stage, which was last in the order, the four judges and thousands in the audience had already heard five impressive performances. But Truglia delivered, earning a near perfect score that sent him to the final championship round against experienced veteran Danielle Rivelli. And when that close matchup was completed, he found himself wearing a gold belt and holding a big check that duly crowned him as the Top Broker.

For those that didn’t know him, Anthony Truglia was simply the man that had put on the most impressive performance, an Account Manager at CapFront who won the hearts and minds of his peers. deBanked wanted to know more as he was little known to the editorial team until the day of his victory. It turns out he’s got an interesting story.

Anthony Truglia

Truglia was born and raised in Stamford, Connecticut and got his education at Lawrence University in Appleton, Wisconsin. He interned for a paper company that he said was reminiscent of Dunder Mifflin in the hit sitcom The Office, where he got a taste of doing sales. There, he discovered his own inner drive but paper was not the business he wanted to be in. “I was very young and I’ve always been very ambitious, always trying to accomplish something,” he said. After that he aimed big and actually launched his own coffee business, which ultimately didn’t pan out. Truglia followed that up with real estate, which he enjoyed, until he met someone that changed everything for him, a mentor that was making a name for themselves in the world of small business financing.

“See, I know most people when they get into this industry they’re just thrown into the gauntlet, they maybe have a team lead that gives them some supervision and some pointers, maybe you go through like a training for a month with a group of people, but I actually got one on one training with Justin Friedman,” Truglia said. Friedman, as one might already be familiar, is currently the Head of Sales Training & Development for Enova International, the parent company of one of the largest small business lenders in the country. At the corporate level, one could confidently say that he is among the best of the best.

“See, I know most people when they get into this industry they’re just thrown into the gauntlet, they maybe have a team lead that gives them some supervision and some pointers, maybe you go through like a training for a month with a group of people, but I actually got one on one training with Justin Friedman,” Truglia said. Friedman, as one might already be familiar, is currently the Head of Sales Training & Development for Enova International, the parent company of one of the largest small business lenders in the country. At the corporate level, one could confidently say that he is among the best of the best.

That was in 2018 for Truglia, where that one-on-one training included roleplay rehearsals, ones that eventually resembled the format of the Broker Battle he’d partake in nearly six years later. Truglia’s career has led him to CapFront. He speaks incredibly highly of the company and its CEO Zack Fiddle. If one suspected that Truglia’s time in the business had led him to slow down or retreat to back-office work, they’d be wrong. Truglia says that he’s on the front lines making about 150 customer calls per day on average.

“…my job is to contact [inquiring clients] as soon as possible to get a feel for whether they’re interested, if they’ve already been funded or not, but also just trying to figure out what it is they’re trying to accomplish really, try to gauge their urgency, gauge what their comfortability is, and see if we can find something that they will be comfortable with,” he says. “But also it’s a fine line because people’s aspirations are oftentimes not anywhere close to what they qualify for. And unfortunately, not a lot of people are aware of what lenders look for so that’s where we come into play.”

To get ready every morning to do this job he’s up at 6am and off to the gym before he even has his first cup of coffee. Then it’s game time, a lifestyle he’s accustomed to that doesn’t require anything else to pump him up.

“I’ve just gotten to that point where I’m very confident I know what I’m talking about. I’ve heard every question asked and I just practice it so daily that [outside motivation] is not really needed anymore,” he says.

Truglia is also confident that the type of role he fulfills is here to stay, that even lurking AI technologies are not something to fear.

“I definitely think that AI is not going to take away sales jobs because I’m one of those people that thinks that people enjoy talking to human beings. They don’t like talking to robots,” he says. “I think there’s something about—even if [an AI] sounded good, and you know it’s not really a human deep down, there’s no connection. So there’s no loyalty generated. I think people naturally like to talk to people, they like the personal connections relationship.”

But in real life, one might not be the only person that a potential client is considering and how they make a final decision to move forward could entirely depend on the best vibe that they feel.

But in real life, one might not be the only person that a potential client is considering and how they make a final decision to move forward could entirely depend on the best vibe that they feel.

“I always tell clients, ‘check out our company, myself on Trustpilot’ and stuff like that, do they always do that? Sometimes, not always. But from a psychological standpoint, I think a lot of times it comes down to how professional you are, how polished, your tone—just the chemistry that you can develop in that first call is what usually decides if this is somebody that you enjoy speaking to.”

This entire thought process ultimately played out on stage where his approach, one which included warmly thanking the judges for their imaginary call and the reaching in for a fist bump to close a deal, wooed the judges in his favor.

“[My team was] all very ecstatic for me,” he says. “And I thank them very much deeply for it. They were certainly rooting for me.”