Articles by deBanked Staff

Role-playing and The Value of Practicing Sales Calls

March 31, 2025deBanked asked several brokers over the past month about the value of role-playing with colleagues to prepare for real life sales engagements. Below are some excerpts of what they said.

Cheryl Tibbs, Commercial Capital Connect: “Before my broker life, I was a call center supervisor, so just really familiar with call centers making cold calls and that type of thing. So it’s very important [to role play], I think you have to practice. You don’t want to read a script, you don’t want to sound robotic, but you want to be engaged enough where you can have a good conversation with people without having to really think about it.”

Cheryl Tibbs, Commercial Capital Connect: “Before my broker life, I was a call center supervisor, so just really familiar with call centers making cold calls and that type of thing. So it’s very important [to role play], I think you have to practice. You don’t want to read a script, you don’t want to sound robotic, but you want to be engaged enough where you can have a good conversation with people without having to really think about it.”

Is there a point where practice is no longer necessary?

“Our industry changes day-to-day, little by little, things are changing. So I think it’s just always incumbent upon us to sharpen our skills. That means practicing at least once a week.”

Josh Feinberg, Everlasting Capital: “Role-playing is like stretching before going for a run. It makes it possible for you to be fast on your feet and really be able to have the answers when you’re talking to a, let’s just say, a construction company that does equipment financing, and they’ve financed all of their equipment. A lot of times they’re going to be more knowledgeable about the equipment financing and leasing product than a lot of the brokers that are going to be talking to them in regards to it.”

Josh Feinberg, Everlasting Capital: “Role-playing is like stretching before going for a run. It makes it possible for you to be fast on your feet and really be able to have the answers when you’re talking to a, let’s just say, a construction company that does equipment financing, and they’ve financed all of their equipment. A lot of times they’re going to be more knowledgeable about the equipment financing and leasing product than a lot of the brokers that are going to be talking to them in regards to it.”

Is this something you do with your own reps?

“Yes, especially when someone is newer or starting out, role playing is essential to even a point just like on Equipping The Dream, we need to make sure that we’re call-coaching too. While we’re listening to them on the phone we’re in their ear telling them what to say, just to have them get used to it. And then we do a bunch of different role playing…we’ve done it hundreds and thousands of times over the years”

Adam Oster, Canyongate Financial: “We have a set list of questions: understanding the merchants needs and building that relationship. And if I know somebody’s really good but they’re not doing well, then we’ll go back and say, ‘Hey, let’s role play. Because there’s something—you’re too complacent, you’re missing something, or you’re not listening to the customer.’ So role play is very important.”

Adam Oster, Canyongate Financial: “We have a set list of questions: understanding the merchants needs and building that relationship. And if I know somebody’s really good but they’re not doing well, then we’ll go back and say, ‘Hey, let’s role play. Because there’s something—you’re too complacent, you’re missing something, or you’re not listening to the customer.’ So role play is very important.”

How does this take place?

“If they’re here locally, we’ll do it in-house a lot of times. I’ve got a couple people—one in California, one in Austin, Texas, so we have to do it over the phone. And if somebody’s thriving, I’ll ask them, ‘What are you doing? What are you saying to your dealerships or your customers that are helping you get deals?'”

Register for Broker Fair 2025 – May 19 – NYC

March 28, 2025

Broker Fair 2025 returns in May. Here’s what you need to know:

Book Your Room at ModernHaus SoHo. Us this link to get our special room rate.

Preshow Party ModernHaus rooftop at JIMMY May 18, 7-9pm

Conference May 19, 9-5pm

Register for the Preshow and Conference here

Contact us here to become a sponsor or email events@debanked.com.

Prosper Marketplace Originated $2.2B in Consumer Loans in 2024

March 28, 2025 Prosper Marketplace, the last vestige of the P2P lending era, put up a repeat origination performance in 2024 vs 2023. The company originated $2.2B in consumer loans in 2024 and in 2023. That number had hit $3.3B in 2022 as part of the post-covid boom and had come in at only $1.9B in 2021.

Prosper Marketplace, the last vestige of the P2P lending era, put up a repeat origination performance in 2024 vs 2023. The company originated $2.2B in consumer loans in 2024 and in 2023. That number had hit $3.3B in 2022 as part of the post-covid boom and had come in at only $1.9B in 2021.

Only 7% of its originations in 2024 were from the “note channel” aka the peer-to-peer platform.

“We have incurred operating losses in prior years and may continue to incur net losses in the future,” the company disclosed in its annual report. “For the years ended December 31, 2024 and 2023, we incurred net losses of $54.1 million and $106.5 million, respectively. Additionally, from our inception through December 31, 2024, we have had an accumulated deficit of $644.2 million. We believe our liquidity needs for the next twelve months, and for the foreseeable future beyond that period, can be met through transaction fees, servicing fees, net interest income, other revenue, proceeds from sales of loans and securitizations, realized gains from the Credit Card portfolio and Cash and Cash Equivalents.”

Prosper used to compete against LendingClub as a peer-to-peer investment platform. LendingClub, however, discontinued its peer-to-peer business five years ago when it acquired Radius Bank.

Small Business Truth in Lending Bill Under Consideration in Maryland

March 27, 2025The “Small Business Truth in Lending” Bill introduced in Maryland on January 24, 2025, is continuing to advance through the state’s legislature. Among the finer details in the bill is an APR disclosure requirement on commercial finance transactions. The bill has attracted testimony from various organizations including the Responsible Business Lending Coalition, Revenue Based Finance Coalition, Innovative Lending Platform Association, Electronic Transactions Association, Rapid Finance, the Maryland Transportation Builders and Materials Association, and the Maryland Bankers Association. The majority have argued against the bill’s APR requirement. The combined testimonies are available here.

The bill’s path can be followed here.

The Art of Funding The Deal

March 26, 2025If you had fun at Broker Fair 2024…

… then you’ll love Broker Fair 2025.

PayPal Exceeds $30B in Business Loans and Merchant Cash Advances

March 26, 2025 PayPal has officially crossed $30B in merchant cash advance and business loan originations, the company announced.

PayPal has officially crossed $30B in merchant cash advance and business loan originations, the company announced.

“Access to capital is consistently one of the top challenges small businesses face as they look to maintain and scale their businesses,” shared Michelle Gill, EVP and GM of SMB and Financial Services at PayPal in an official release. “Traditional business loans are not only difficult to secure for small businesses, but the application process can be challenging and prohibitively time consuming. PayPal’s financing solutions have a streamlined online application process with no lengthy paperwork or extensive credit checks, and approved PayPal loans are funded within minutes. We launched PayPal Working Capital and PayPal Business Loan to serve this important need, and to provide a quick and responsible way to inject much needed capital to help fuel small business growth.”

PayPal had pulled back significantly on originations for a while as can be seen here but ramped back up last fall. For example, PayPal said that global originations had surpassed $25.6B at the end of Q2 2022 across a total of 1.3 million transactions. That means it has added roughly $5B in originations across 100,000 transactions in the span of almost 3 years since they now report 1.4 million total.

“Small businesses have seen tremendous value in PayPal Working Capital and PayPal Business Loan, as both offerings continue to receive remarkable feedback from customers,” the company said. “Additionally, both offerings have achieved Net Promoter Scores of 76 and 85 respectively and our customers renew loans or access our offerings on a repeat basis more than 90% of the time. Businesses also experience an increase in their total PayPal payment volume by 36% after adopting PayPal Working Capital and 16% after taking a PayPal Business Loan.”

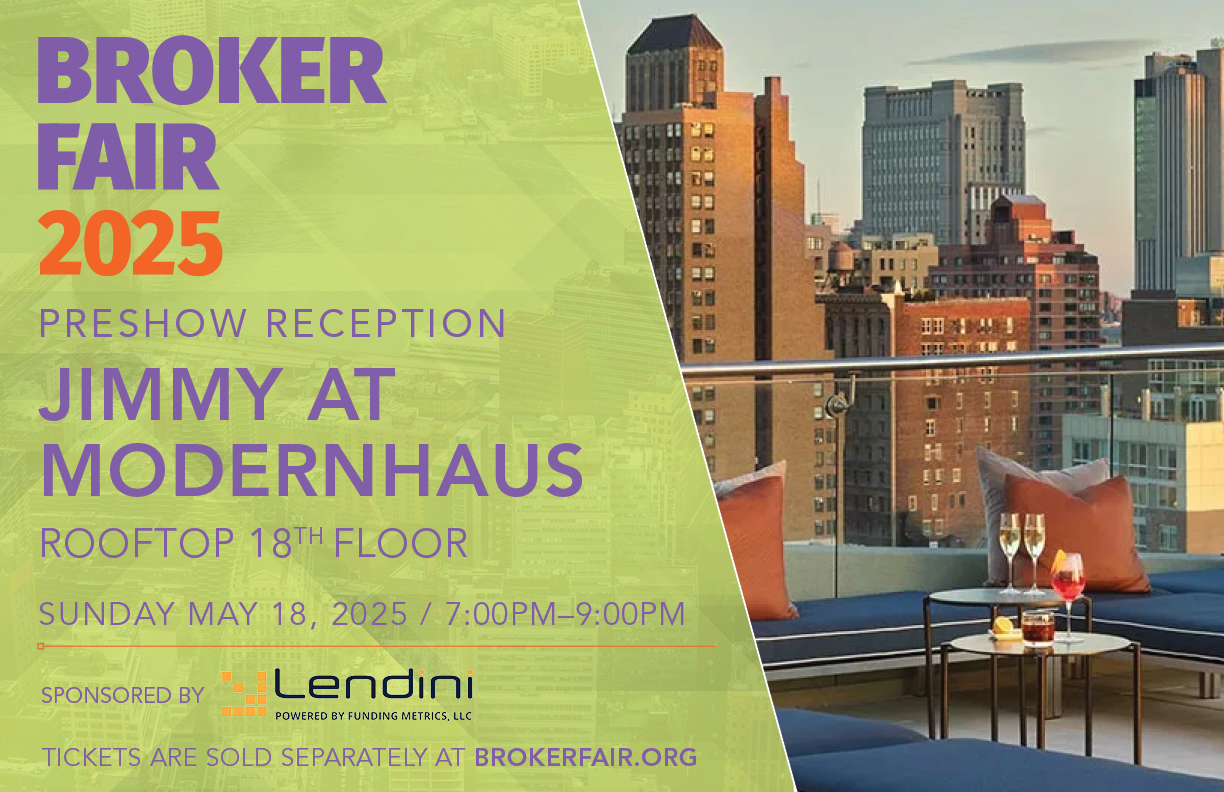

Broker Fair Preshow Party Info – NYC

March 25, 2025Broker Fair 2025’s preshow party is at JIMMY, located on the rooftop of ModernHaus in SoHo. Sponsored by Lendini, it’s being held on the evening of May 18th. To attend, make sure you add the preshow ticket during online checkout for Broker Fair. Broker Fair’s special pricing room block is also at ModernHaus and you should use this link to book your hotel stay.

Broker Fair is on May 19th in NYC at Tribeca 360 in Tribeca, walking distance from ModernHaus.

Book Your Room for Broker Fair 2025 – NYC – May 19

March 21, 2025Book your room at ModernHaus located in the SoHo neighborhood of Manhattan using our special link. The pre-show party will be on the hotel’s rooftop bar JIMMY. The conference itself is just blocks away at Tribeca 360. To register for the pre-show and/or the conference, click here.

For any questions, email events@debanked.com or call 917-722-0808.