Articles by deBanked Staff

Square Funded $339M to SMBs in Q1

May 2, 2018

Square’s small business funding arm, Square Capital, made over 50,000 business loans for a total of $339 million in Q1, according to the company’s latest earnings report. That figure is a 35% increase year-over-year and puts them on pace to break last year’s $1.177B total. OnDeck, by comparison, who is arguably their top rival, made $2.11B in business loans last year.

“[..] they just don’t have another way to get access to that sort of capital. And when they get it, they invest in their business,” Square CFO Sarah Friar, said of their merchants during the earnings call. “They’re buying inventory, they’re hiring new employees, they may be taking any lease hold and opening that second location. And when they do that, their business grows and hence our business grows. So, we still think we have a unique product that no one else can really follow us into.”

Square also earned $34 million in revenue from bitcoin, thanks to the Cash App they launched in January that allows users to buy and sell bitcoin. Bitcoin was mentioned an eye-opening 37 times in their quarterly shareholder letter, while their loan program is only referenced 7 times.

Overall, the company brought in $669 million in revenue and recorded a $24 million loss. They also entered into an agreement to buy Weebly, a company that helps people build professional websites and online stores.

“Weebly will expand Square’s customer base globally and add a new recurring revenue stream. Weebly has millions of customers and more than 625,000 paid subscribers,” the company wrote.

Shopify Capital Issued $60.4M in Merchant Cash Advances in Q1

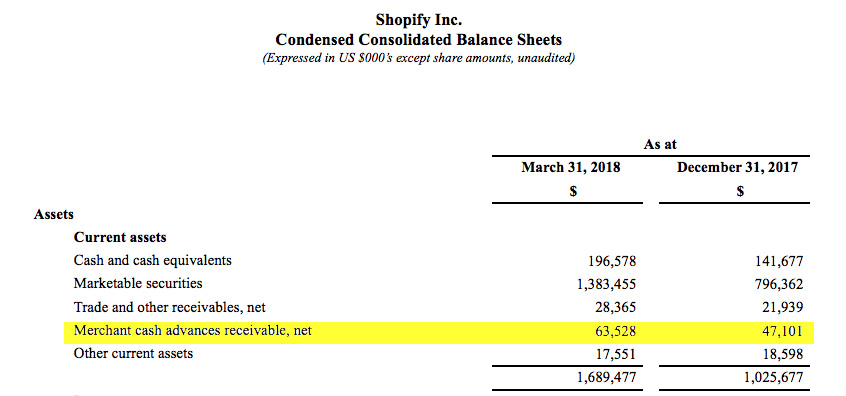

May 1, 2018 Shopify Capital, Shopify’s small business funding arm, issued $60.4 million in merchant cash advances in Q1, according to the company’s earnings report, an increase of more than 300% year-over-year. The company has advanced $230 million to merchants since April 2016.

Shopify Capital, Shopify’s small business funding arm, issued $60.4 million in merchant cash advances in Q1, according to the company’s earnings report, an increase of more than 300% year-over-year. The company has advanced $230 million to merchants since April 2016.

On the company’s earnings call, Canaccord Genuity equity researcher David Hynes, inquired about the patterns of seasonal demand one could expect for the company’s merchant cash advances.

“So in terms of seasonality on Shopify Capital,” said Shopify COO Harley Finkelstein, “it’s important to note that the use of proceeds for Shopify Capital for most of our merchants tend to be in the realm of inventory or marketing spend, which we quite like, because that leads to more sales, which makes it easier for them to return the capital to us.

“Obviously, there’s the seasonality of capital reflecting the seasonality of retail in general, which is certainly more of a Q4 issue than it is a Q1 issue,” he added.

Canaccord’s Hynes also referred to Shopify’s product as a loan but was corrected by Finkelstein.

“Just keep in mind, these are not loans, these are cash advances, so I want to be very clear about that,” Finkelstein explained.

Shopify is a Canadian e-commerce company headquartered in Ottawa, Ontario. It is also the name of its proprietary e-commerce platform for online stores and retail point-of-sale systems

View the company’s earnings report here

Yellowstone Capital Funded $61 Million in April

May 1, 2018Yellowstone Capital originated $61 million in funding to small businesses in April, according to the company. The year-to-date total now exceeds $200 million.

Yellowstone Capital, which is based in Jersey City, NJ, originated $553 million in 2017.

What You Can Find on the BCFP Consumer Complaint Database

April 30, 2018 Last week, Acting Director of the BCFP Mick Mulvaney told bankers that he had plans to make the agency’s consumer complaints database no longer visible to the public. In light of this, deBanked searched the agency’s complaint database. While there were numerous grievances that consumers reported because they could not fully resolve an issue with a financial service company on their own, we also found a host of questionable entries that leave much to be desired about the underlying issue and resolution sought.

Last week, Acting Director of the BCFP Mick Mulvaney told bankers that he had plans to make the agency’s consumer complaints database no longer visible to the public. In light of this, deBanked searched the agency’s complaint database. While there were numerous grievances that consumers reported because they could not fully resolve an issue with a financial service company on their own, we also found a host of questionable entries that leave much to be desired about the underlying issue and resolution sought.

Part of a complaint from last April against Bank of America reads as follows:

“The XXXX XXXX XXXX Police Beat you up XXXX Times and dont file Charges 5 times stays on youre record and you cant get Residency. All Countries murder the XXXX XXXX collect there benefits indefinitely After youre XXXX.”

Another complaint against Wells Fargo from December of last year reads:

“They are lower than pond scum and belong in prison. both XXXX XXXX executive resolution specialist and XXXX XXXX Sr. VP refuse to return my calls.”

And yet another complaint against U.S. Bancorp from July of last year asserts that a certain fraud department is:

“full of shit.”

Others are incomplete, like the following complaint against Experian from earlier this month:

“I’m an authorized user on this account but did not sign up for this on XXXX account.”

Taking the consumer complaints database out of public view could benefit lenders from complaints that have not been fully vetted. A consequence of it being public is that an independent party could paint a picture about a financial company’s behavior by simply tallying the raw number of complaints, regardless of whether those complaints are genuine.

Such a thing has been done. Several months ago, LendEDU published a ranking system of banks by the number of complaints they have received, placing Wells Fargo and Bank of America in the #1 and #2 spots respectively. Time Magazine picked up that story and presented it as “20 Banks That Consumers Loved to Hate in 2017” and ranked the number of complaints to the banks’ total deposits. Minnesota-based TCF Bank was crowned the worst.

Among some of the complaints that deBanked reviewed about TCF Bank did not even appear to be complaints at all. Interspersed with seemingly real grievances were some rather general questions or comments like how to view an account balance, how to access your account information through the mobile app, a purported compliment about the bank’s service that was nonetheless attributed to them as a complaint, and complaints about other companies that did not even mention TCF Bank but nonetheless counted as a complaint against them. All of these counted toward their complaint totals regardless of the content.

Chris Larsen on Crypto, Ripple, and ICOs

April 24, 2018 At LendIt Fintech, Ripple co-founder and Chairman Chris Larsen got real in his on-stage conversation with Jo Ann Barefoot. This is what you missed:

At LendIt Fintech, Ripple co-founder and Chairman Chris Larsen got real in his on-stage conversation with Jo Ann Barefoot. This is what you missed:

I think this is a fundamental shift in fintech and what we believe the big thing happening here is the development of a second internet. We call it the internet of value so that value, money, assets will begin moving as quickly and efficiently as data has been moving for the last 25 years

Using SWIFT is like sending a letter. You know, when drop it in the mailbox, you have no idea where it is, if it got there or not. So, getting away from that I think is profound. And what we would say is that, you know, a lot of the backlash from globalization today, it’s not because globalization is bad. It’s essential. It’s that it’s incomplete because globalization needs kind of 3 key systems to be working together and it needs interoperability and data.

I think all new technologies start with a, you know, screw the government, disruption, tear everything down. So, I think that’s natural and then, you know, the internet started that way too and then it has to sort of grow up. And particularly, it’s solving real world problems. Real world problems are always more complicated than that. And then when you switch to finance, this is different. Right? You know, the internet was mostly technology. Mostly. It’s just now kind of crashing into regulatory issues.

I think on some of the other things like ICOs, we’re pretty anti-ICO. I think it’s a bad thing to get involved with from the founder’s perspective because, you know, if you’re a founder and you can raise money many ways today, do you really want to do something where you’re going to have the SEC, you know, kind of threat hanging over your head for 10 years with strict liability? You just don’t want that. You know, that’s a problem.

[..]From building currencies, digital assets, ICOs typically say, “Okay. There’s a currency for this use case and none other.” That’s kind of the opposite of the way it should go. Currencies need to be as liquid as possible. And so, they’re going to have as many use cases as possible. For XRP for example, the kind of early beachhead has been cross border payments, but we see that as just the beginning of something that really has a multitude of use cases. To get as liquid as possible, that’s what drives utility and value at the end of the day. So, I think in all fronts ICOs are problematic and that’s why you’re seeing the regulators crack down on them, not everywhere, but I think they’ll be transformed. They’ll probably look like, you know, IPOs at the end of the day.

Boiler Rooms Are Not Brands, Kabbage CEO Says

April 21, 2018

Kabbage CEO Rob Frohwein has a knack for speaking his mind at lending conferences and LendIt two weeks ago was no different. Below are some of the most notable quotes from his April 10th presentation.

On building a brand

Unfortunately, in the online lending space, most companies basically think that boiler rooms = brand. Boiler rooms don’t equal brand. They have these huge call shops and that’s what they’re focused on. That doesn’t create brand. It just doesn’t. You have to spend money in order to build a brand over time. You have to have a brand obviously from a user experience and a customer service experience that people love. That’s how you build a brand.

We’ve invested over $125 million into building our brand specifically. We don’t use brokers and brokers are those 3rd parties that go out and find loans for you, but they don’t represent your company in the process.

How 2018 differs from 2015

About 6 months ago, I was asked to speak on a panel and it wasn’t this conference. And so, I got on the phone with the conference organizer and he said to me “Hey, we’d like to do a panel on fintech and bank partnerships.” Total yawn. 2015 called. They want their panel topic back. I mean, after all, there are probably more panels on fintech and bank partnerships than there are actual conversations going on between fintechs and banks. 2018 is all about relationships.

If the only thing you’re doing is lending money online, it’s going to go the way of the dinosaur. It’s very important. It doesn’t mean that the companies are gonna blow up. It doesn’t mean that there’s going to be any challenges, you know, trying to grow that business, but they’re not going to be the kind of exciting companies that we saw just a few years ago.

The only way to build substantial enterprise value is to be in a position to expand your brand’s offerings.

On whether or not your relationship with the customer can naturally extend to other products

I’ve heard lots of people say I had 2 million customers so I can sell them an auto loan. Actually, you can’t. That’s not the way it works. That’s not the way you build the company. You can certainly try, but the question becomes do you have implicit permission from the customer to make this kind of an offer?

How close is the next product you’re launching from both the function and a brand perspective to your last product? Right? Is it close? Smith & Wesson came out with a lot of bicycles. I am not sure what amendment covers bicycles, but they did not do great with the Smith & Wesson bicycles as far as I know.

The challenge is that most online lending companies don’t really have much of an idea about what their customers want or need because they only have basic credit info at the time of qualification and they also are just getting repayment information. That does not equal understanding the customer.

On engaging with your customers

If you’re not interacting with them very often, then they’re not thinking about you very often.

Kabbage customers take 20 loans over 4 to 5 years, 4-5 loans a year every year. We have that many positive interactions. Our competitors average 2.2.

Finally, I really think of this as the potato chip dream. And I think about Amazon a lot when I talk about the potato chip dream. What that dream is the day that Kabbage is able to sell bags of potato chips to our customers and our customers are like “of course, I’m gonna buy potato chips from Kabbage, why would I buy them from anybody else?” That will mean that Kabbage is worth hundreds of billions and our customers are incredibly happy in the process because it necessarily means that we will provide them with every product and service between where we are today and potato chips tomorrow. And that’s really the key for what we’re trying to accomplish, is allow us to expand our offerings in a natural evolutionary way and take care of our customers. And I really do think that all of us here should think about that as well especially if you’re running an online lending company. Focus back on the customer. Build those relationships. Figure out how to take it to the next level.

Industry Representatives to Testify at California Hearing

April 18, 2018

Several people will be testifying in front of the Senate Committee on Banking and Financial Institutions in California today. Among them are Joe Looney, COO & GC at RapidAdvance, who will be speaking on behalf of the Small Business Finance Association, and Katherine Fisher, Partner at Hudson Cook LLP, who will be speaking on behalf of the Commercial Finance Coalition.

At issue is SB 1235, a bill that would require providers of commercial financing to provide disclosures about the cost of that financing to the recipients of the financing.

Industry analysts believe the bill could have implications not just for small business lending but also for factoring and merchant cash advance.

Update: Full video of the hearing below

World Business Lenders Responds to the New York Post Story

April 13, 2018

A controversial story published in the New York Post earlier this week about World Business Lenders has drawn a response from the company. The text below was circulated by email to all World Business Lenders employees. With permission, it is being republished here.

——-

As you may be aware, an article appeared earlier this week in a local tabloid which described entirely unsubstantiated allegations against our company and members of its senior management team made by a disgruntled former employee. Because the allegations are as inflammatory as they are baseless, I thought you should hear from me, since I am responsible for the day-to-day operation of the company’s business and ensuring compliance with its policies. Nevertheless, I am accountable to WBL’s Board of Managers. As soon as we became aware of these false allegations, we alerted the Board, including retired U.S. Congressman Edolphus Towns, who chairs the Board committee which focuses on WBL’s reputation in the business community. During his many decades of distinguished service to our country, Congressman Towns chaired the U.S. Congressional Black Caucus and the U.S. Committee on Oversight and Government Reform.

First, the allegations of race discrimination are patently false. I am very proud of WBL’s unwavering commitment to the practice of providing equal employment opportunities to all of its employees and applicants; our company has zero tolerance for employment discrimination or retaliation of any type. And, I want to remind you that, if at any time you feel you are being treated unfairly at work, for any reason, WBL’s policy encourages you to surface and escalate such concerns.

Second, I want to address this disgruntled employee’s outrageous and untrue allegations that WBL defrauded the State of New Jersey. Since we moved to Jersey City in 2016, we have been welcomed with open arms by the State and maintained a cooperative and constructive relationship. WBL has participated in and supported State programs designed to provide employment to some of New Jersey’s most vulnerable residents. We continue to enjoy our partnerships with various State agencies, including our ongoing grant from the Economic Development Authority. To be clear, at no time has any agency of the State of New Jersey expressed any concerns or reservations about our Company or its activities. Rather, we have been commended for our contributions to the economy, both locally and on a state-wide basis.

Finally, I want to assure you that WBL is not in the habit of succumbing to poorly veiled financial demands, and we will not do so here.

– Doug Naidus, CEO