Federal Reserve Publishes Results of Alternative Lending Focus Groups

Alternative lenders have a lot of work to do!

Alternative lenders have a lot of work to do!

In a study conducted by the Federal Reserve which included focus groups moderated by the Nielsen Company, small business owners that had not heard of online lenders or had not used them, expressed extreme skepticism about their legitimacy. Among the negative responses were words such as shady, scam, identity theft, high APRs, ridiculous, wild west and unregulated, among others.

The focus groups, while small, had to meet a minimum criteria to be eligible:

- Have 2 to 20 employees

- Have annual revenues between $200,000 and $2 million

- Be the financial decision maker

- Not be a new business

Only 44 people participated.

There were both bright and dark spots in the findings, with one of the bright spots being that people’s attitudes became more positive about online lenders once they started to actually navigate the websites of several big industry players.

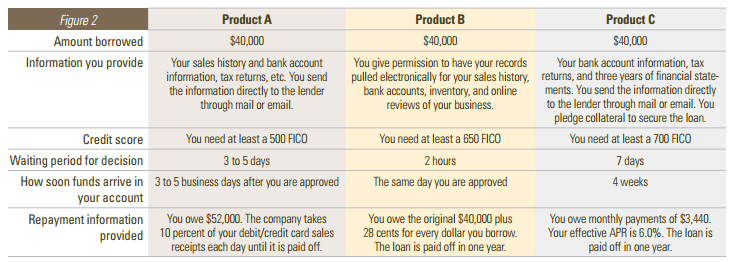

While the extent of the research is significant for any lender trying to get into the mind of a small business owner, there was a section in particular that warrants closer attention. In a mock comparison, participants were asked to compare three unnamed financial products, with one supposedly representing the characteristics of a merchant cash advance based on future credit card sales, another on a daily debit business loan, and the last a traditional bank loan.

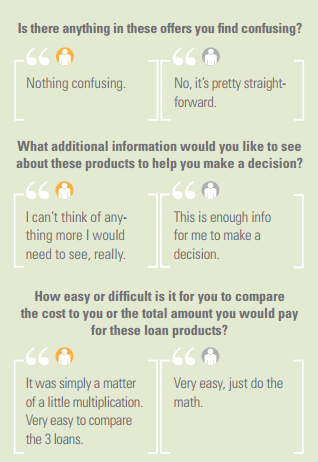

Respondents generally reported that they understood these offers and were not confused by them.

Unfortunately, the researchers assigned some gut-wrenching characteristics to the structure of the product alleged to represent merchant cash advances (Product A).

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

Since the researchers presented the theoretical product as a loan, not a sale, they have potentially tainted the inferred conclusions about the transparency of future receivable transactions. Given the strong authority associated with the Federal Reserve and Nielsen, there is a troubling implication that the findings about a hypothetical loan could be used as a basis to make future regulatory decisions about unrelated products like receivable purchases.

Ironically, the diversity of wrong answers to the interest rate question could lead one to this conclusion though, that APRs wouldn’t necessarily be a transparency cure.

If business owners don’t understand what Annual Percentage Rates represent, then it might not be a very good medium to make comparisons. This argument is actually reinforced by the study’s own research since two of the three products were presented without the confusion of interest rates and “participants initially reported the three were easy to compare and that they had all the information they needed to make a borrowing decision.”

In regards to the traditional bank loan, one business owner is actually quoted as saying, “I am not sure what they mean by my ‘effective APR.'”

While value can be gleaned from the results of such a small sample size of 44 business owners, it’s obvious that the researchers influenced the participants answers on how they assessed the cost of merchant cash advances in particular.

- A transaction typically structured as a sale was presented to participants as a loan.

- A predetermined time frame of 1 year was provided to participants when they were asked about interest rates even though purchase transactions have no time frame.

The merchant cash advance product presented in the focus groups has just about no similarities to the purchase transactions that exist in real life.

What are your thoughts on this report and particularly the way merchant cash advance is framed in it? You can download the full report, including the focus group questionnaire here.

Last modified: August 26, 2015Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.