The Merchant Cash Advance “Don’ts”

In sales training, young men and women are taught to negotiate with positive language to close a deal. For example: “We can’t meet the deadline” is replaced with “We can achieve the objective, but we may need to extend the deadline.” Or “We don’t offer that service” is transformed into “We offer many services that can add value to your business but that particular one is a challenge.”We apply a bit of that psychology when developing resources for business owners. People are a lot more open to input when you cast out the negativity. So it’s a bit ironic then that we created a printable reference form, titled The Merchant Cash Advance “Don’ts”. Though it may be perceived as a little condescending, this little banker/business pep talk can protect you from making a major mistake that could cost your business money. So keep it handy even if you don’t plan on applying in the near future.

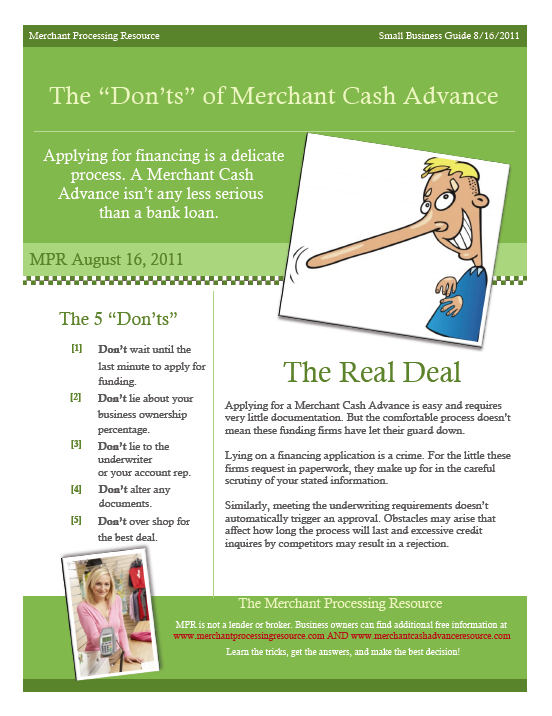

1. Don’t wait until the last minute to apply for funding.If a firm is advertising funding in 3-5 days, don’t put yourself in a position where you MUST have the funds in 5 days or less. The underwriting process may take longer than you anticipate. The advertised timeframes generally describe a perfect situation. For example: If all documents are received by day 1, all references checked out by day 2, you could potentially receive funds by day 3 assuming the technical setup is already completed. There are situations where business owners have spent 10 days waiting to obtain a copy of their lease from their landlord, which piggybacks onto the 3-5 days. Additionally, supplemental paperwork may be asked for, a trade reference might be unreachable, or your method of card acceptance might require more time to integrate. Anything can happen so don’t wait until the last minute!

2. Don’t lie about your business ownership percentage.This might be seem like silly advice but underwriters report that it’s a growing trend. People with low credit scores tend to assume that they will be declined for their score alone. Therefore they may feel inclined to state that a partner, friend, or family member with excellent credit is the owner of their business and not them. This is bad for several reasons:

- Credit score isn’t the sole determining factor for a Merchant Cash Advance. So why lie?

- Misrepresentation of ownership will be discovered and the application declined.

- Misrepresentation to obtain financing constitutes fraud and is a crime.

3. Don’t lie to the underwriter or your account rep.The liar loans of the mortgage boom ultimately led to the financial crisis and lending shortage. That means the days of declaring whatever you want to obtain the deal you want, are gone. If you state that you generate $100,000 in sales per month, be prepared to show documentation that backs up that claim. Your sales agent or account rep is probably compensated if you close on financing. That doesn’t mean they will help you get there at all cost. They are bound by a certain code of ethics and all applicable laws. If they become aware of any misrepresentation or intended misrepresentation, don’t expect them to be an accomplice to your dishonorable act. If you put them at risk, they will inform the underwriter and terminate your application.

4. Don’t alter any documents.Changing the expiration date on a lease, editing out the embarrassing withdrawals from the bank statements, or any other more or less blatant alteration will result in a rejection. Merchant Cash Advance underwriters are extremely adept in detecting alterations and fraud. Altering documents in an attempt to secure financing is a crime. You are well advised not to try this, no matter how harmless you may perceive the alteration to be.

5. Don’t over shop for a deal.You are entitled to obtain quotes from multiple sources, but don’t press your luck. Too many credit inquiries can spook an underwriter. For one, it tends to drive down the margins that will be earned because competition, thus making the deal less profitable for them and less attractive to put on the books. On the other hand, they may suspect that the other firms declined you and therefore they are being picked as a last resort. When underwriters start to feel this way, your approval may be retracted and it can be a tough battle to convince them to change it back.

We promise next time to provide a guide full of “Do’s”! But for now, we’re making it a point that Merchant Cash Advance is a serious business. The process may be fast and easy, but don’t get too comfortable and make claims you can’t back up. That will lead nowhere good…

– The Merchant Cash Advance Resource

http://www.merchantcashadvanceresource.com

Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.