Merchant Cash Advance Accounting Q&A

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

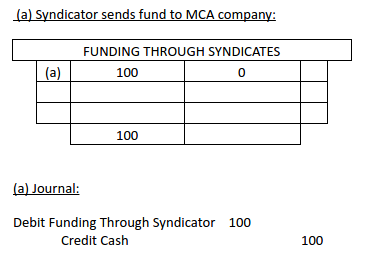

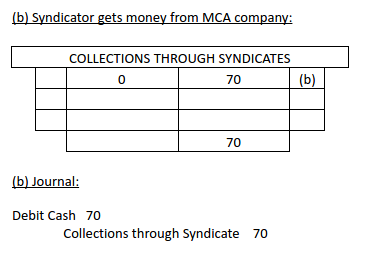

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

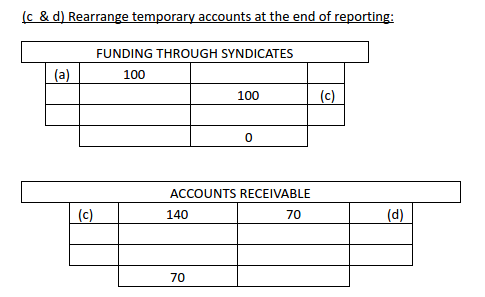

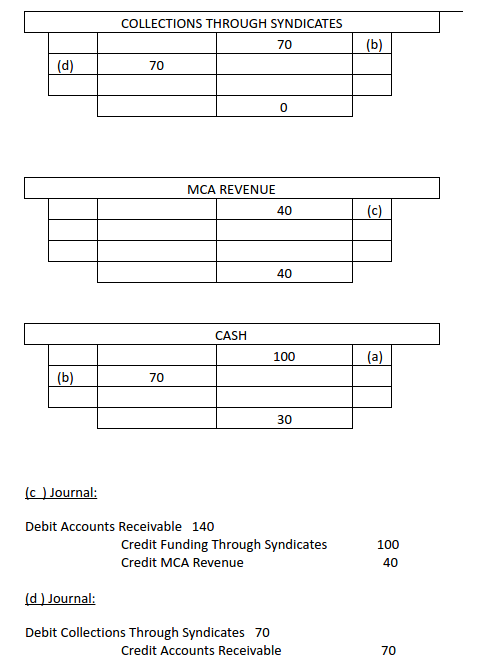

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

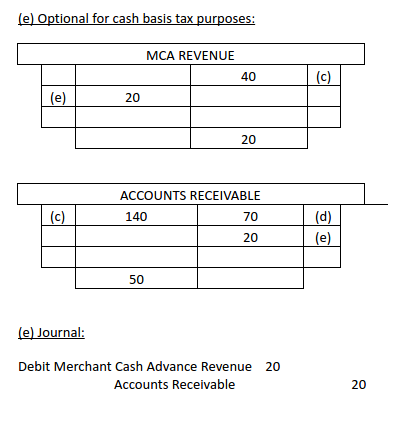

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com