Related Headlines

| 05/17/2023 | Percent closes $30M Series B |

| 01/12/2023 | Nomura invests in Percent |

Related Videos

What does Specified Percentage or Purchased Percentage Mean? |

Stories

Percentage of Merchants Seeking MCAs in 2022 Waned But Approval Rate Went Up

April 19, 2023 Only 7% of small businesses that applied for financing in 2022 applied for a merchant cash advance, according to the most recent report published by the Federal Reserve. Of those, 90% reported being approved for some amount of capital. That’s up from the 84% in 2020 and up from the 87% reported in 2019 prior to the pandemic. Approvals, it appears, were quite generous in 2022.

Only 7% of small businesses that applied for financing in 2022 applied for a merchant cash advance, according to the most recent report published by the Federal Reserve. Of those, 90% reported being approved for some amount of capital. That’s up from the 84% in 2020 and up from the 87% reported in 2019 prior to the pandemic. Approvals, it appears, were quite generous in 2022.

Overall, the percentage of merchants seeking MCAs has dipped, however. In 2019 for example, 9% of businesses said that they were seeking an MCA. In 2021 it was 8%. In 2022 it was 7% as mentioned above. The decrease could be explained by the pandemic which introduced an abundance of free and low interest government business aid. Also, the proliferation of low-cost online lenders created by the 0% interest rate environment may have weakened demand for alternatives like MCAs. Given that much has changed in the last 4 months, the Fed’s next report (scheduled for release in approximately March 2024) stands to be much more informative.

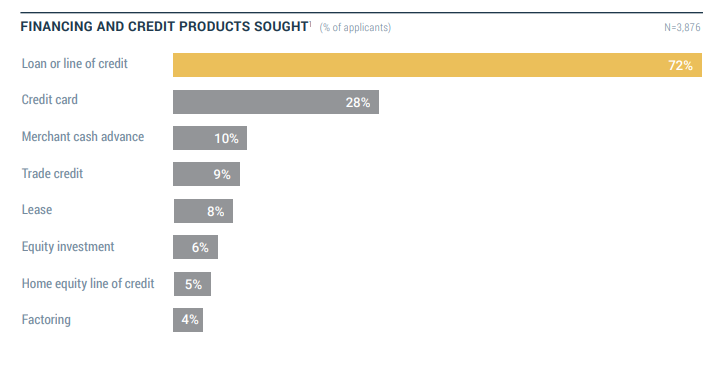

Ten Percent of Small Businesses That Sought Financing in 2021 Sought a Merchant Cash Advance

April 18, 2022A whopping 10% of small businesses that sought financing last year sought out a merchant cash advance, according to the latest study published by the Federal Reserve. That figure was up from 8% in 2020 and 9% in 2019. For the the preceding years, that figure had held fairly consistent at 7%. [See 2015, See 2017]. Market penetration, therefore, has arguably increased by about 40% since 2015.

Meanwhile, the percentage of applicants that sought out leasing has gone down over the last seven years: from 11% in 2015 to 8% in 2021. Factoring has hovered around 3-4% consistently.

The pursuit of of loans and lines of credit decreased dramatically from 89% in 2020 to 72% in 2021. And approvals have gone down across the board. Approvals on business loans, lines of credits, and MCAs hit a peak of 83% in 2019 and plunged to 76% in 2020, the first year of Covid. The figure fell even further in 2021, down to 68%. Online lenders and large banks had the lowest approval rates overall, at 51% and 48% respectively.

Q&A with Isaac Wagschal on One Percent Ventures’ Intentions to Transform MCA

October 21, 2021One Percent Ventures, a loaded name with implications depending on who reads it, is the latest small business funding company to enter the fray. No, it’s not funding for the one percent, but rather the numerical percentage the company would make off first-time clients with near-perfect performance. They’d make just one percent…

The concept, which caught the attention of deBanked, had to be explained in detail, especially when a merchant paying only $500 on a $50,000 advance was communicated as an example. Say what? The catch is in a rebate and the cost independent of the broker’s commission. Nevertheless, One Percent Ventures CEO Isaac Wagschal seems to be bringing in a new concept, one that was originally supposed to be 0%, he says, but he was already stuck with his company name. deBanked did a Q&A to find out exactly how it all works.

– The Editor

Q&A

Q (Adam Zaki): Why did you choose the name One Percent Ventures?

A (Isaac Wagschal): The original idea for One Percent Ventures wasn’t to be a funding company that gives one percent deals. Originally, we were going to provide branding and marketing services to small businesses who do not have any marketing, but can benefit from it. Our compensation was to be a one percent partnership in the company. Then a situation came my way where I was able to form a team of people with extensive knowledge and experience in the MCA space. I grabbed the opportunity and switched from marketing to funding small business.

We designed the product with a rebate that refunds basically the entire cost of the first advance. I realized that if we changed the rebate where instead of refunding 100% of the 1st advance factor cost, we keep 1%, I wouldn’t have to change the name and logo of the company. This is the reason our merchants are now paying one percent. If I had not already determined the name, the merchants would have been paying zero instead of one percent.

Q: What was the most difficult part of the shift from marketing to funding?

A: Shifting from marketing to funding was very difficult because of the nature of the market which existed at that time. That difficult transition forced the creation of our unique product, which includes rebates and payment-pauses. I looked into the mainstream MCA product in-depth, and realized that from a marketing point of view the product is flawed, and cannot be marketed properly. The more I scrutinized the MCA industry, I realized that the problems are not just from a marketing perspective. There are existential problems that need to be addressed, or they will eventually cause the demise of the industry altogether. Default rates are so high that mathematically the industry is forced to charge extremely high prices. This makes the product unmarketable to merchants who are not in the absolutely highest risk bracket.

I knew that unless we remade the product to be more attractive and marketable to a larger market share, the funding industry had no tangible room for expansion. Why would we want to get into this market space in the first place? As a team, we agreed that instead of hiring ISO-reps and underwriters, we would first hire accountants, actuaries, and data analysts.

We applied the same psychological principles used in marketing, where you try to predict and manipulate people’s reactions. By doing that, we were able to redesign the old MCA product. We introduced a rebate system that gives the merchant an opportunity to potentially only pay a $500.00 factor cost on a $50k advance. In this way, we expanded the current market share, and turned it into a hot product. I hear from ISOs on a daily basis who recontacted old unsuccessful leads, and turned them into deals after they presented the OPV-rebate and payment-pause-award system. This proved that the OPV product is expanding the market share.

Q: What are your thoughts about the market share in MCA?

A: The current market share consists of the absolute highest risk merchants who are willing to pay such high prices. It is becoming harder and harder to maintain deal flow. This has forced the industry to slowly keep raising the standard with respect to how many positions we are willing to accept. If nothing happens, we will soon find ourselves talking about 10th and 15th positions. This is certainly not sustainable, and puts an amazing amount of stress on the ISOs who are working tirelessly to maintain deal flow. They see it all happening, but feel helpless because at the end of the day, they can only present a product that a funder puts on the table. The tiny market of willing and able merchants is also a source of stress, and a key factor to the mistrust that is largely present between ISOs and funders.

Q: What are your thoughts on a relationship with the ISOs and funders?

A: Let’s face it, the way the current ISO-Funder relationship is set up scientifically creates a conflict of interest. It is simple math – when a funder loses a renewal that carried a potential profit of 50k and thinks that the deal could have happened if not for the 14 points that is reserved for the ISO, there is a natural conflict of interest. You can be honest with your ISOs and even give Rolexes and call them your partners on paper, but the spreadsheet still calculates a conflict of interest at the end. The lavish gifts are nice, but they do not eliminate the scientific conflict of interest.

We have corrected this fundamental problem by designing our business model so that our ISOs are genuine partners. This too is simple math – when a funder’s product is designed to issue an unheard-of large rebate, and 3rd party costs are deducted from the final rebate amount, the merchant will obviously be super happy because of the astronomic refund. More importantly, by using this model, the conflict of interests between ISO and funder is erased because mathematically the merchant paid the commission, not the funder!

Q: How does OPV make money? How do merchants qualify for all of your incentives? What are these incentives?

A: Let me first answer the latter part and explain how our product works and then I’ll come back to answer how we make money.

Our typical product is a ninety-day term at 1.49 sell rate. At mid-term, if the merchant didn’t miss any payments, they are eligible for an add-on, largely known as a renewal. At this phase, we begin to issue an OPV-Pause award after each cycle of four consecutive successfully completed payments. The pause awards can be submitted smoothly on our automated online system either one at a time, or they can be saved and initiate a pause for an entire week. After the final payment, if the merchant didn’t miss more than three payments, excluding the pauses, we refund the entire factor cost of the first advance except for 3rd party fees, processing fees, and 1% of the advance, which gives us only $500 profit on a 50k advance.

Every merchant that qualifies for funding, automatically qualifies for all the incentives. The OPV funding model is actually designed to perform better when more merchants actually receive the rebate. Why? Because that also means there has been a drop in the default rates. If every merchant was to qualify for the rebate, it would mean we had a zero percent default rate, which would allow us to make a healthy return, even if we made profit only on the 2nd advance.

This is precisely the reason we added the OPV-Pause awards. It is in our best interest to keep the merchant motivated to stay current on their payments, in order to qualify for the rebate. We even added a condition that in the event a merchant doesn’t have an unused pause award, they can purchase an OPV-Pause for 20% the daily payment. The goal must be to lower default rates so that we can lower the end cost. In this way we can expand the market share and keep the MCA industry alive. The OPV product is designed to do just that.

Q: What are your immediate goals for OPV? How about long term?

A: Phase I was designing the product and building the platform. Now in phase II, we plan to fund deals for at least a year before making any significant changes. We want to build relationships and earn trust by being transparent and honest, even when it hurts. At phase III we will analyze the data and make tweaks we deem necessary. At phase IV, given that the canary returned from the coal mine, we will share our intelligence, and license the OPV platform to reputable funders throughout the MCA industry.

Q: What is your outlook on the future of the non-bank small business funding/lending sphere?

A: In an effort to truly make a constructive change towards preserving the MCA industry, I will speak openly about the elephant in the room. We are all aware of the unfavorable new laws and regulations that constantly threaten our existence. As long as there are politicians who need to win elections, they will be on the hunt for “do-good projects.” There will always be a lobbyist that is looking for deal-flow, who is willing to provide the perfect “do-good” project. One of those will be – “Let’s save the poor merchant from the greedy funder.” The politician can only succeed because the nature of the MCA industry is such that our funders share only the good news. The bad news is confidential, so there is a stigma of excess profit in the MCA sphere. If we can successfully change that stigma, then we will be a thriving industry for many years to come.

Forty-Four Percent of Small Businesses Were More Than $100,000 in Debt in 2020

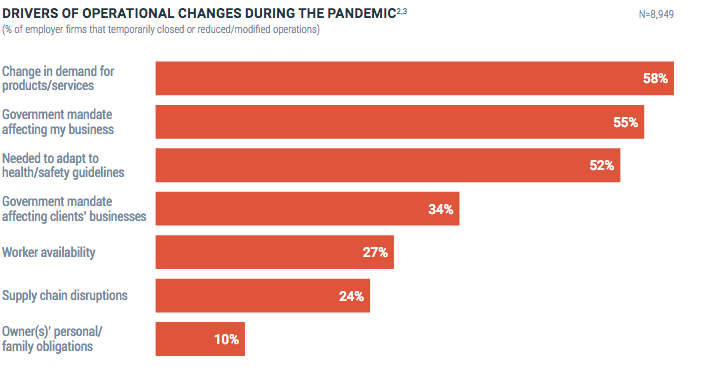

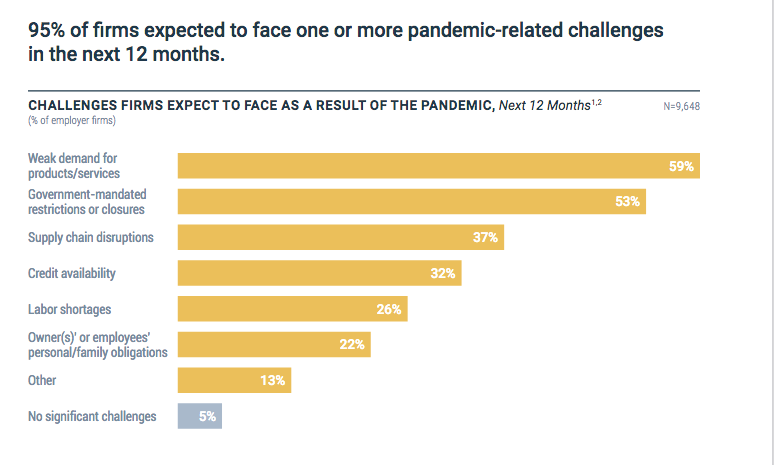

February 5, 2021 Fifty-three percent of firms expected total sales revenues for 2020 to be down by more than twenty-five percent because of the pandemic, according to the latest small business survey published by the Federal Reserve. Eighty-eight percent of firms indicated that sales had still not returned to normal.

Fifty-three percent of firms expected total sales revenues for 2020 to be down by more than twenty-five percent because of the pandemic, according to the latest small business survey published by the Federal Reserve. Eighty-eight percent of firms indicated that sales had still not returned to normal.

Of those hurt by shutdowns, supply chain troubles, and government shutdowns, 26% percent closed temporarily, fifty-six percent reduced their operations, and 48% percent modified their operations.

Fifty-seven percent of firms characterized their financial condition as “fair” or “poor.”

The struggle to remain open sent firms further into debt. Seventy-nine percent of firms had debt outstanding, an 8% increase from 2019. Debt also increased; the share of firms with more than $100,000 in debt rose from 31% to 44%.

The majority of U.S. businesses believe the next year will be rife with the same struggles as the last. Many believe weak demand, government shutdowns, and supply chain breaks will continue disrupting the world economy.

Overall, firms applied for financing less, from 43% in 2019 to 37% in 2020.

Firms got their funds this year through Government aid programs, and they did so through their pre-existing bank relationships, forgoing alternative funders. Forty-eight percent went through large banks for PPP, 43% to smaller banks. 95% and 83%, respectively, already had a relationship with their large or small bank.

Square Capital Made More Loans, Maintained Default Percentage, Continued to Show Why They’re A Tough Competitor in Fintech Loan Market

February 22, 2017Square has continued to set itself apart in the fintech lending space. The company announced Wednesday that Square Capital had facilitated 40,000 business loans for a total of $248 million in the fourth quarter of 2016. And they did that while holding their default rate at 4%.

A look at their recent loan volume compared to their competitor OnDeck:

| 2016 | Square | OnDeck |

| Q1 | $153,000,000 | $570,000,000 |

| Q2 | $189,000,000 | $590,000,000 |

| Q3 | $208,000,000 | $613,000,000 |

| Q4 | $248,000,000 | $632,000,000 |

Square Capital’s biggest competitive advantage is that they have practically no acquisition cost for their borrowers. “We’re able to upsell and cross-sell to our base of millions of sellers with minimal incremental cost,” Square’s Q4 earnings presentation says. Their payment’s customers, which they can convert to borrowers, processed around $50 billion in transactions last year.

Square had a net loss of $171.6 million across 2016 however, the bulk of which originated in the first quarter. The net loss for Q4 was only $15 million.

Annual Percentage Rates Fail Business Owners, Again

September 16, 2016 A survey of small businesses once again revealed that Total Cost of Capital (TCC) was a better metric than Annual Percentage Rate (APR) when choosing a small business loan. This study, conducted by Edelman Intelligence on behalf of the Electronic Transactions Association (ETA), found that a majority of respondents stated that they would look to minimize TCC, rather than APR, when considering loan options in the face of a short-term ROI opportunity.

A survey of small businesses once again revealed that Total Cost of Capital (TCC) was a better metric than Annual Percentage Rate (APR) when choosing a small business loan. This study, conducted by Edelman Intelligence on behalf of the Electronic Transactions Association (ETA), found that a majority of respondents stated that they would look to minimize TCC, rather than APR, when considering loan options in the face of a short-term ROI opportunity.

The ETA explained this in the report as follows:

Generally, when consumers take out a loan, they are not making an income-generating investment that would increase the funds available to pay the loan back. Therefore, in most situations, the more “affordable” loan for a consumer is one with a longer term and lower monthly payments, even if it results in paying more over the long term. Consumers, therefore, look at APR, which describes the interest and all fees that are a condition of the loan as an annual rate paid by a borrower each year on the outstanding principal during the loan term. APR takes into account differences in interest rates and fixed finance charges that may otherwise confuse a consumer borrower and is most useful in comparing similarly long-term loans, such as 30-year mortgages or multi-year auto loans. Likewise, APR is useful for comparing revolving lines of consumer credit, like credit cards, where the amount borrowed each month changes. APR allows consumers to compare the rate at which an outstanding balance would increase under different credit cards.

While APR describes the cost of the loan as an annualized percentage, TCC represents the sum of all interest and fees paid to the lender. As the Cleveland Federal Reserve recently noted, TCC enables a small business to determine the “affordability” of a product – a key driver for most small business borrowers. Unlike consumer loans, commercial loans are normally used to generate revenue by helping a business purchase equipment or inventory or hire additional employees. Thus, “affordability” for small business borrowers means assessing the cash flow impact of the loan and comparing the TCC of the loan and the return they expect to earn from investing the loan proceeds. To reduce TCC, many small business borrowers prefer short-term financing they can quickly pay back with the return on their investment (ROI).

The ETA’s full report can be VIEWED HERE.

The findings are consistent with other studies:

Fed study on small business borrowing

A debate with anecdotal evidence, demonstrating people’s inability to calculate an APR

Consumers also struggle to make sense of APR, according to a 2008 Fed study

Backdooring Deals? You’re a Loser

April 24, 2024 “Backdooring is just for losers,” says Thomas Chillemi, founder and CEO of Harvest Lending, a small business finance brokerage. “Like I think anybody who participates in it is just a loser.”

“Backdooring is just for losers,” says Thomas Chillemi, founder and CEO of Harvest Lending, a small business finance brokerage. “Like I think anybody who participates in it is just a loser.”

Backdooring, as colorfully referenced by Chillemi, is a colloquial term used widely across the industry to describe how leads, apps, or entire deals are stolen from brokers. The deal gets submitted through the front door and then leaks out the backdoor to an unauthorized third party. Chillemi sums it up as such: “backdooring is ‘I secured a lead, I secured a file in some way, shape or form. And that merchant is being contacted through my efforts somehow that I didn’t give permission to.'”

It’s a scenario that’s been top of mind at brokerages across the country for years, and it’s a problem that’s getting worse, according to sources that deBanked has spoken with.

“I would say backdooring is the worst of the worst right now,” says Josh Feinberg, CEO of Everlasting Capital, another small business finance brokerage. “I think as far as rogue employees go at direct funders, it’s the worst it’s ever been.”

Feinberg’s reference to “rogue employees” is just one such way that backdooring can occur. It can be an employee of a lender, management of a lender, an employee of the broker, a broker pretending to be a lender, and possibly in a worst case scenario even a cyber intruder like a hacker. Sometimes it’s a clandestine operation structured in a way to make it difficult for the broker to detect that their client’s file has been intercepted while other times backdooring is such a normalized function of one’s business that accepting a submission from a broker and then shopping it elsewhere to circumvent them is practically firm policy and done on an automated basis.

Some of the more seasoned brokers who are used to being on guard with what a lender intends to do with their file advise that their peers approach any proposed ISO agreement with a fine-tooth comb to establish what is or isn’t allowed. After all, if the agreement grants the lender the contractual right to backdoor the broker, is it really backdooring?

Others say the contract’s language can only carry the relationship so far.

“I only try to board up with people that seem to be good actors, but then you never know what an employee might do, right?” says Chillemi.

Whether it’s a jaded underwriter, a slick admin, or Bob in accounting who never says a peep, it only takes one individual to set eyes on an application to be in a position to transfer the information elsewhere for personal gain. deBanked examined this subject in years past and learned the lengths that rogue employees go through to extract deal data. For example, when one funding company blocked the ability to transfer data outside of the company’s network, an employee took photos of their screen with their phone. When the employer banned cell phones in the office in response, one employee wrote down deal data on scrap paper, threw it in the garbage, and then returned to the office building after hours to try and fish it out of the dumpster.

Whether it’s a jaded underwriter, a slick admin, or Bob in accounting who never says a peep, it only takes one individual to set eyes on an application to be in a position to transfer the information elsewhere for personal gain. deBanked examined this subject in years past and learned the lengths that rogue employees go through to extract deal data. For example, when one funding company blocked the ability to transfer data outside of the company’s network, an employee took photos of their screen with their phone. When the employer banned cell phones in the office in response, one employee wrote down deal data on scrap paper, threw it in the garbage, and then returned to the office building after hours to try and fish it out of the dumpster.

The absurdity of that visual alone implies there must be big bucks in the backdoor business. Indeed, according to screenshots forwarded to deBanked of what appears to be an underground Whatsapp group, backdoored deals are currently being marketed for sale with bank statements, social security numbers, and all. A single fresh backdoored file can go for $20 – $35 or buyers can purchase them in bulk, up to 600 at a time, for a discounted price.

“Fresh Packs” apparently fetch more because the applicants may not have signed a funding contract with anyone yet and are theoretically more warm to doing a deal even if they’re not quite sure how the company approaching them got all of their information. And it’s this speed and efficiency of the backdooring happening that’s making things extra difficult for brokers. For Chillemi, he says the backdooring in earlier years would reveal itself when someone would try to call his customer a month or two after the fact. “Like even if it happened after two or three days that felt really fast,” he says. “But now, you’re talking hours, like these people have it within hours and I just don’t even know how anybody could really compete with that.”

Brokers, ready for this, developed a tactic that is still used today as a front-line defense mechanism, they replace the applicant’s email address and phone number on the application with ones they control, so that when an attempted backdooring occurs, the caller is unsuspectingly contacting the very broker they are trying to steal the deal from. The result? They’re caught red-handed.

Brokers, ready for this, developed a tactic that is still used today as a front-line defense mechanism, they replace the applicant’s email address and phone number on the application with ones they control, so that when an attempted backdooring occurs, the caller is unsuspectingly contacting the very broker they are trying to steal the deal from. The result? They’re caught red-handed.

“I got a text from somebody claiming that they worked at Fidelity,” says Chillemi. “They texted me a picture of my own application. They’re so brazen that they’re just texting the merchant… they thought they were texting the merchant.”

Not only was the Fidelity component a deception, but the mistake of texting the broker who was just waiting to catch them is causing the backdoor shops to evolve. New backdoor callers know the application contact info might be booby-trapped so they’re now skip-tracing the applicants on an automated basis and getting their real contact info and using that instead.

For Feinberg at Everlasting, he says the method of substituting out an applicant’s contact info is not something they do, though he’s aware that it’s done by others in the working capital space. He says that it’s not something that would really be tolerated in the equipment finance side of the industry which operates much cleaner with no backdooring, at least in his experience. The lenders there hate it and everyone involved needs to be able to communicate with the customer. It’s just the working capital deals where all these problems happen.

“It’s defeating, and it’s a very very difficult thing to diagnose,” Feinberg says. He adds that the feeling is worse when realizing that it has happened even when submitting to top tier A players. There’s no delay either. He says that the customer can be called literally within the same hour of submitting it, which makes them look really bad.

“They lose complete trust in our company,” Feinberg says. “And it makes it very difficult to be able to work with these clients.”

According to Chillemi of Harvest, “Most of the time what happens is the merchant calls us and says, ‘Now I’m getting all these phone calls people saying they’re working with you,’ and it’s just kind of like an embarrassment of where I’ve got to explain to this person that somebody at these companies leaked their information that wasn’t supposed to. And it just makes me look bad, right?”

According to Chillemi of Harvest, “Most of the time what happens is the merchant calls us and says, ‘Now I’m getting all these phone calls people saying they’re working with you,’ and it’s just kind of like an embarrassment of where I’ve got to explain to this person that somebody at these companies leaked their information that wasn’t supposed to. And it just makes me look bad, right?”

Another owner of a large broker shop, who did not authorize his name to be used in connection with this story, says that while everyone’s mind immediately goes to the lending companies, the most common source of backdoored deals is actually from rogue employees inside the brokerages themselves. Whether it’s the rep backdooring themselves to circumvent splitting commissions with their employer or someone else in the chain that has access to the data, his advice was that brokerage owners first need to look extremely inwards before pointing fingers outwards. Investing in proper security is critical, he says.

But assuming that base is covered, Feinberg says that brokers should do a background check on the lenders and interview them like a lender would interview a merchant for funding.

“We absolutely look into the agreements that we sign but a lot of due diligence happens just on the first phone call,” Feinberg says. “Just on the first phone call we can judge whether this is going to be a real lender…”

A key question to ask, he says, is how compensation works. And that’s because an individual lender will have a defined fixed system whereas a backdoor broker pretending to be a lender is subject to the different compensation structures they have at all their different lending relationships and would not be able to guarantee any fixed commission pricing to the broker they are trying to trick into submitting, that is if they are intending to pay them out a percentage of the deals they backdoor them on in the first place.

“Trust is the number one thing with us,” Feinberg says. “And if trust gets broken, then it’s over. So we really try to work with people that we know personally. And the way that we’ve met people personally is through trade shows, specifically deBanked events.”

Chillemi argues that someone who tries to make their living off of backdoored deals are not salespeople at all, but as he reiterates, losers.

“[the backdoor broker] knows he’s a liar,” says Chillemi, “He’s calling these people saying he’s an underwriter… he’s not strong, he’s not learning. They don’t know what they’re doing. They’re putting the lenders at risk.”

Checking in On Stripe Capital

April 15, 2024 Everyone is well aware that Square does revenue-based financing loans, but lesser talked about is that Stripe does too. Stripe has been offering financing to merchants since at least 2019. Valued at more than $65 billion with IPO rumors swirling, Stripe has the potential to become one of the largest online small business lenders in the United States.

Everyone is well aware that Square does revenue-based financing loans, but lesser talked about is that Stripe does too. Stripe has been offering financing to merchants since at least 2019. Valued at more than $65 billion with IPO rumors swirling, Stripe has the potential to become one of the largest online small business lenders in the United States.

Stripe’s loan program is big enough to leave a trail of discussions across the web about their product, including on Reddit where some users have discussed getting loans well into the six figures. In February, one tech founder shared on X that a Stripe Capital loan had been very beneficial for his business.

Originally, Stripe offered a merchant cash advance but has since switched to doing revenue-based loans. In both cases, merchants pay by Stripe withholding a percentage of their card sales in what’s known industry-wide as a split.

No Broker Fees - Monumental Funding Solutions... monumental funding solutions has been working hard to bring you the very best there is to offer and this next deal you will not believe! we are doing ... |

Close Rate... of all the deals in your pipeline, what percentage do you actually close? sales close ratios let you know how effective you are as a sales rep. a... |

Ready to make some money?... the commercial finance academy is now accepting applications for our october classes!! we are offering a comprehensive 5 day course that will teach y... |

See Post... percentage of usage are they at... |

See Post... percentage for psf's or additions to their set up fee, but regardless if they do or not it's going to cost you that merchant or potentially even endanger the repayment if they don't net enough (this is really high risk stuff i'm talking about, but i have seen guys wack a 3k origination fee on a guy we funded for 10k). , , someone pointed out that certain places will allow you to add to their contract set up prior to drafting, and it's true.. i've done that before, which is also segways into another lesson of being aware of every funder's specifics from product space to buy rates, terms, commission allowances etc. it's key to know where you have maneuverability and how to place deals so that they not only get funded but it maximizes profit for you too. after all.. we all play this game to get paid right?... |

See Post... percent!... |