Alternative Lending: People are Finally Getting it

Alternative lending is all the rage these days and so much so that BusinessWeek asked the question: What Do Small Businesses Need Banks for Anyway?. They go on to name many companies with ties to the merchant cash advance industry, which is no surprise to us of course. It is interesting however to notice that the mainstream media is not only giving us the time of the day, but starting to treat us like royalty.

Alternative lending is all the rage these days and so much so that BusinessWeek asked the question: What Do Small Businesses Need Banks for Anyway?. They go on to name many companies with ties to the merchant cash advance industry, which is no surprise to us of course. It is interesting however to notice that the mainstream media is not only giving us the time of the day, but starting to treat us like royalty.

Five and a half years ago this very same collective of lenders were referred to as bottom feeding vampires¹. Over the next couple years they upgraded us to a very expensive alternative, then to an acceptable alternative, and now finally to who the hell needs banks when you have these great companies?!. You have to laugh just a little bit at the shift.

It’s easy to call a lender that charges high rates a bad seed when you have no sense of the context. The reality in lending is that a material amount of borrowers don’t make their payments on time or they don’t pay back the loan at all. That causes rates to go up to compensate for the losses. Critics argue that borrowers can’t make the payments or default because the rates were too high to begin with. Some lenders cave to that assumption and position themselves as a fair lender by undercutting the market rates. They eventually learn that defaults are less related to the cost of the loan and more so tied to a borrower’s willingness to repay or ability to repay. Meaning, loans with no interest tacked on to the principle will still be rocked by late payers and defaults. Wait, seriously?

Yes, welcome to America where sometimes borrowers face circumstances beyond their control or they maliciously decide they don’t want to pay. The overwhelming majority are in the former camp, the ones where sudden or gradual hardship is interfering with their ability to make good on their commitment. I admit, even I feel uncomfortable mentioning this. Nobody wants to be seen as picking on borrowers. We’d all rather pretend that lenders are inherently bad and borrowers are inherently innocent. The truth is that most lenders and borrowers are good but some lenders and borrowers are bad. Lending is a two way street and what’s fair for all is somewhere in the middle.

My friends in the commercial banking sector tell me their tolerance for bad debt is less than 1%. Even 1 single loan default over the course of a year could cause their entire portfolio performance to come crumbling down. They do make loans, but they’re often in the tens of millions or hundreds of millions of dollars and only to large established businesses that quite often, don’t even need the capital but would rather not jeopardize their liquidity by spending their own cash. Some of these loans end up getting classified as small business loans even though there’s nothing small business about them.

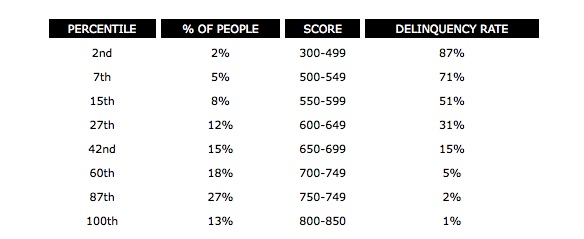

Mom and pop shops see the statistics and the corresponding rates of say 4% to 10% APR and set that as the bar to shoot for. Then they head down to their local bank and hit a roadblock. The average small retail/food service business is going to have a greater than 1% chance of default no matter how good it looks on paper. I mean think about it, what are the odds that things will go 99% as planned for a restaurant over the next 12 months? Do you think it’s reasonable to assume there is at least a 5% chance that any of the following could happen in the next year even without knowing anything specific? A failed health inspection, bad reviews published online, a revoked liquor license, construction outside impeding pedestrian traffic, internal damage caused by a flood or disaster, extreme weather hurting sales, major job losses in the area leading to people having lower disposable income, key employees quitting, theft, landlord not renewing the lease, competitor opening up in the neighborhood, or declining sales for no single identifiable reason? Lending money to retail businesses is risky, really risky. Suppose the above business owner had a history of late payments and defaults to begin with. At what cost does it begin to make sense to do this deal? And those are just the risks of what could happen to the business itself, so what about the other risks involved?

To a bank, the stereotypical entrepreneur is damaged goods. The hard knock humble beginnings of turning a vision into a successful business usually comes with personal financial sacrifice and in turn a lower credit score. And just as the successful entrepreneur is getting ready to explain his/her high debt to income ratio and story of triumph, they’re already being declined. Banks don’t care about the story. They care about the aggregate mathematics. If there’s just a 5% chance that the business isn’t going to be where it thinks it will be in a year from now, then the deal’s probably a non-starter. Leveraged? Declined. Poor credit? Declined. Business is running smoothly? Who cares, it’s declined already!

Extension on your taxes? Declined. Showing modest profit or a loss for tax purposes ::wink wink:: ? Declined. Didn’t file a tax return? Declined. Co-mingling funds with your personal finances? Declined. Overdrafts or NSFs? Declined. Unaudited financials? Declined. No collateral? Declined. Doing the books with paper and pen? Declined. Have less than 5 employees? Declined. Can’t find a document the bank wants? Declined. Need the money really badly? Declined. Experiencing a downturn? Declined. Have a tax lien? Declined. Have a criminal record? Declined.

Extension on your taxes? Declined. Showing modest profit or a loss for tax purposes ::wink wink:: ? Declined. Didn’t file a tax return? Declined. Co-mingling funds with your personal finances? Declined. Overdrafts or NSFs? Declined. Unaudited financials? Declined. No collateral? Declined. Doing the books with paper and pen? Declined. Have less than 5 employees? Declined. Can’t find a document the bank wants? Declined. Need the money really badly? Declined. Experiencing a downturn? Declined. Have a tax lien? Declined. Have a criminal record? Declined.

Get the picture? If you take a look at Lending Club, an alternative lender, they’re widely known to have a 90% decline rate. Their maximum interest rate is 29.99% APR. Think about that for a second. Some people would say, “WOW, 30% are you kidding me?” but statistically, Lending Club would be losing money on the deal 9 times out of 10 if they approved every single person that applied. Lending Club actually used to be more liberal with their approvals when they first started and what happened is that too many borrowers just didn’t pay. If you believe that Lending Club should approve even more loan applications than they already do, then they would have to compensate for the increased risk and we’d quickly see APRs reach well into the 40s,50s,and 60s.

A critic might argue that once an applicant exceeds the risk of a 30% APR loan, they probably shouldn’t be getting a loan from anyone. That’s not a bad suggestion and what happened is that when the lending world concurred with that 5 years ago, Americans and politicians went up in arms because “Banks weren’t lending.” No loans? Businesses can’t hire. No loans? Businesses can’t grow. No loans? Economy gets stuck in neutral. The nation demanded that capital flow despite the risks presented to the lenders. And so the finance world heeded the call to provide solutions and came up with a smorgasbord of financial products. Merchant Cash Advance financing was already established but had an especially unique characteristic that allowed it to take off. It structured financing as a sale, not a loan. A big problem was that traditional lenders and alternative lenders were at the mercy of state regulated interest rate caps. Once an applicant reached a certain risk threshold, they just couldn’t do the deal anymore. But when financial companies came in to buy future revenues in exchange for a large chunk of cash upfront, the system started to gain some traction.

The effective cost of the money got high, very high, yet they weren’t predatory. I say that because despite how expensive it seemed, most of them were getting eaten alive by defaults. From 2008 – 2010, many merchant cash advance companies filed for bankruptcy. One of the main attributes of a predatory lender is for the lender to actually be getting filthy rich. That means layering on interest way in excess of a healthy profit. Losing a lot of money to help borrowers and small businesses when no one else will can hardly describe a predatory lender.

One has to wonder that perhaps there is a better way. If unsecured financing breeds high defaults, then surely things would be different if a risky applicant secures the loan with collateral. Have the borrower put skin in the game and we’d have a different outcome right? Lenders such as Borro publicly describe their default rate as falling between 8-10%. They offer collateralized personal loans and are described as a “pawn shop for the posh” in the below video, though most of their clients are small business owners. This tells me that even in the instance where borrowers have something very valuable to lose, a significant percentage of them will not repay the loan in full regardless.

A look around at what merchant cash advance companies have been willing to admit has put their average bad debt between 2-5%. In my experience in this industry however, 8% – 15% is a lot more realistic. But are these funding companies getting filthy rich or treading water? Anyone can look at the financial statements of IOU Central², a lender that’s part of the broader merchant cash advance industry. Since they’re owned by a publicly traded company in Canada, we get to see firsthand that they’re suffering tremendous losses quarter after quarter. I find that to be perfectly in line with what I suggested about undercutting the market earlier. IOU Central’s allure is that their loans cost less than a traditional merchant cash advance. The end result is that after paying commissions to sales agents, paying interest on their capital, and factoring in bad debt, they’re hurting pretty badly.

On Deck Capital too, a company mentioned in the BusinessWeek article above acknowledges that they are not profitable, though they do not make their financials public to verify how unprofitable they are or if that’s really even the case.

An SBA loan through a bank may cost approximately 5.5% APR, but if the loan goes bad, the SBA covers almost all of the bank’s losses. There is no such security blanket in the real private sector. The market determines the rates based on the risk. Each funder measures risk differently and in 2013, there is no longer a one-size-fits-all cost of unsecured funding much like there was in 2007 with merchant cash advances. Compared to a bank loan, almost all of these alternative options will be perceived as expensive, but if banks don’t approve anyone, then they’re a terrible standard for a comparison.

It’s taken a long time for the public and the media to come to terms with that. Banks are still technically in the game but by proxy. They are financing numerous alternative lenders and merchant cash advance companies. Banks shouldn’t be lending out their client’s deposits to really risky businesses anyway. A bank is supposed to be safe. If they’re lending money to 100 businesses and 15 of them aren’t paying it back, then that’s the opposite of safe.

So what do small businesses need banks for anyway? Checking, payroll, overdraft coverage, debit cards, wires, record keeping, CDs etc. There is a place for banks in 2013 and beyond. Alternative lenders charge more and that’s okay. Ultimately it’s up to the borrowers to decide what they can sustain. It is better to have expensive options than no options at all. There’s endless proof of that when credit dried up five years ago. Small businesses cried foul so the market reacted. And here we are now with Kabbage, On Deck Capital, Business Financial Services, and Capital Access Network being portrayed as the norm, the new standard. Almost everything that would cause a bank to say “no” can be resolved in some way. That’s incredible and how it should be.

So what do small businesses need banks for anyway? Checking, payroll, overdraft coverage, debit cards, wires, record keeping, CDs etc. There is a place for banks in 2013 and beyond. Alternative lenders charge more and that’s okay. Ultimately it’s up to the borrowers to decide what they can sustain. It is better to have expensive options than no options at all. There’s endless proof of that when credit dried up five years ago. Small businesses cried foul so the market reacted. And here we are now with Kabbage, On Deck Capital, Business Financial Services, and Capital Access Network being portrayed as the norm, the new standard. Almost everything that would cause a bank to say “no” can be resolved in some way. That’s incredible and how it should be.

People are finally getting it.

– Merchant Processing Resource

https://debanked.com

MPR.mobi on your iPhone, Android, or iPad

¹ It took 5 years but Forbes has Finally deleted the March 13, 2008 article that haunted the merchant cash advance industry forever. In Look Who’s Making Coin off the Credit Crisis, Maureen Farrell referred to merchant cash advance companies as vampires that were feasting on small businesses and singled out some of the biggest names in the business at the time. It was Global Swift Funding* (GSF), one of the major funders cited by Farrell that exposed this assertion to be blatantly false. Not too long after the article was published, GSF closed their doors and filed for bankruptcy. It would seem that small businesses actually feasted on them by defaulting in record numbers. Back in April of this year, Forbes essentially rebuked that article when Cheryl Conner revisited the industry to note how much good it was doing in ‘Money, Money’ — How Alternative Lending Could Increase Your Company’s Revenue in 2013

*Disclosure: Raharney Capital, LLC the owner of this website currently owns the former domain of Global Swift Funding (GlobalSwiftFunding.com) though the companies did not have and do not have any ties to each other.

² IOU Central is a subsidiary of IOU Financial Inc. Management’s Discussion and Analysis of Financial Condition and Results of Operations as of August 22, 2013 are available at: http://cnsxmarkets.com/Storage/1563/144040_MDA_%282Q2013%29_-_FINAL.pdf

Last modified: April 20, 2019Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.